90 / 176

90 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

73

5.4 Profitability in Islamic Banking

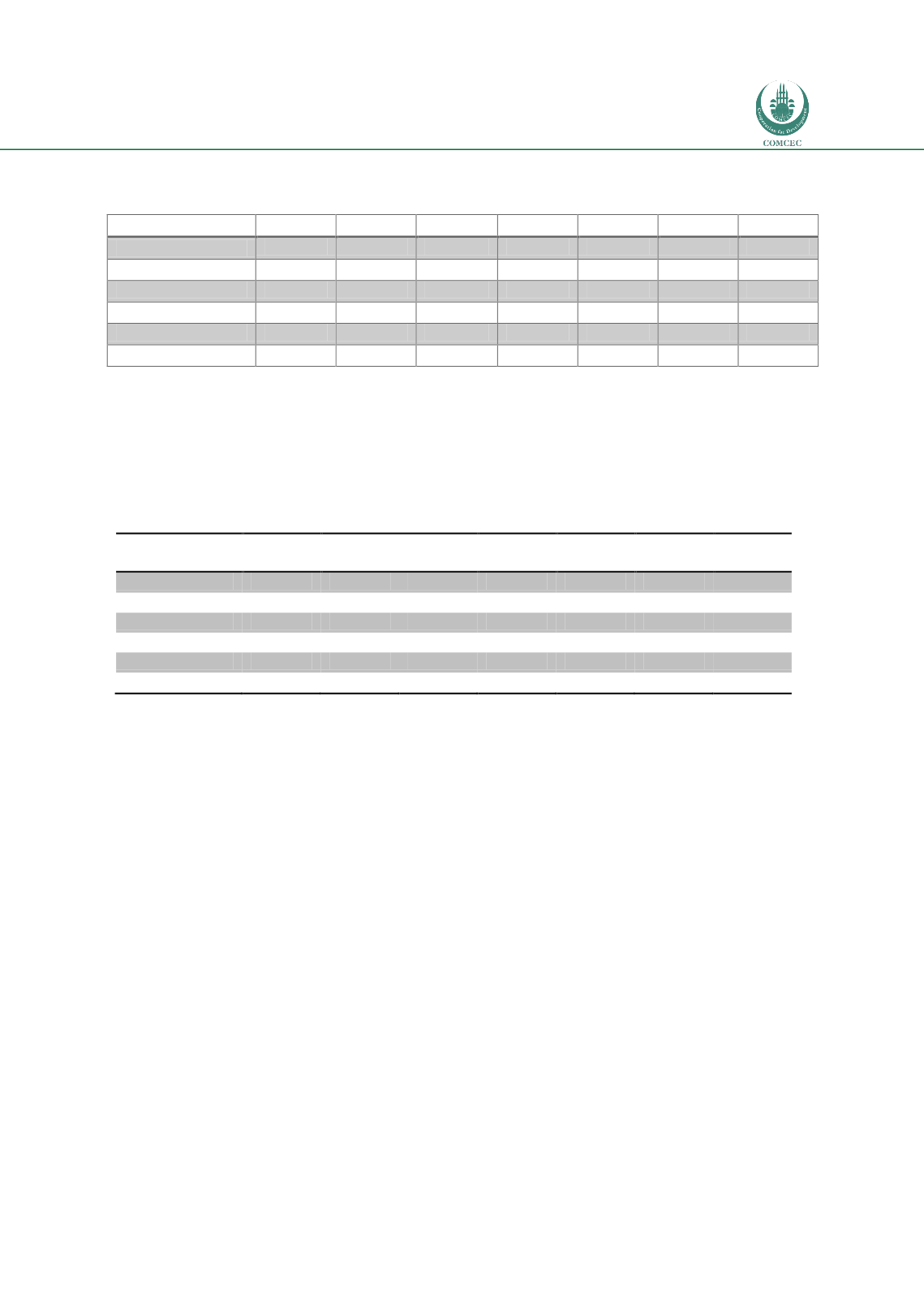

Table 36: ROA, Islamic Banking

2007

2008

2009

2010

2011

2012

2013

Turkey

2,78

3,05

2,25

1,91

1,57

1,40

1,27

Indonesia

3,83

2,26

0,68

0,83

1,23

1,38

0,96

Malaysia

0,23

0,51

0,62

0,64

0,06

0,78

0,95

Pakistan

0,96

0,95

0,19

0,72

1,57

1,40

3,57

S.Arabia

3,07

3,20

1,63

1,45

2,12

2,71

2,22

UAE

3,44

1,42

-0,57

0,02

0,59

0,91

1,10

Source: KFHR

Banking profitability is one of the most important indicators for banking soundness.

Comparing the profitability of the Islamic banks with conventional banks in OIC member

countries, we observe a similar pattern. Even though conventional banks on average have a

relatively higher return on assets, return on assets (ROA) of Islamic banking is also

satisfactory.

Table 37: ROE, Islamic Banking

2007

2008

2009

2010

2011

2012

2013

Turkey

22

23

17

15

14

14

14

Indonesia

16

18

9

11

9

12

14

Malaysia

13

7

9

10

6

11

13

Pakistan

5

3

-1

1

8

8

7

S.Arabia

16

11

6

9

12

17

14

UAE

18

10

-4

0

4

6

8

Source: KFHR

Return on equity figures in Islamic banking for the selected OIC member countries appear to

be, generally, double-digit numbers. These figures are comparable with conventional banking

in the same countries and better than many of the European and US banks. Therefore, one can

conclude that Islamic banking in OIC countries currently produces a sustainable profit. This

observation confirms the findings of Thornbeck et al (2013).

5.5 Liquidity Risk in Islamic Banking

Basel III liquidity risk requirements may negatively affect Islamic banks, since Islamic money

market instruments are traded in relatively illiquid markets. Therefore, Islamic banks may find

it difficult to attain the Liquidity Coverage Ratio, which requires a large portion of assets to be

held in the form of short-term maturity. Liquidity levels of the banks in the selected OIC

member countries are provided in Table 38, which shows that liquidity ratios of almost all

countries seem to be better than conventional banks. Despite current statistics, Liquidity

Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) of the new Basel III may be a

problem for Islamic banking.