101 / 231

101 / 231

Diversification of Islamic Financial Insturments

87

efficiency of its sectors and even in the number of Islamic financial institutions. The same

applies on

Takaful

sector where

Takaful

and

Retakaful

assets are significantly lower than many

other smaller jurisdictions. The following Table shows some key financial inclusion indicators

in Sudan for the year 2012.

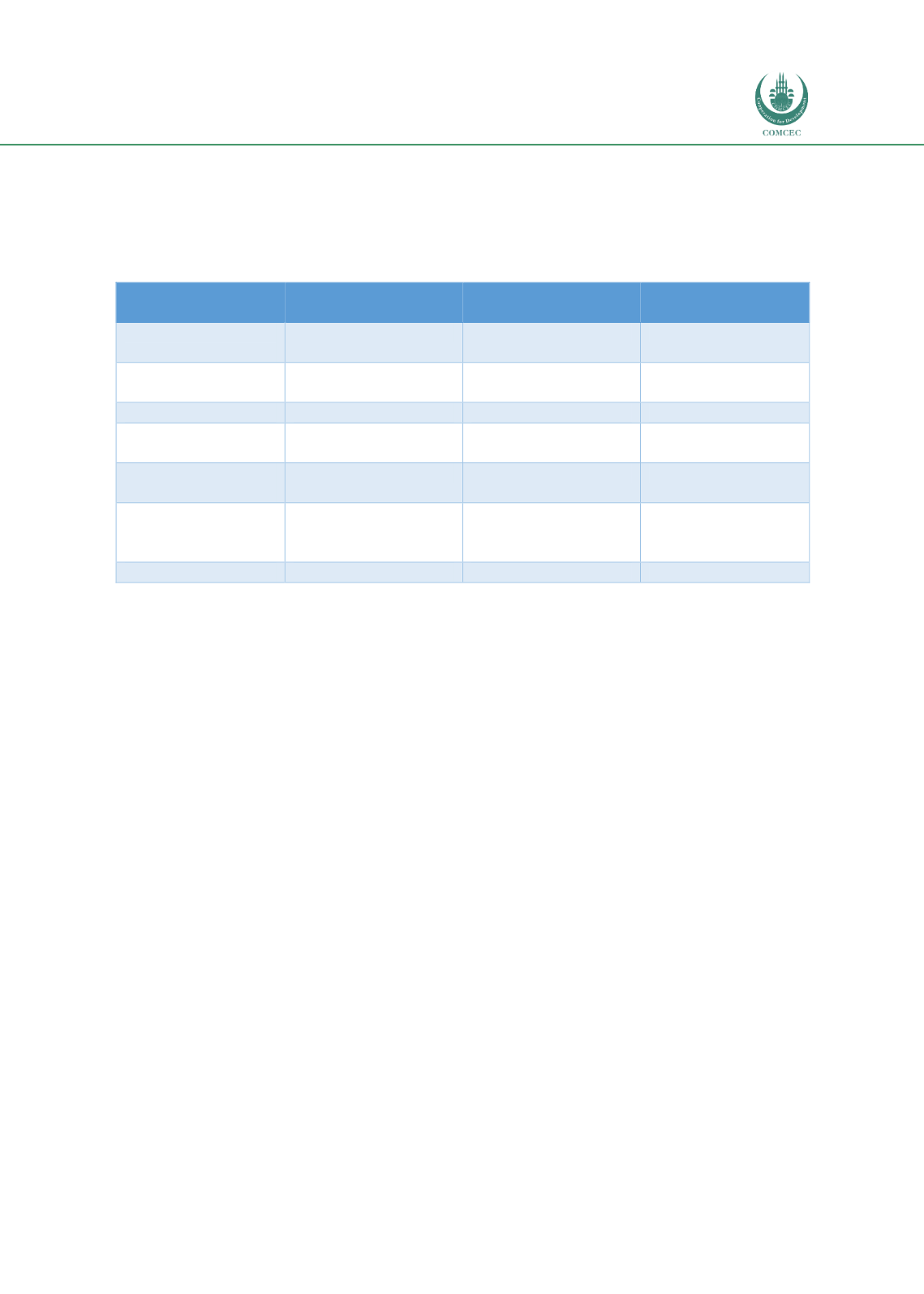

Table 37: Basic Financial Inclusion Indicators in Sudan (2012)

Low income

countries

Sub-Saharan

Sudan

Loan from a

financial institution

11%

5%

2%

Loan from a family

or friends

30%

40%

47%

Credit cards

2%

3%

1%

Saved at financial

institution

11%

14%

9%

Saved using a

saving club

8%

19%

7%

Account at formal

financial institution

(Male)

20%

24%

4%

Female

24%

21%

3%

Source: World Bank Findex database. The indicators represent percentage of population above 15

From above table, it is realized that the Sudanese depends more on other modes of finance

such as family, friends and clubs comparing to other Sub Saharan and low income countries.

Moreover, their savings at banks are less than others. This could be due to the significantly

lower percentage of bank accounts per person which is only 4% for male and 3% for female.

Hence, the weak financial inclusion in Sudan emphasise the importance of a comprehensive

financial development that include banking and non-banking institutions.

3.4.3 ISLAMIC BANKING IN SUDAN

Banking system in Sudan works under the supervision and regulations of Central Bank of

Sudan within the banking business organization act for the year 2004 which clearly states that

“banking business operating in Sudan should not contradicts with Islamic Shariah, and defines

finance as “investing funds according to Islamic contracts”.

The banking sector forms the backbone of Sudan’s financial system and is the primary source

of financing for the domestic economy. Sudan and Iran continue as the two jurisdictions that

operate fully

Shariah

-compliant banking systems; hence, a 100% Islamic banking market share

for each (IFSB, 2017). According to the Islamic finance development indicator for 2016: “Sudan

came at the 11th place out of 124, although it has followed a “fully” Islamic financial system for

quite a long time. This indicates many challenges that face the financial sector in Sudan, and

large area for improving it”.