39 / 176

39 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

22

reducing competition and access to finance, and potentially contributing to future instability as

a result of moral hazard problems associated with too-big-to-fail institutions. However,

Thorsten Beck states (2013), "Risks and dangers in banking arise primarily from a regulatory

framework that is not adapted to the market structure. Large financial institutions turn too-

big-to-fail because the regulator does not have any means to properly discipline and resolve

them. Therefore banking concentration is not an impediment for the OIC member states.

However, adapting the supervision mechanism for this market structure is important.

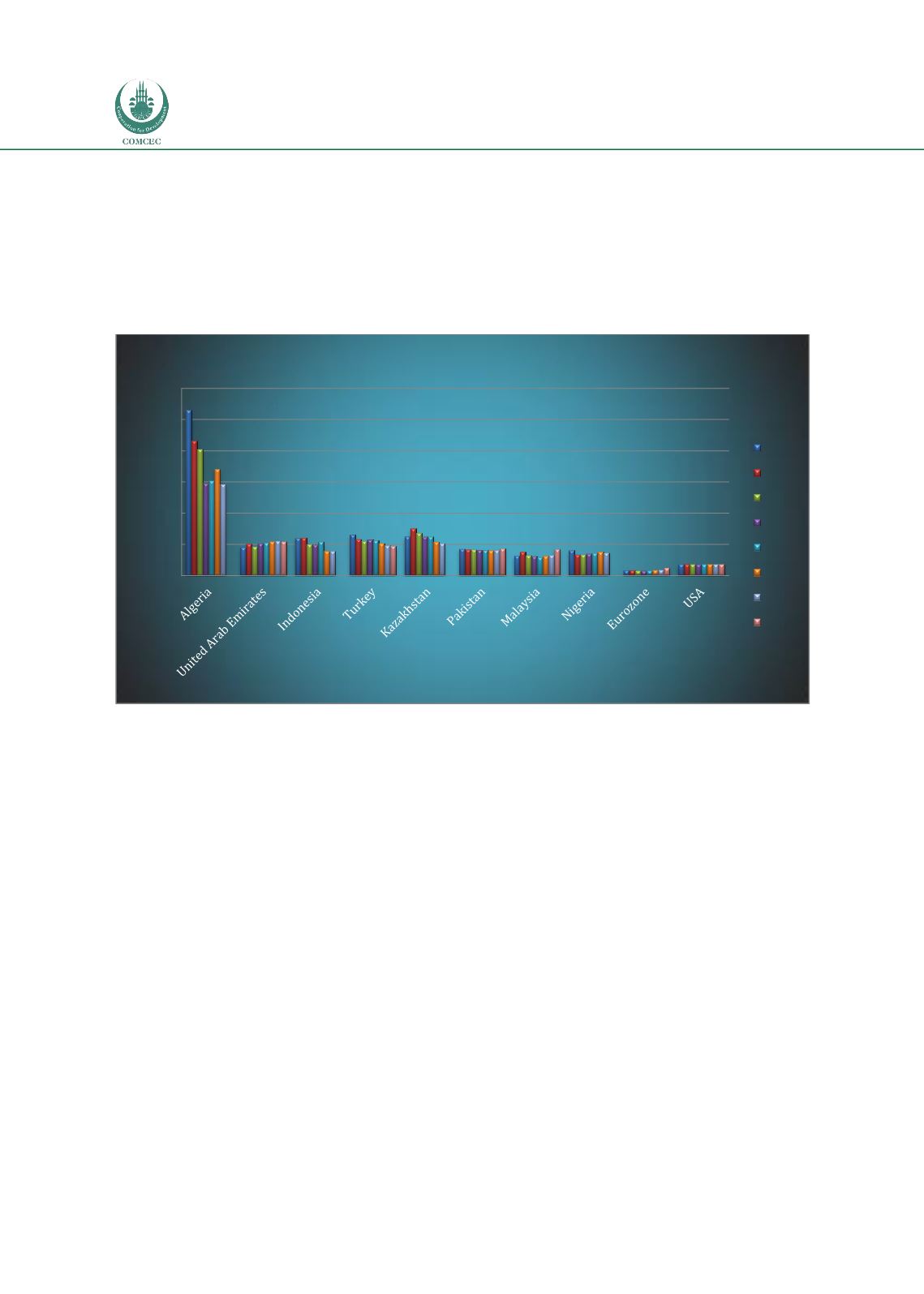

Figure 9: Deposit Concentration: Herfindahl-Hirschman Index

Source: Bankscope

Distribution of banking deposits across banks plays a critical role for a banking system as

concentration among few banks could hinder financial stability. However, concentration

among the selected OIC countries seems to be evenly distributed with Hirschman-Herfindahl

index values lesser than 25% of critical value except Algeria for some years.

3.1.2.3 Banking versus Non-Banking Sector in the Selected OIC Member States

Recent studies on banking and financial development emphasize that the relative size of

banking in the whole financial sector is also important in assisting economic development.

Equity market, mutual fund industry, leasing and factoring industries is critical for a well-

functioning financial system. Furthermore, the use of derivative products and other financial

instruments can be operational in expanding the financial sector. While banking sector is

crucial in supporting for indirect intermediation role in the economy, equity financing and

debt financing are also important for sustainable investment and growth in the real sector. In a

developed financial system, usually there is a balance between the non-banking financial

sector and banking sector.

0%

10%

20%

30%

40%

50%

60%

HHI For Total Customers Deposit

2006

2007

2008

2009

2010

2011

2012

2013