85 / 176

85 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

68

Sharia-compliant finance does not allow charging of interest payments (riba), as only goods

and services are allowed to carry a price. In addition, Islamic banking does not have room for

speculation, and prohibits financing of specific illicit activities. Another important

characteristic of Islamic banks is that trading in financial risk products, such as derivative

products, is not used. In addition, diversifying debt instruments with Islamic financial products

could be beneficial for OIC members’ treasuries. Therefore, it will be more challenging to find

the impact of recent financial regulations for the banking sector, which are under Shariah-

compliant regimes. In this section, we will discuss Basel III rules and regulations and how they

will change regulatory and supervisory aspects of Islamic banking compared to conventional

banking. Our analysis is based on the following categories: Common equity changes, Credit

Risk, Liquidity Regulations, Leverage and Derivative Use and Capital Conservation Buffer and

Countercyclical Buffer.

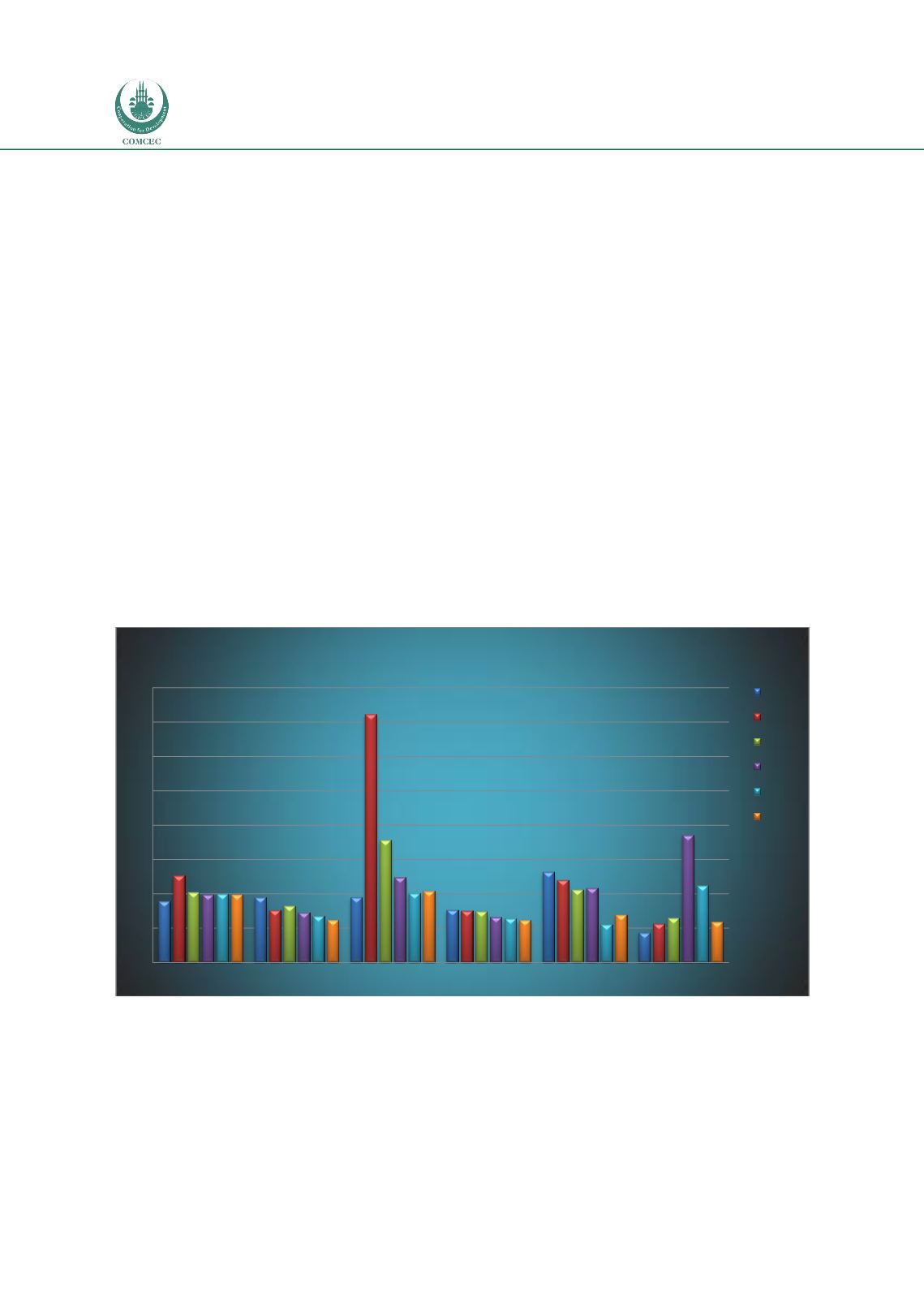

5.1 Capital in Islamic Banking

We compare capital adequacy ratios (CAR) for Islamic banks with those of the conventional

banking sector. In Malaysia, CAR ratios of Islamic banks are similar to conventional banks;

therefore, regulation of Islamic banking does not require any additional measures. In Saudi

Arabia, CARs of Islamic banks were relatively lower than the CARs of conventional banks in

2008; however, over the last few years, Islamic and conventional banks have exhibited similar

CAR ratios. The general observation of similar CAR ratios for the Islamic conventional banking

sector also holds true for the Turkish banking sector.

Figure 43: Islamic Banking Tier-1 Capital Ratio

Source: KFHR

0

10

20

30

40

50

60

70

80

UAE

MALAYSIA SAUDI ARABIA TURKEY

PAKISTAN INDONESIA

Islamic Banking Tier-1 Capital Ratio

2008

2009

2010

2011

2012

2013