91 / 176

91 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

74

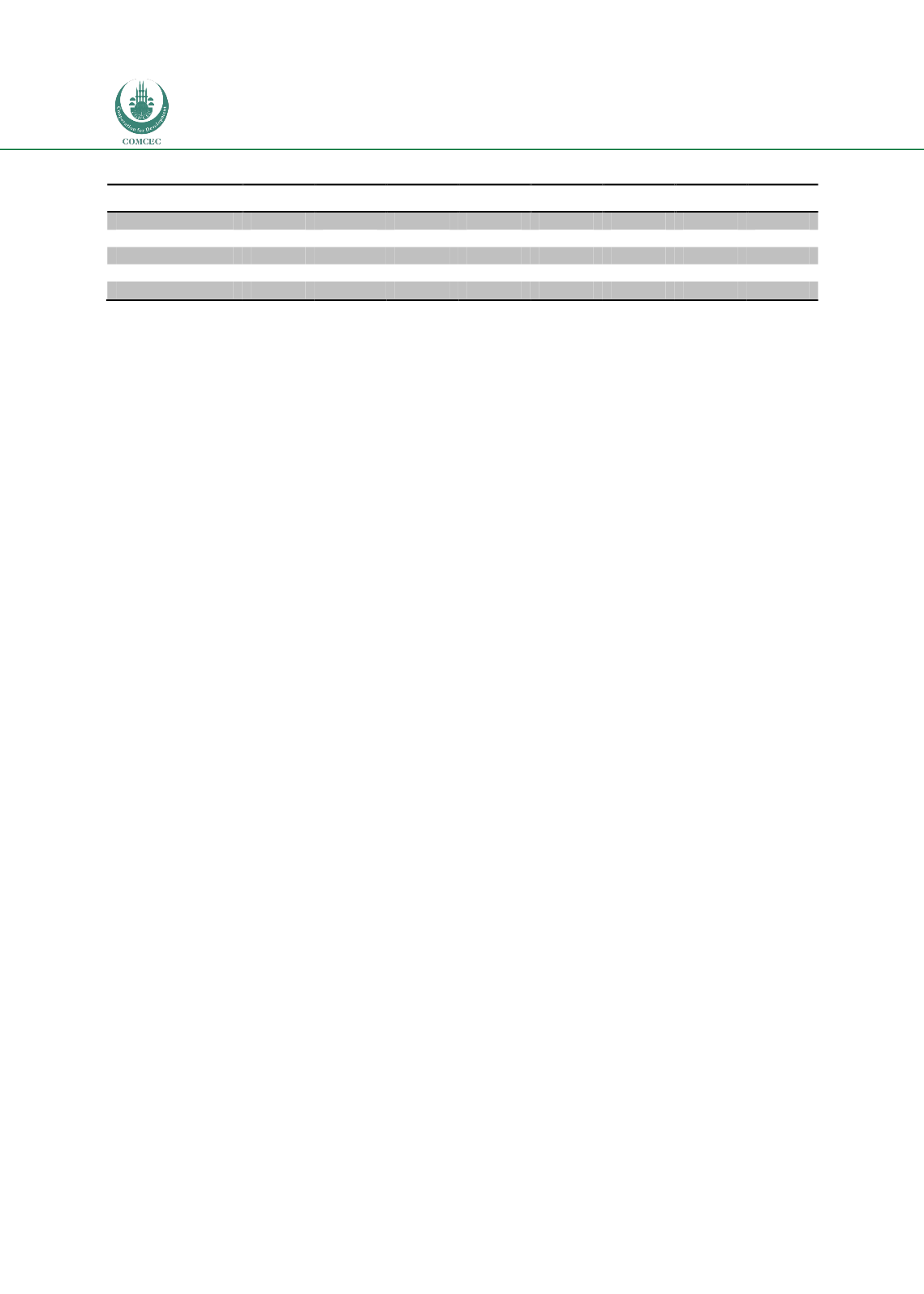

Table 38: Islamic Banking Average Liquidity Ratio

2005

2006

2007

2008

2009

2010

2011

2012

Turkey

82

90

91

84

86

79

86

85

Malaysia

60

91

90

60

55

56

58

57

Saudi Arabia

58

91

100

90

93

89

77

75

UAE

74

72

65

63

61

67

66

69

Pakistan

95

120

103

90

93

148

123

95

Source: IFSB

-

Coordination and Cooperation in Islamic Banking

Even though the current liquidity level of the selected member countries is satisfactory, in the

future, relatively more liquid Islamic money market instruments will be needed. In this

context, one welcome development was the establishment of the Islamic Financial Services

Board (IFSB) in 2003. Since its establishment, the IFSB has issued 22 standards and guiding

principles. The last principle is related to Shariah-compliant money market instruments with

primary objective to issue Shariah-compliant financial instruments in order to facilitate more

efficient and effective liquidity management solutions for Islamic financial institutions, as well

as to facilitate greater investment flows of Sharia-compliant instruments across borders.

To conclude, by referring to the Islamic Financial Services Industry Stability Report (2014), the

liquidity side, the challenge is to give Sukūk the features of high-quality liquid assets (HQLA) to

meet Basel III requirements regarding the Liquidity Coverage Ratio (LCR). This necessitates a

deep and liquid secondary market and fixed-income paper with no price risk. On the

capitalization side, the challenge is to give Sukūk the features of loss-absorbing capital to meet

the Basel III requirements for additional Tier 1 and Tier 2 capital.

The Dubai Financial Services Authority (DFSA), for example, while appreciating the prompt

work on the part of the IFSB in issuing the revised capital adequacy standard for IIFS (IFSB-

15), believes that Islamic banks are not likely to find it overly challenging to comply with the

enhanced capital requirements coming out of Basel III, though they might find meeting the

enhanced liquidity requirements relatively more challenging.

-

Regulatory Challenges

Legal and Regulatory Challenges in Islamic Finance

There are certain specific and unique challenges facing the Islamic finance industry. These

challenges include Shariah compliance and governance, and form versus substance in Islamic

financial transactions.

The IFSB (2014) report on the results of a Quantitative Impact Study (QIS) states, "Overall, the

QIS findings also highlighted a number of major problems for the IIFS, such as: insufficient

Sharī`ah-compliant High Quality Liquid Assets (HSLA) in the Islamic finance jurisdictions, and

lack of a deep and active secondary market for Sharī`ah-compliant HQLA for IIFS to manage

their liquidity.