117 / 176

117 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

100

In Kazakhstan majority of the credit is distributed as a corporate and commercial credit.

Compared to other OIC countries, Kazakhstan has the lowest consumer credits. Banking sector

has mostly distributed its credit to corporate and commercial sector.

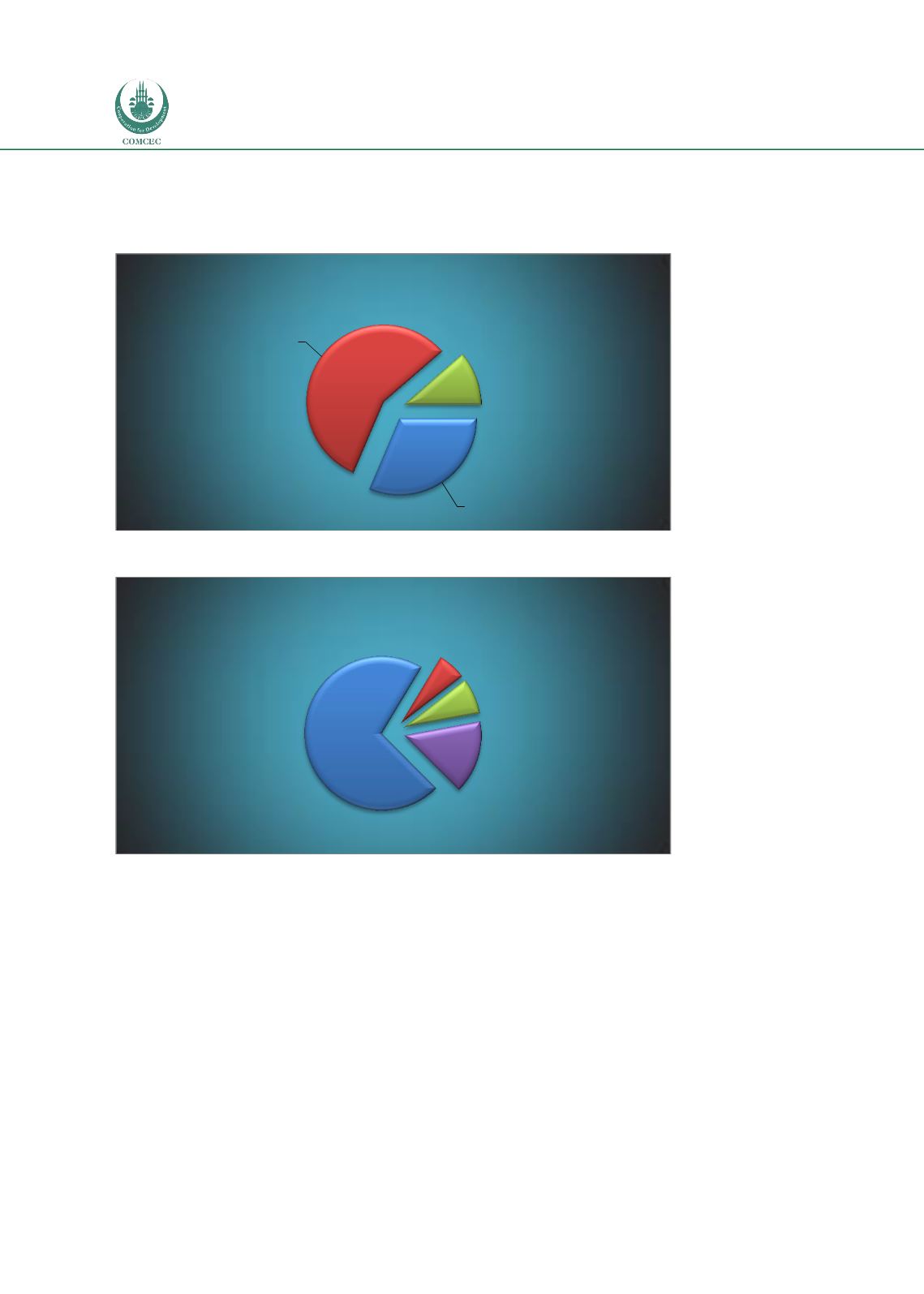

Figure 73: Decomposition, Kazakhstan

Source: Bankscope

Figure 74: Liability Decomposition, Kazakhstan

Source: Bankscope

o

Turkey

In terms of total asset decomposition, Turkey is slightly different than other selected OIC

member countries with a relatively lower fraction of loans in total assets. However, Bankscope

classifies most of the assets as “others” and it can be argued that this classification also

corresponds to credit related activities since 90% of risk weight is given to the credit risk

which is similar to the common pattern in selected OIC members.

Most of the securities are in the form of “available for sale” which indicates a high level of

liquidity of total securities. Majority of liabilities of the Turkish banking sector is in the form of

customer deposits and as indicated for other OIC countries, this provides a stable source of

funding. Furthermore, most of the profits of banks originate from interest-bearing activities

with 67% followed by operational profits which constitutes approximately 30% of total

profits.

Trading Sec. &

at FV

through

Income

32%

Available for

Sale Securities

57%

Held to

Maturity

Securities

11%

Securities Decomposition

Total

Customer

Deposits

71%

Deposits from

Banks

6%

Others

8%

Total Equity

15%

Liability Decomposition