46 / 176

46 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

29

for getting ready for the BASEL III rules where most OIC countries seem to be prepared for the

more demanding nature for the quality of bank capital.

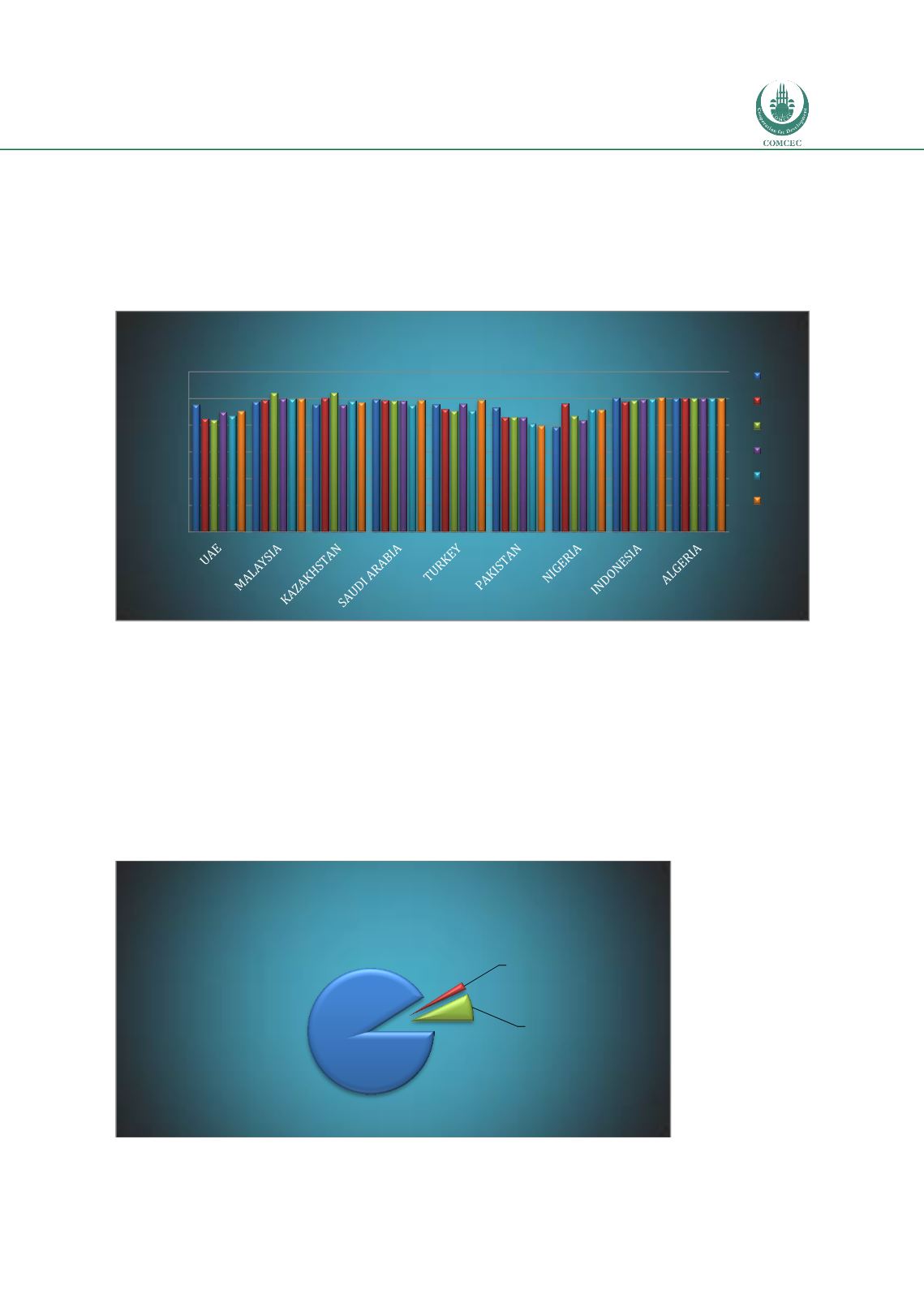

Figure 20 compares the common equity versus total bank capital for the selected OIC

members. Banks on average have more common equity, which is a positive condition for the

quality of capital.

Figure 20: Common Equity-Total Equity Ratio

Source: Bankscope

Decomposition of risk weights with respect various risks is also extremely critical from the

supervisory point of view. Around 90% of the capital is hold against credit risk in OIC member

states, which means that loan portfolio is the main source of banking risk for the OIC members.

This means, loan portfolio is the main source of banking risk for the OIC members. Market and

operational risks have far less weights than that of credit risk. This may be related to the fact

that the relative weight of securities portfolio is small. In addition, standard risk weight

calculations under BASEL II is not risk sensitive and can underestimate the actual market risks.

This is relevant for all OIC members. Operational risk is the second biggest risk, which is

calculated on the basis on banking sector profitability.

Figure 21: Risk-Weighted Assets

Source: Bankscope

0,00%

20,00%

40,00%

60,00%

80,00%

100,00%

120,00%

Common Equity/Total Equity

2008

2009

2010

2011

2012

2013

Risk Weig. Ass.

- Credit Risk

91%

Risk Weig. Ass.

- Market Risk

2%

Risk Weig. Ass.

- Op. Market Risk

7%

Risk-Weighted Asset Decomposition

(for Selected OIC Members)