43 / 176

43 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

26

The other important aspect of banking sector's asset side in OIC member states is their

relatively less concentrated loan portfolio compared to Europe and US. The average loan size

relative to total assets is less than 40% in selected OIC member states.

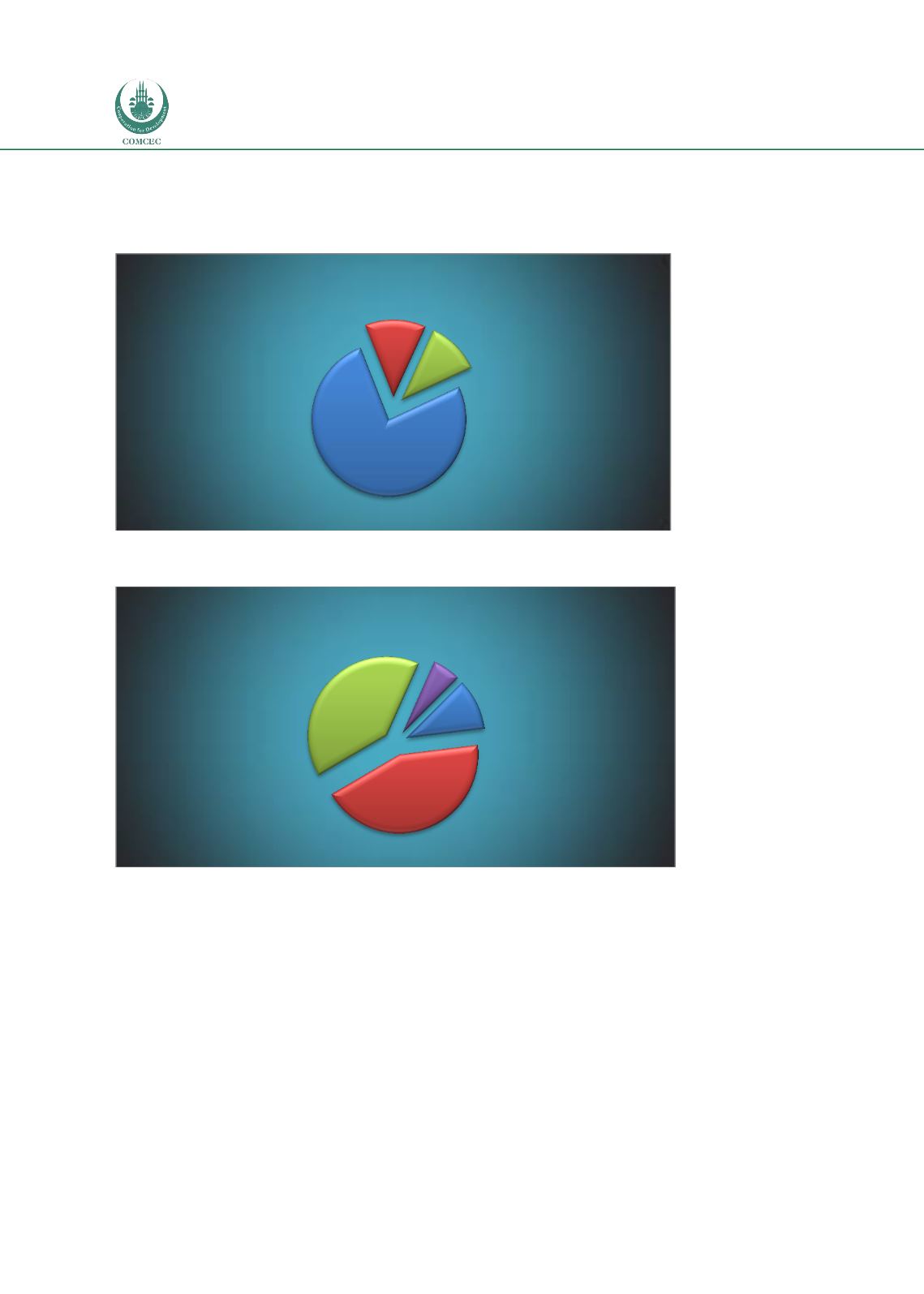

Figure 15: Liabilities for US Banks (2014)

Source: Bankscope

Figure 16: Liabilities for EU Banks (2014)

Source: Bankscope

3.1.2 Banking Capital in Selected OIC Countries

Capital is the most important soundness criteria for banking as the ratio of capital to total

assets is an important health measure for banks. The higher this ratio, the stronger the

banking sector is. Capital/asset ratio appears to be around 10% in OIC members, in general.

However, some countries have a serious difficulty in attaining a stable capital/asset ratio.

Particularly, Nigeria and Kazakhstan has shown a decreasing trend in their ratio in 2009 amid

to the negative impact of the global credit crunch in 2009. Regulatory framework requires the

calculation of this ratio based on a risk-based evaluation of assets; hence BASEL II and III

framework put a significant importance on finding risk weighted assets rather than total

assets, since different assets have different risk weights. Therefore, capital adequacy ratio

formula is crucial factor for assessing the quality of bank capital with respect to risk-weighted

assets. Figure 17 presents the corresponding ratio, which complies with the regulatory

Total

Deposits;

76

Other

Liabilities; 13

Total Equity; 11

Total Liability Decomposition (for US Banks)

Deposits from

Banks; 11

Total

Customers

Deposits;

44

Other

Liabilities;

40

Total Equity; 6

Total Liability Decomposition (for EU Banks)