38 / 176

38 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

21

In addition, the numbers of banking branches in OIC member states are much lesser than that

of developed countries which indicates a relatively lower banking population in OIC member

states compared to US and Europe. However, this may also imply that there is a room for

banking sector development and financial inclusion in the OIC member states.

3.1.2.2 Banking Sector Asset and Deposit Concentration

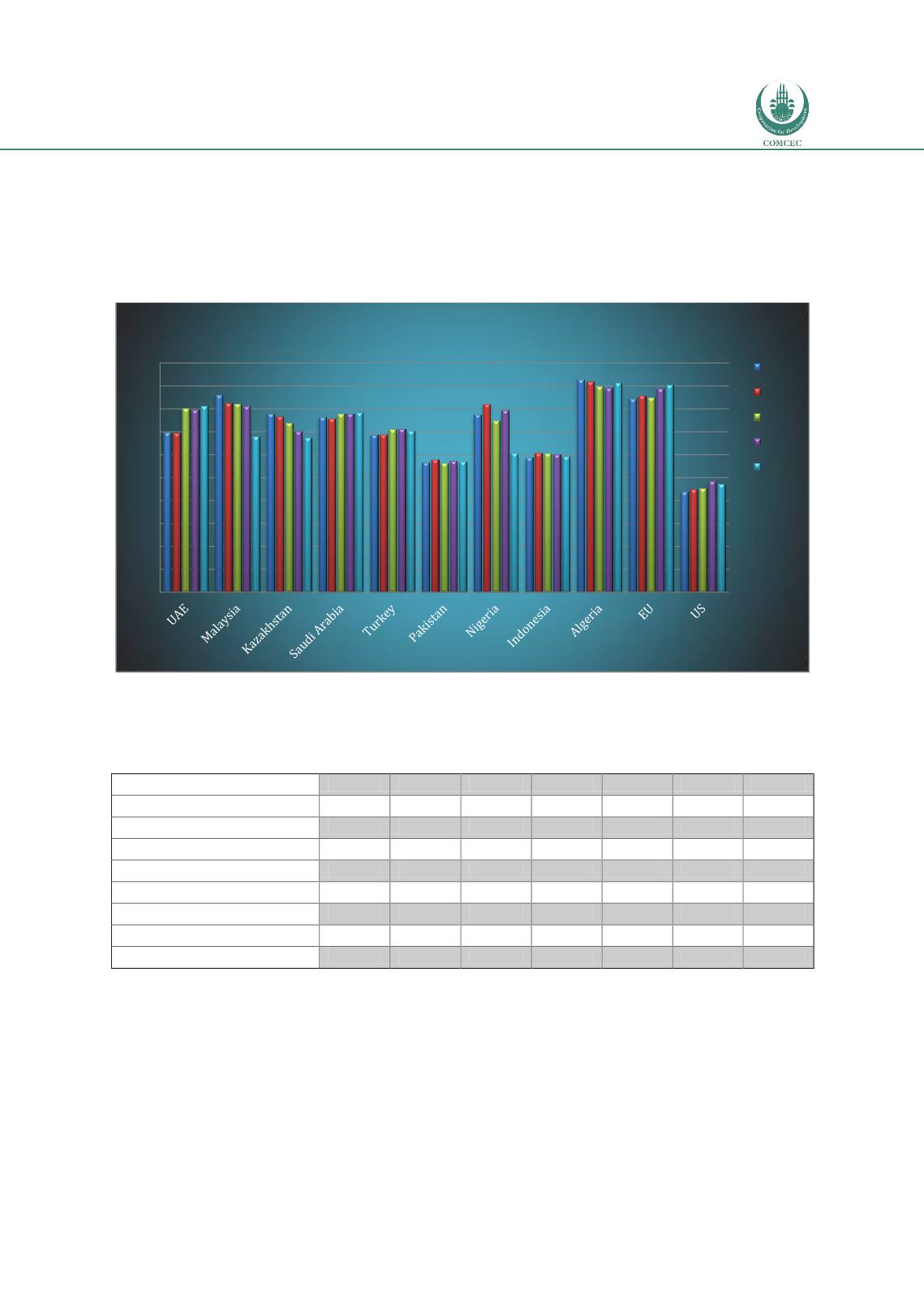

Figure 8: Bank Concentration (percentage)

Source: Bankscope

Table 4: Asset Concentration for the selected OIC countries (Herfindahl Index)

2007

2008

2009

2010

2011

2012

2013

Algeria

0.25

0.23

0.19

0.19

0.19

0.17

N/A

Saudi Arabia

0.12

0.12

0.12

0.12

0.12

0.12

0.12

United Arab Emirates

0.11

0.10

0.11

0.10

0.11

0.11

0.11

Indonesia

0.16

0.13

0.12

0.12

0.12

0.11

N/A

Turkey

0.11

0.10

0.11

0.10

0.10

0.10

0.09

Kazakhstan

0.14

0.12

0.11

0.11

0.10

0.09

N/A

Pakistan

0.08

0.08

0.07

0.08

0.07

0.08

0.08

Malaysia

0.07

0.07

0.07

0.06

0.09

0.07

0.09

Nigeria

0.06

0.06

0.07

0.07

0.06

0.06

N/A

Source: Bankscope

We investigate banks' asset concentration using the Herfindahl-Hirschman index. This ratio

lies between 0 and 1 and an index closer to 1 indicates a higher concentration. 25% is usually

used as a cut-off value for medium level of concentration. As of 2013, none of the OIC member

countries seem to have a banking system with relatively high asset concentration.

The effect of banking concentration on financial stability is not a fully resolved issue. As stated

in a recent World Bank Study (Global Financial Development Report, 2013), some researchers

believe that government support of the largest banks increased banking concentration,

0

10

20

30

40

50

60

70

80

90

100

Five Largest Banks Asset Concentration

2007

2008

2009

2010

2011