93 / 231

93 / 231

Diversification of Islamic Financial Insturments

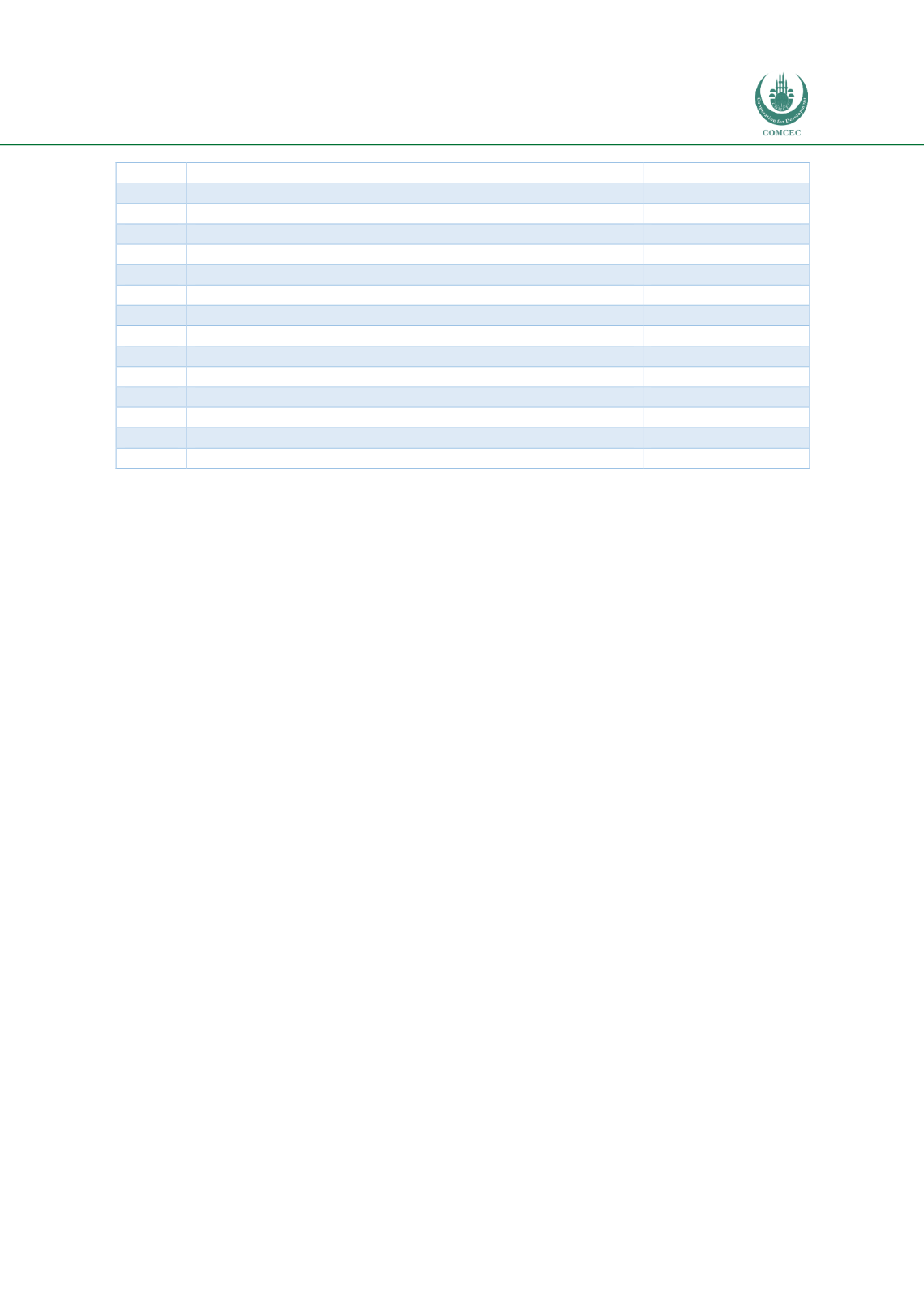

79

6

The United Insurance Company of Pakistan Limited

General

7

TPL Direct Insurance Limited

General

8

SPI Insurance Company Limited

General

9

Jubilee General Insurance Company Limited

General

10

EFU General Insurance Limited

General

11

Askari General Insurance Company Limited

General

12

Asia Insurance Company Limited

General

13

Alfalah Insurance Company Limited

General

14

Premier Insurance Limited

General

15

Adamjee Insurance Company Limited

General

16

UBL Insurers Limited

General

17

Atlas Insurance Limited

General

18

Reliance Insurance Limited

General

19

Sindh Insurance Limited

General

20

Allianz EFU Life & Health Insurance

General

Source: Created by Author

There is no Re-Takaful operators at present in Pakistan, and this presents a significant

challenge for the Takaful industry. Re-Takaful is essential for the insurance industry, both Life

and non-Life Takaful as it combines several different Takaful pools to create a ‘pool of pools’,

mitigating risks. The coverage amount exceeding the legal ‘retention limit’ has to be covered by

a Re-takaful arrangement. Family Takaful operators in Pakistan are able to avail the large

global capacity of the Re-Takaful industry, using international operators such as Takaful-Re,

Munich-Re, Hannover-Re and Swiss Re-Takaful. This is partially because Family Takaful

products have been in existence for a comparatively longer time period. However, the lack of

local Re-Takaful operators poses a challenge for General Takaful. In view of this, the Shariah

advisors of General Takaful companies in Pakistan have allowed a relaxation in the sharing of

risks, by allowing a ‘co-Takaful’ instrument (5-6 Takaful operators sharing risks).

Wakala-Mudarabah-Waqf Model

In Pakistan, the Shariah advisors and the SECP regulators advise a hybrid model for both

Family and General Takaful operators, based on Wakala, Mudarabah and Waqf. It is commonly

denoted as ‘Wakala-Waqf’ model and is the only model commonly used by Takaful operators.