95 / 231

95 / 231

Diversification of Islamic Financial Insturments

81

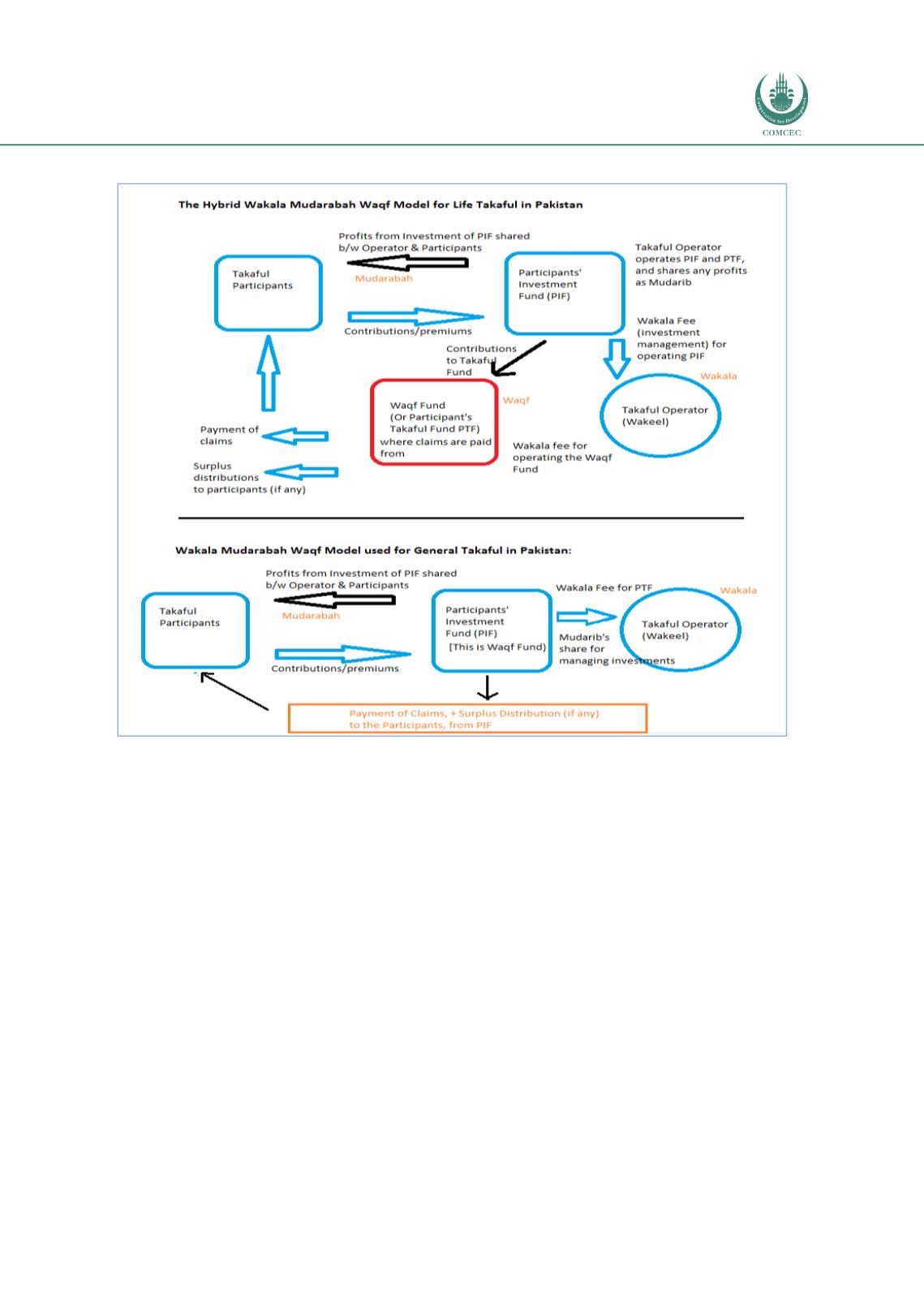

Figure 11. Hybrid Wakala Waqf Mudarabah Model Used in Pakistan

Source: Created by Author

In contrast, in General Takaful, there is no separate PTF, and the Participants’ Investment Fund

itself acts as the Waqf fund.

In both business models, the income of the Takaful operator is both in the form of a Mudarib

(for managing the investments of the PIF) and as a Wakeel (fixed percentage fee charged for

operating the Waqf fund). In cases where there is a surplus in the Waqf fund (contributions

exceeding claims in a financial period), with the approval of the Shariah Board of the Takaful

Operator, the surplus is either

Used to pay back any Qard-Hasan from shareholders, taken previously in case of

deficit

A portion of the surplus is kept as a reserve, to mitigate for future losses.

The remaining portion is distributed among the participants of the fund

Note that, as per SECP regulations, it is not incumbent for Takaful operators to have a Shariah

Board. The minimum requirement is that of one qualified approved Shariah Advisor. However,

a few full-fledged operators such as Pak Qatar Takaful and Dawood Family Takaful have their

own Shariah Boards.