92 / 176

92 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

75

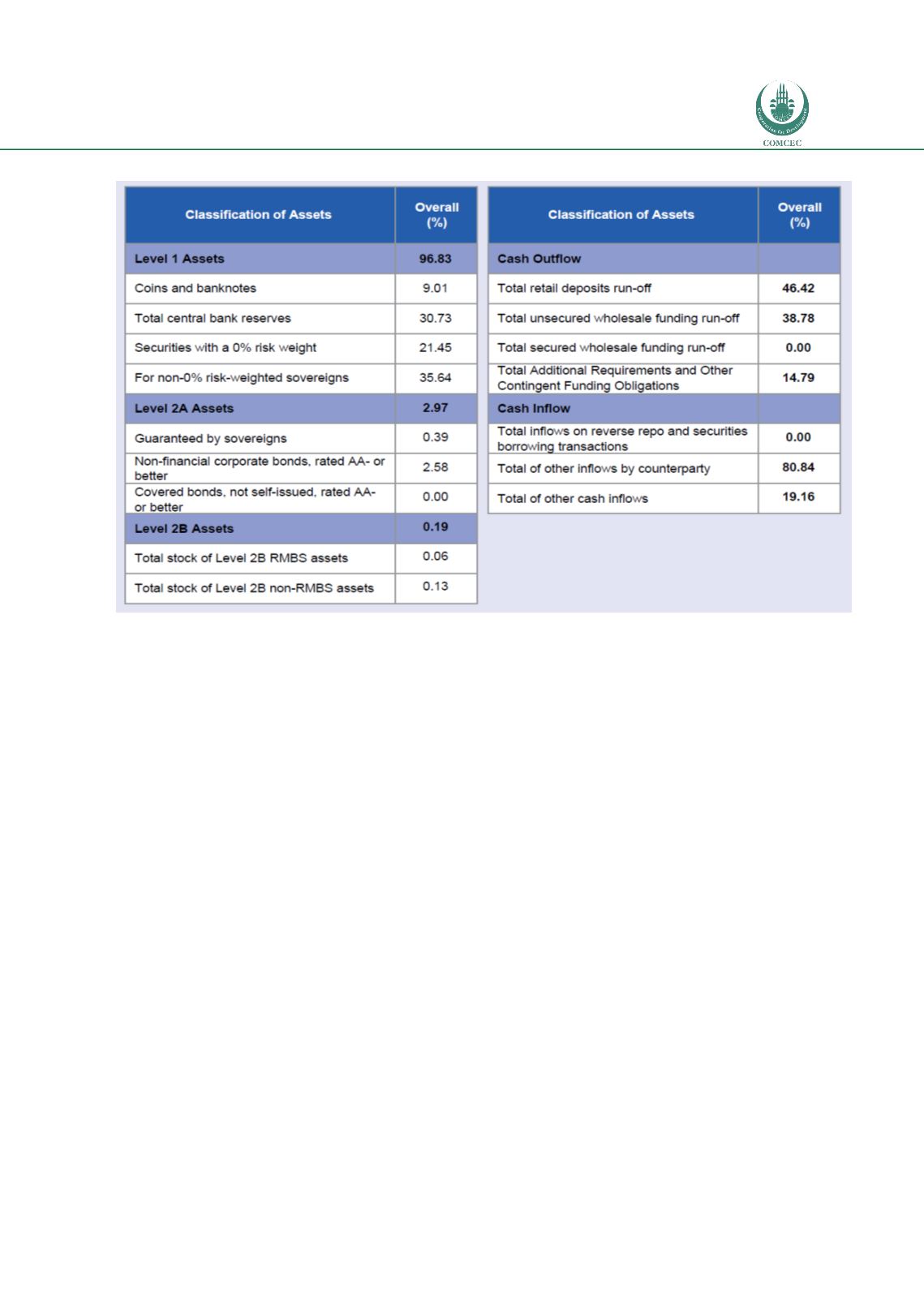

Table 39: Islamic Banking Asset Classification

Source: IFSB, 2014

A QIS made on Islamic banking on LCR is presented above. The majority of Islamic banks can

comply the LCR requirements, but mainly with cash or central bank reserves. This is

satisfactory, but might lead these banks to lose their liquidity flexibility.

5.6 Market Risk and Derivative Use in Islamic Banking

Market risk measurement and management has always been at the core of banking regulation

and supervision. Historically, market risk sourcing from trading book businesses is less

important in Islamic banks than they are in conventional banks. This is because a non-

negligible part of the derivatives instruments used are not Shariah-compliant and short selling

is not allowed. As a consequence, Islamic banks will not see their market risk affected by the

changes in Basel III regulation. This is also true for the use of derivative and structured

products. As we discussed before, only 4% of the global derivative use can be related to Asia-

Pacific countries. These new changes will have a much more severe effects on the European

and the US banking sectors.

However, as Harzi (2012) points out, the products in the quasi trading books (as Salam and

istisna contracts) may be affected mainly due to the fact that it is commodity structured

products with a price that depend on the volatility of the markets. He further claims that the

volatility will have a major impact on the stress-test scenarios and will increase the capital

requirements due to the price fluctuations of the assets. In addition, Islamic banking would not

experience a negative effect of Basel III on the extra charges stemming from the counter party

risk or stress VaR, since Islamic banks do not hold CDO, CDS, repos or interest rates swaps in

their portfolios. However, a major quantitative impact study will be needed to see the gap

between the current state and the future needs of Basel III.