48 / 176

48 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

31

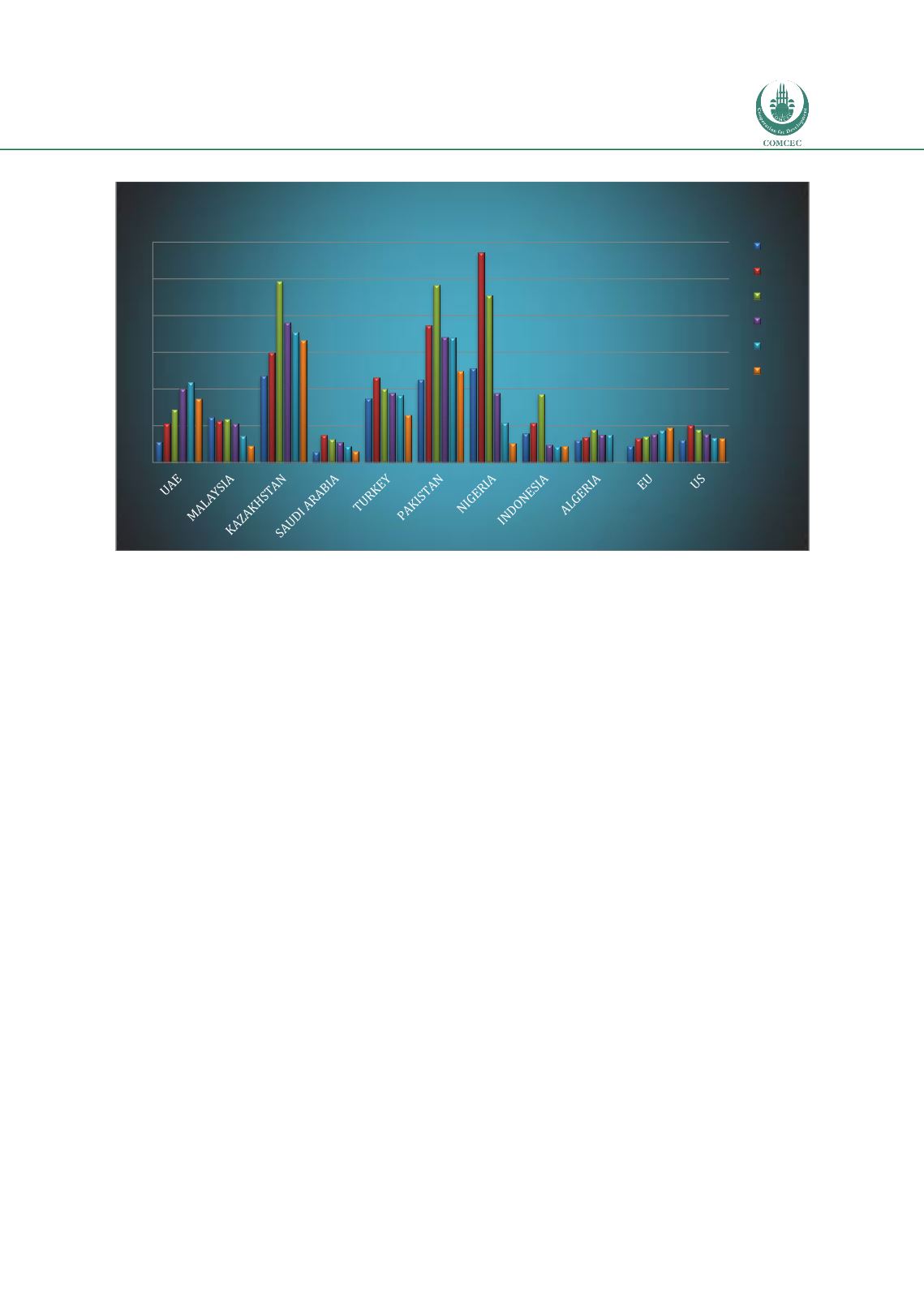

Figure 24: NPL Ratio

Source: Bankscope

Another important measure for the evaluation of the banking sector is the ratio of non-

performing loans. (NPL). For most of the member states, the ratio of NPL’s to total loans

remains below 10% with notable exceptions of Kazakhstan, Nigeria and Pakistan (see Figure

24). In those countries both the level and the volatility of NPL seems to be high. NPL is an

important indicator where high ratios depresses bank profitability and usually lead to further

deteriorations in credit quality. Therefore, high NPL ratio limits the financial intermediation

role of the banks and their ability to raise capital to meet the capital requirements imposed by

the regulatory framework. It is also important to note that NPL ratios increase sharply during

recessions. NPL is in a way a historical measure. More forward-looking measures should be

studied to predict what might happen to the NPL's in the future. Particularly, stronger

collaterals and avoiding concentration risk in lending would be helpful.

The average NPL in OIC member states is around 7%. This is a moderate figure. But it is

important to note that, in 2009 after the financial crisis in US, the NPL figure average was

around 9%. What is critical in this context is to get ready for these types of global or local

shocks. Capital buffers are needed to defend bank runs in these dates. Because of this, a well-

defined stress testing methodology can be applied in OIC member countries.

Loan to deposit ratio is another critical measure for banking deepening and soundness.

Normally, a higher loan to deposit ratio is a good thing for the banking sector development.

However, a very high deposit to loan ratio can be detrimental during a financial crisis. But

majority of the selected OIC member states has a loan to deposit ratio below 100%. This level

does not imply a high level of risk.

0

5

10

15

20

25

30

NPLs/Gross Loans

2008

2009

2010

2011

2012

2013