143 / 221

143 / 221

Risk Management in

Islamic Financial Instruments

114

5.6 RISK MONITORING

IFIs must ensure the presence of an appropriate risk monitoring environment. IFIs have to

continuously monitor the collateral taken against different modes of financing. Risk ratings

should be analysed regularly. IFIs must have a system in place that enables them to monitor

the rates of commodities, currencies, and the returns offered by other banks. One of the typical

items that can be used to monitor the business risk of clients is to have a detailed idea of the

type of businesses in which its clients are involved. Consequently, quarterly or monthly

performance data can be collected from clients and can be adjusted with the market

performance in order to further analyse upcoming challenges. A number of components are

involved in this decision. Table 5.5 offers a description of the set of prerequisites. Around 50

percent of the banks do not reappraise the collateral unless it is required. One third of these

banks do not regularly check the status of the guarantor. Half of the sample banks have never

conducted a country risk rating. Major emphasis is given on analysing the business

performance of the borrower, which is the most traditional of all pre-requisites.

Table 5.6: The Prerequisites to Risk Monitoring

Issues

Never (%)

Occasionally (%)

Regularly (%)

Appraisal of the collateral

16.7

27.8

55.6

Confirming guarantor's intention

11.1

22.2

66.7

Review country ratings

50.0

11.1

38.9

Review borrower's business performance

11.1

5.6

83.3

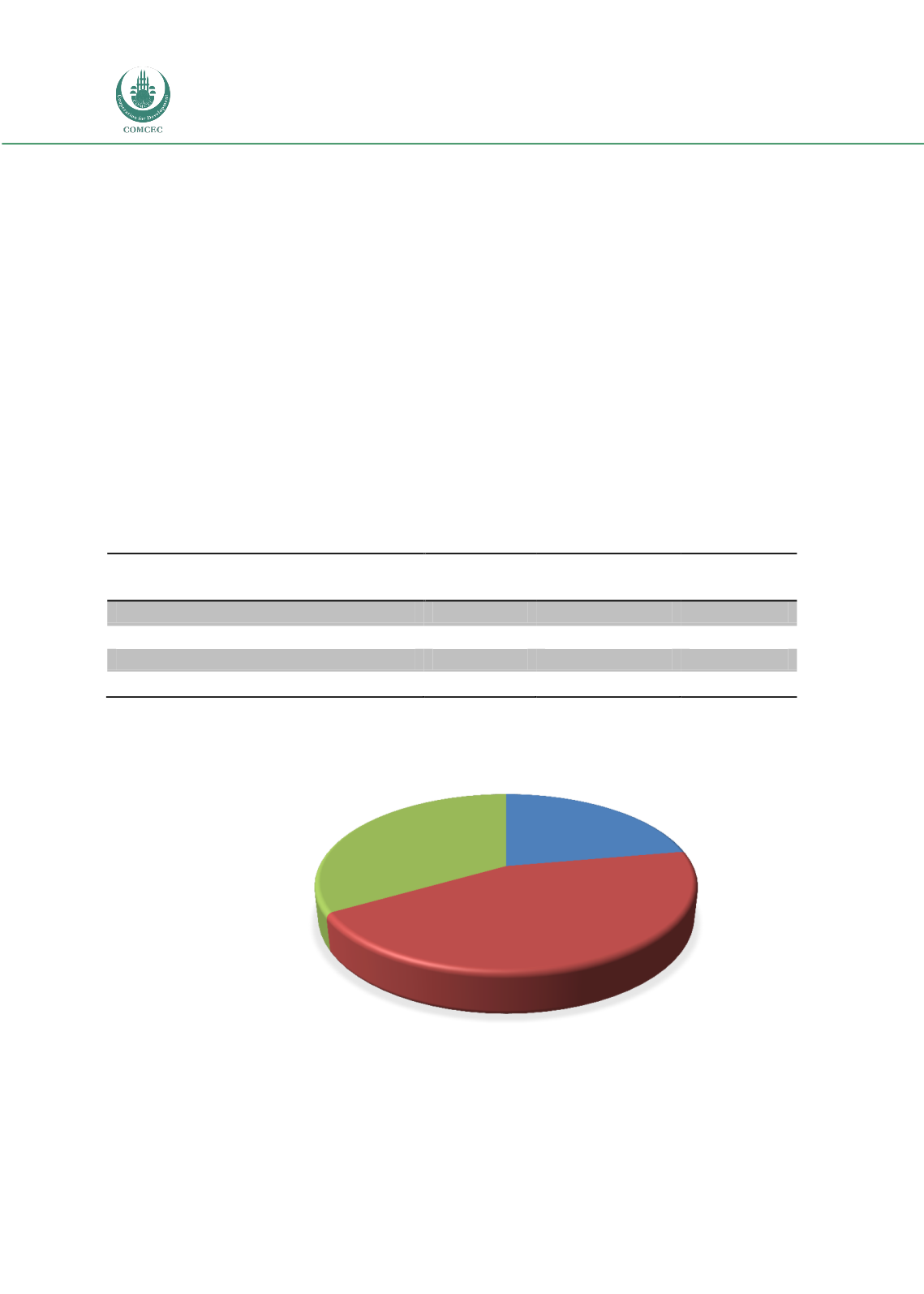

Figure 5.5: Use of Accounting Reporting System

The use of an accounting system affects the style of financial reporting. Different countries use

different reporting and accounting systems. The most popular among these systems is the one

provided by AAOIFI. This Bahrain-based organization provides standards for accounting-

International

22%

AAOIFI

45%

Others

33%