89 / 228

89 / 228

Infrastructure Financing through Islamic

Finance in the Islamic Countries

73

sectors. For example, Bank Indonesia, Ministry of Finance, Ministry of Religious Affairs,

Indonesian National Zakat Body (Baznas) and the Association of Productive Waqf (FWP) are

developing models of waqf-linked sukuk and sukuk-linked waqf. While the former utilizes cash

waqf to build social infrastructure (public schools, hospitals, etc) by purchasing government

sukuk (SBSN), the latter plans to use land waqf as the underlying asset to issue sukuk to

construct public (social purpose) buildings on the land.

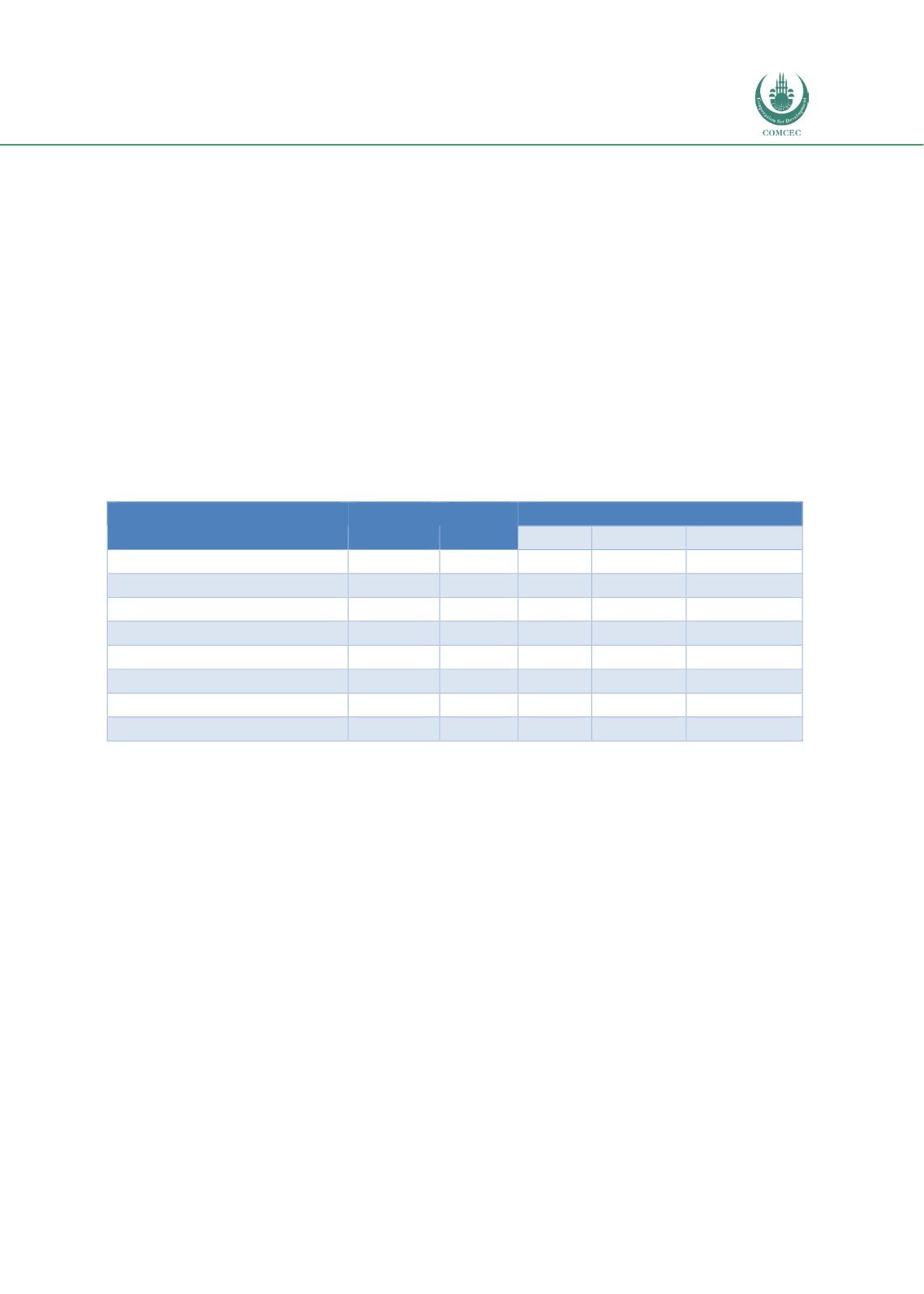

The growth and current status of the different sectors of Islamic finance are shown in Table

4.1.1. Islamic financial markets have outpaced financial institutions in terms of both value and

as a percentage of GDP. Up to December 2017, government Sukuk (called SBSN) has dominated

the industry and has captured nearly 17% of the market share, and this is followed by Islamic

nonbanks (Islamic cooperatives, Islamic pension funds,

Baitul Maal Wattamwiil

(BMT), etc)

owning an almost 11% share of the total industry. Meanwhile, Islamic securities, Islamic

financing companies and Islamic banks have gained 6.16%, 6.34% and 5.56% of the market

shares of their corresponding sectors respectively.

Table 4.1. 1: Development of Islamic Finance Sectors (in USD billion)

Type of Industry

2013

2015

2017

June

December

Share (%)*

Islamic banking

17.72

21.16

27.01

30.30

5.56

Islamic insurance

1.19

1.89

2.67

2.89

3.4

Islamic financing

1.78

1.63

2.77

2.46

6.34

Islamic non-bank

0.57

1.11

2.25

1.72

10.99

Corporate Sukuk

0.54

0.71

1.08

1.23

4.3

Islamic mutual funds

0.67

0.79

1.35

2.01

6.16

Government Sukuk

12.09

21.15

35.94

39.40

16.97

Stock market capitalization

182.70

185.77

249.39

264.39

Source: Bank Indonesia (2017)

*Share of Islamic finance relative to total.

In terms of value at the end of 2017, the sukuk market is the largest, valued at USD 40.63

billion (USD 39.4 billion sovereign and USD 1.23 billion corporate) followed by the Islamic

banking industry with total assets valued at USD 30.2 billion, Islamic insurance has assets

worth USD 2.8 billion and the Islamic nonbank financial institutions sector is worth USD 24.14

billion. From the periods of 2013 to 2017, the total number of Islamic mutual fund companies

increased 29% to include 181 companies, with the total growth of net asset values (NAB) of

31% valued at IDR 28.31 trillion (USD 2 billion).

4.1.2.

Current Status and Projected Investment in Infrastructure Sectors

Chart 4.1.3 shows the status of infrastructure in Indonesia relative to the OIC countries and the

East Asia and Pacific (ES&P) region. While the statuses of the overall infrastructure and its

quality in Indonesia (4.5 and 4.1 respectively) are better than that of the OIC countries (3.6 and

3.7 respectively), they are poorer compared to the statuses of the EA&P region (4.9 and 4.6

respectively). Similar trends can be seen for electricity and telephony infrastructure. However,

the transport infrastructure in Indonesia (4.7) is better than both the OIC countries (3.5) and

the EA&P region (4.6).