122 / 176

122 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

105

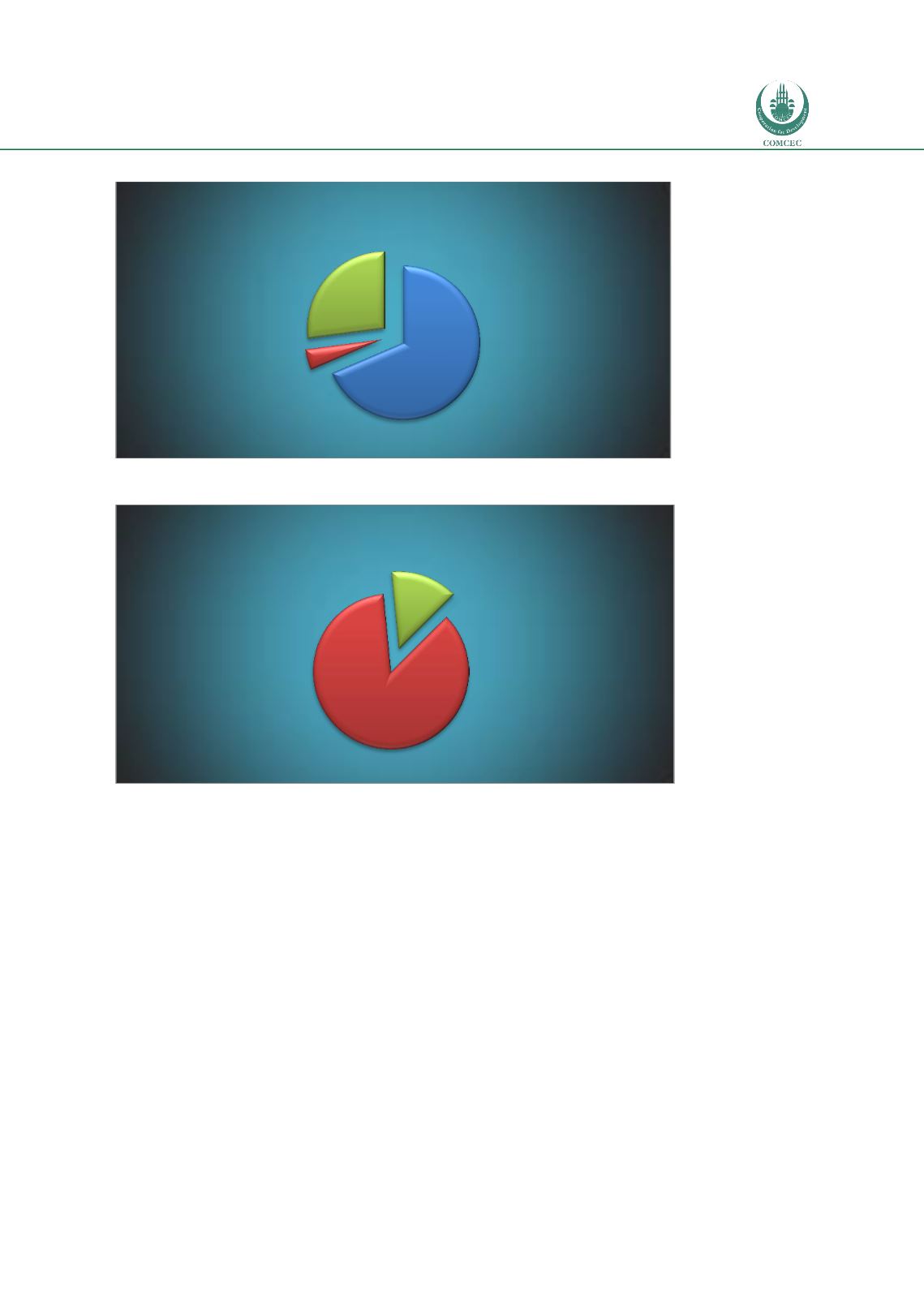

Figure 85: Profitability of the Banking Sector, Pakistan

Source: Bankscope

Figure 86: Loan Decomposition, Pakistan

Source: Bankscope

o

Nigeria

The banking sector in Nigeria exhibit a similar pattern to OIC countries in terms of asset

composition as most of assets are in the form of loans which is followed by securities. Risk-

weights are not available from Bankscope, however we infer a higher weight of credit risk

given the high fraction of loans. Securities are again in mostly “available for sale” form and

most of the liabilities are customer deposit, hence not deviating from the general pattern in

selected OIC countries.

Bank profit mostly originates from interest income. Loans are extended to the corporate sector

at a higher proportion compared to retail loans hence banks are mainly financing real sector

rather than consumer expenditures.

Net Interest

Income

69%

Net Gains on

Trad. and Der.

4%

Non-Interest

Operating

Income

27%

Profitability of the Banking Sector

Other

Consumer

Retail Loans

86%

Other Loans

14%

Loan Decompositon