40 / 176

40 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

23

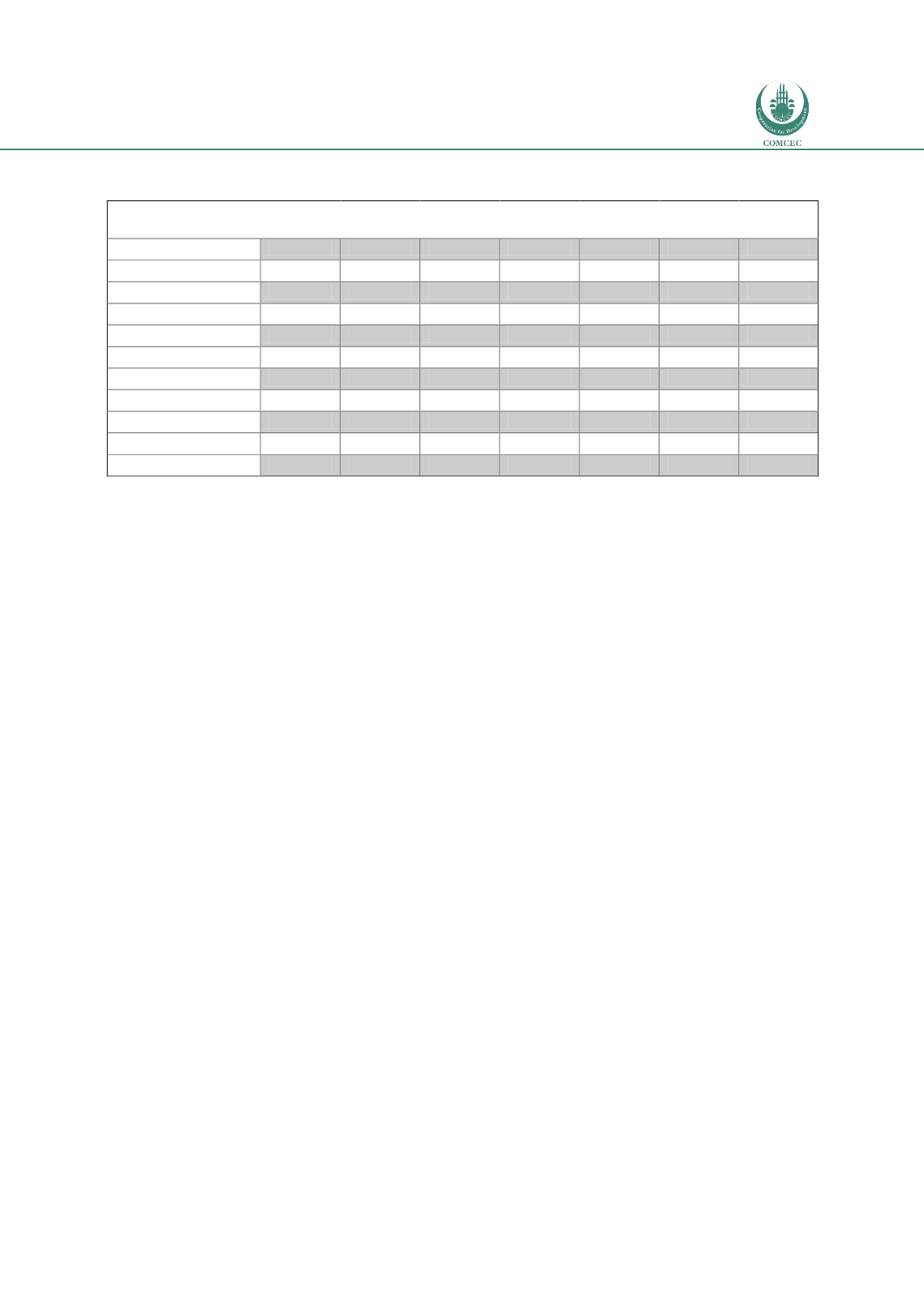

Table 5: Banking versus Non-banking financial sector size in the selected OIC Countries

(percentage)

2007

2008

2009

2010

2011

2012

2013

Turkey

79

76

75

74

72

69

71

Algeria

97

97

93

92

91

92

N/A

Indonesia

49

47

44

40

40

39

45

Kazakhstan

85

85

82

81

82

81

95

Malaysia

74

71

71

69

73

68

68

Nigeria

42

85

71

32

44

53

83

Pakistan

71

70

70

70

74

76

81

Saudi Arabia

58

65

64

62

59

56

57

UAE

65

72

71

68

69

67

67

Eurozone

24

22

23

26

24

25

N/A

USA

19

11

13

13

13

14

14

Source: Bankscope

As can be seen from Table 5, except for Indonesia, banking sector dominates non-banking

financial sector in the selected OIC member states. For most of the member countries, total

banking sector constitutes around 65% of their respective financial sector (2013 average for

the selected OIC member countries). This finding in the selected OIC member states conflicts

with what we observe in the US and Europe. For instance, US has a very big non-bank financial

sector compared to its banking sector, where US banking sector asset size is less than 20% of

the total asset size of its financial sector because of a relatively large stock market brokerage

industry, financial derivative industry, asset management and insurance industry in the US

economy. In addition, there is a significant mortgage related financial industry in the US

economy. A similar observation holds true for the European economy. However, in the selected

OIC countries (which can be generalized for the whole OIC states), non-banking sector

including asset management companies, insurance industry, leasing industry are in a

development stage. Financial development literature supports an even distribution among

banking and non-banking industries; therefore there is an important room for improvement

for the non-financial sector in OIC member states.

In Figure 10, we present the total asset decomposition in the OIC members. For the selected

countries, the dominant asset class seems to be the loans as banks from the selected OIC

member countries do hold 39% of their assets in the form of a loan portfolio. This ratio is

lower than that of both US and EU. However, the securities portfolio of the member countries

is lower than that of both US and EU banking system. Banks in the selected member OIC states

hold only 11% of their assets in their security portfolio. This ratio in EU and US is two to three

times higher. The majority of OIC member states hold a significant amount of other assets, as

specified in Bankscope database, which surfaces as an important issue to be investigated in the

following sections. As can be seen in EU banking system, the amount of loans and securities in

EU banking system is higher than that of US banking system. However, general conclusion,

which can be withdrawn from the analysis, is that securities portfolio of selected OIC member

states is relatively small compared to European banking sector, which might be related to the

fact that trading activities in OIC member countries are relatively limited.