148 / 221

148 / 221

Risk Management in

Islamic Financial Instruments

119

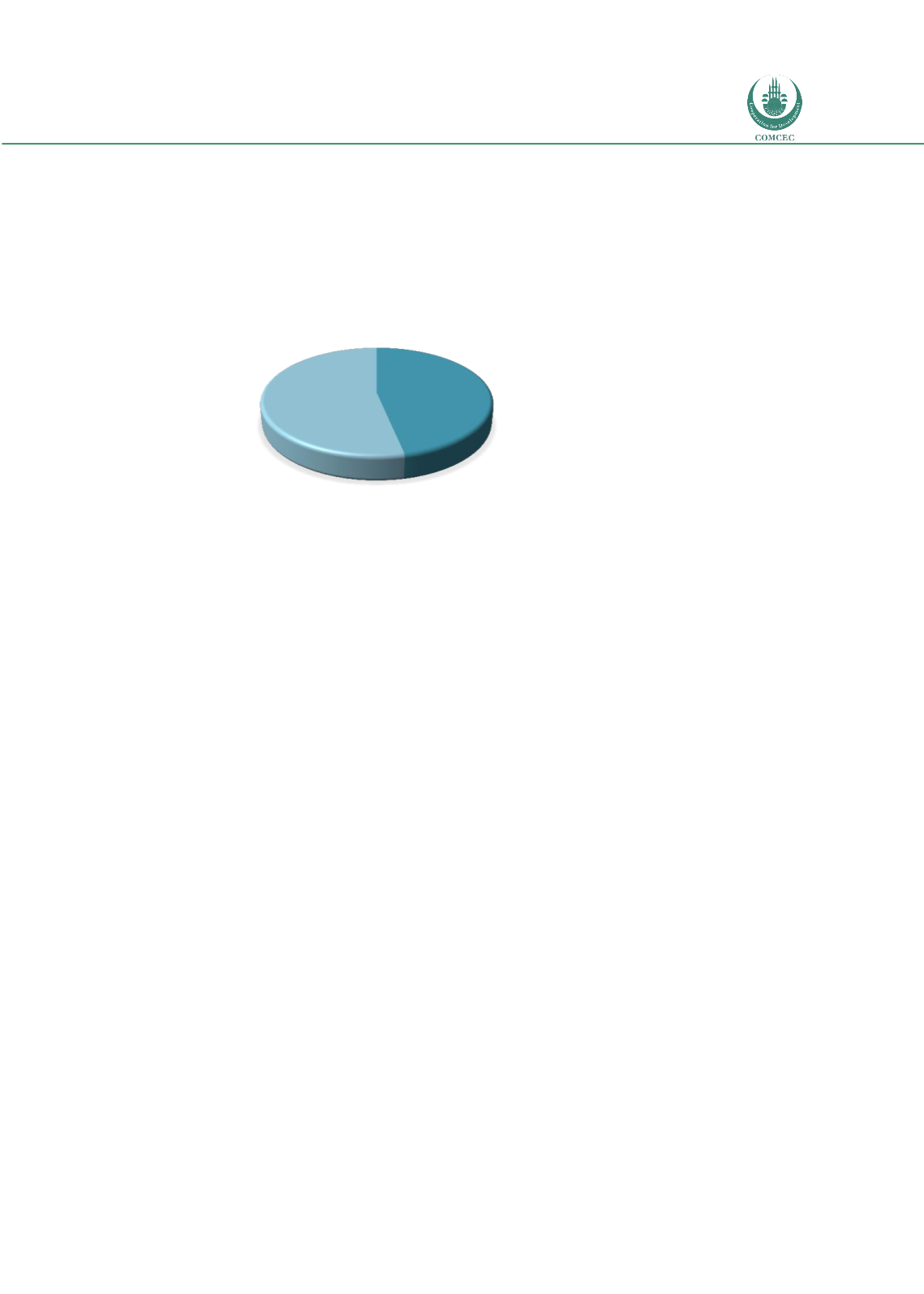

indicates room for development in the internal and external systems of the Islamic financial

systems in terms of strengthening internal mechanisms and widening cross border banking

with other countries.

Figure 5.11: Satisfaction with Existing RM System

5.10 REACHING THE OBJECTIVES OF SHARI’AH

The benefits of the Islamic financial system are already well established in financial systems.

Among many, the system does not allow unnecessary profit making, unadjusted for risk, and

the system promotes social development through partnership and entrepreneurship. Risk is a

part of any business, but IFIs cannot take any investment activity where the risk is excessive.

Perhaps this is the reason that saved the Islamic system from the recent crisis of 2007-08. That

is how the IF system started gaining momentum among Muslims and non-Muslims.

Risk management at IFIs is primarily proactive. The system does not allow any speculative,

highly risky engagement in gambling by bankers. In addition, the partnership nature of the

contracts allows the parties involved to share the risk and profits, based on agreed upon ratios.

Hence, it becomes the responsibility of the parties, not only the IFIs, to ensure the cost of the

risk. In fact, the risk sharing mechanism is already integrated in the system. As a secondary

proactive mechanism, IFIs must establish effective internal mechanisms to continuously look

for loopholes in the system. In addition to internal control systems, IFIs are equally open to

control by internal auditors and the scrutiny of the

Shari’ah

supervisory board.

The tertiary level of the risk management system comes from the use of derivative techniques,

which is heavily criticized in the Islamic financial system. These are proactive mechanisms to

risk management. Finally, the last resort of risk management rests with external stakeholders.

These external stakeholders include the Basel committee and the central bank of each country.

Figure 5.12 illustrates the risk management framework of IFIs.

Shari’ah

principles at the very

core and the supervisory board clearly differentiate the uniqueness of IFIs, compared to

conventional banks. Overall, in theory, if the system works, IFIs should be more resilient to risk

than their conventional counterparts.

Yes

47%

No

53%