94 / 231

94 / 231

Diversification of Islamic Financial Instruments

80

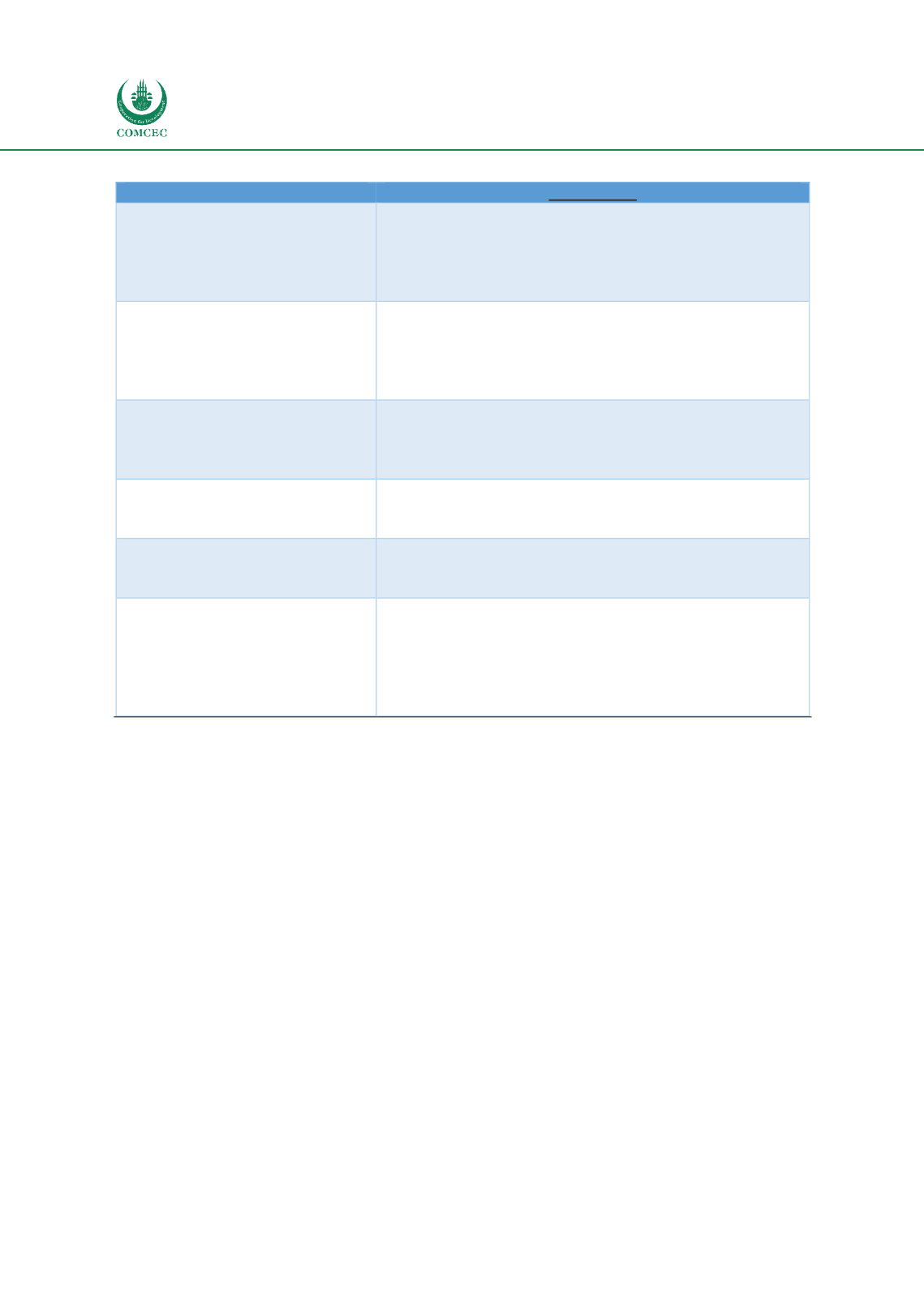

Table 35. Financial Instruments Used in Takaful Industry in Pakistan

Description

Minimum Capital Requirements

For Life Takaful: PKR 700 million

For General Takaful: PKR 500 million

Paid up capital requirements make it easy for Insurance

companies to commence Window Takaful operations in

Pakistan, since 2015

Shariah Governance

requirements

Minimum one qualified resident Shariah Advisor for both

Life and General Takaful, full-fledged and Windows.

Advised but not necessary to have a Shariah Supervisory

Board. Pak Qatar and Dawood Takaful have Shariah

Supervisory Boards.

Model used for Life/Family

Takaful

Hybrid Wakala-Waqf-Mudarabah model used. Takaful

operator acts as Wakeel for Waqf fund (or Participants

Takaful Fund PTF, from which claims are paid), and

Mudarib for Participants Investment Fund.

Model used for General Takaful

Hybrid Wakala-Waqf-Mudarabah model used.

Unlike Life Takaful, there is no separate Participants

Investment Fund (PIF) and PTF in general Takaful.

Products offered in Life Takaful

Individual life insurance

Group Life insurance

Banca Takaful group Life insurance

Products offered in General

Takaful

Health insurance

Group health insurance

Motor takaful

Fire takaful

Marine Takaful

Engineering Takaful

Source: Annual Reports, Pak Qatar Family Takaful 2015, Pak Qatar General Takaful 2015.

In Pakistan, following the development of Takaful Rules in Pakistan in 2005, the Wakala-

Mudarabah-Waqf model was developed. This was partially in response to criticisms of earlier

models such as the Wakala-Mudarabah model (e.g. regarding the ownership of the Takaful

fund being with the operator), and Mufti Muhammad Taqi Usmani suggested declaring the

Takaful Fund a Waqf. The full hybrid model, called Wakala-Mudarabah-Waqf model, is now

used for both Life and General Takaful in Pakistan, and has been approved along with Waqf

deed by the SECP. A depiction is given in the Figure (Hybrid Wakala Waqf Mudarabah model)

below.

As the figure below explains, the main difference between the model used in Life Takaful and

General Takaful in Pakistan is the existence of a separate Participants’ Takaful Fund (PTF) in

Life/Family Takaful. This is the Waqf fund from which all participants’ claims are paid. Note

that when the participants or beneficiaries pay their risk coverage Takaful premiums, they are

first transferred to the Participants’ Investment Fund (PIF), and then only a fraction is

transferred to the PTF. The Waqf deed stipulates that, once funds are transferred to the Waqf

fund (as the ownership of this fund is neither with the Operator nor the Participants, but with

Allah alone), they cannot be withdrawn for any purpose other than that of the establishment of

the fund. All claims of participants for their risk coverage are paid from this Waqf fund. If a

client withdraws or the policy matures, he/she gets the remaining balance from PIF as well as

PTF.