51 / 176

51 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

34

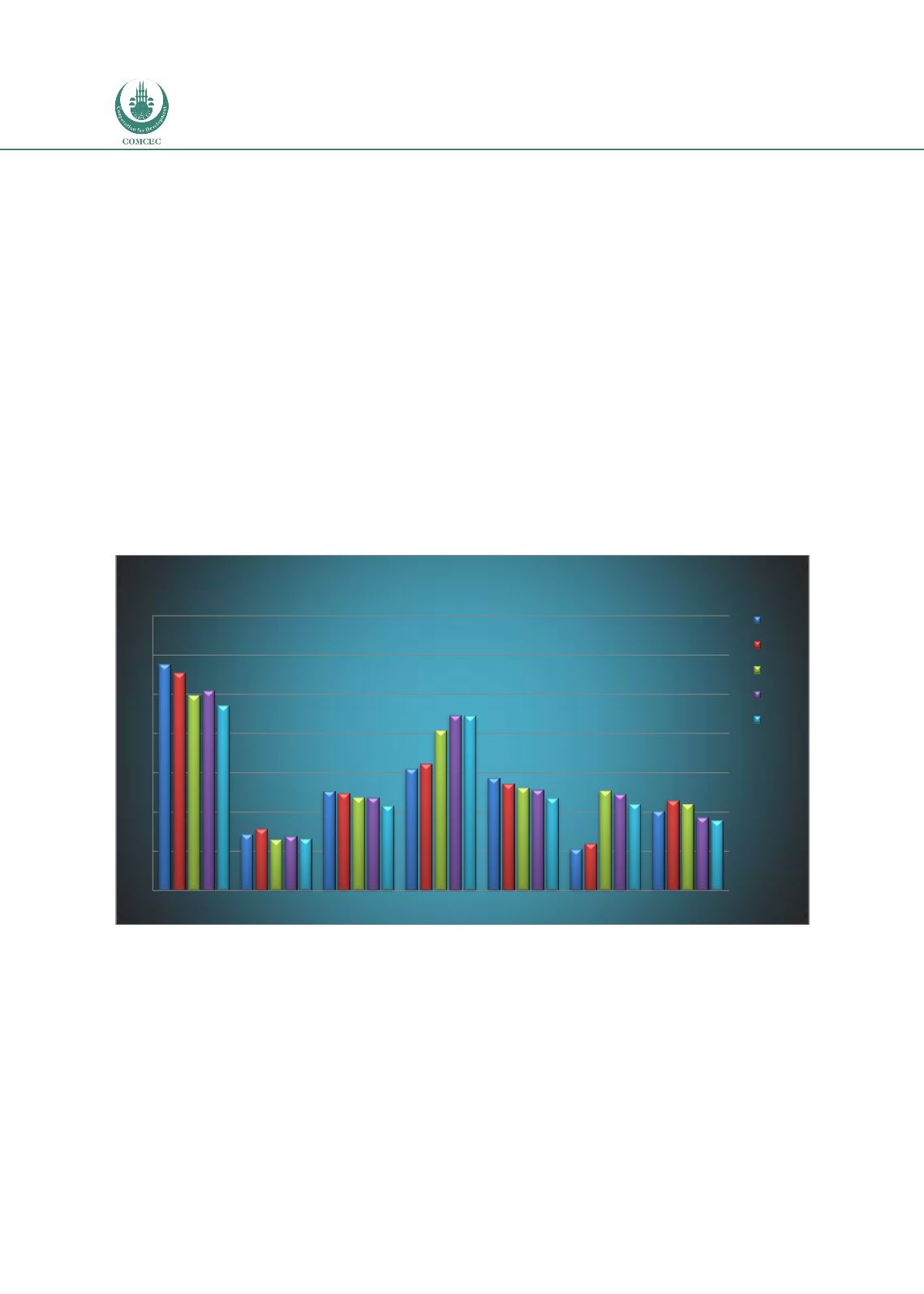

3.1.5 Liquidity Risk and Basel III in Selected OIC Countries

In terms of the ability of liquid funds to cover short-term needs of banks, we focus on the ratio

of liquid assets to the short-term liabilities. For this measure, Turkey and Pakistan reach a

level above 80%, which is in line with the ratio in US. For other member states used in the

analysis, we observe ratios ranging between 25%-60%.

Liquidity conditions in the financial markets are crucial for a well-functioning banking system

because during the times of financial stress, we observe quick and severe evaporation of

liquidity putting banks into difficulties. In this regard, BASEL III imposes new constraints on

the amount of liquid assets banks need to hold to match both short and long-term cash

outflows. Figure 29 and Figure 30 present the ratio of liquid assets to total assets and to short-

term liabilities of the banking system in the member states for which data are available, in a

comparison to the Euro area and US for the period 2008-2014. These measures do not directly

comply with LCR or NSFR however; they still provide a clear picture of liquidity conditions

from a comparative perspective. The fraction of liquid assets to total assets vary between 15-

30% for Malaysia, Kazakhstan, Nigeria, Indonesia and Saudi Arabia which are mostly above the

corresponding ratio in US. Turkey and Pakistan are positively separated in this measure with a

ratio above 40%.

Figure 29: Liquid Assets over Total Assets

Source: IMF-FSI

0

10

20

30

40

50

60

70

Turkey

Malaysia Saudi Arabia Pakistan Indonesia

Nigeria Kazakhistan

Liquid Assets to Total Assets

2009

2010

2011

2012

2013