124 / 176

124 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

107

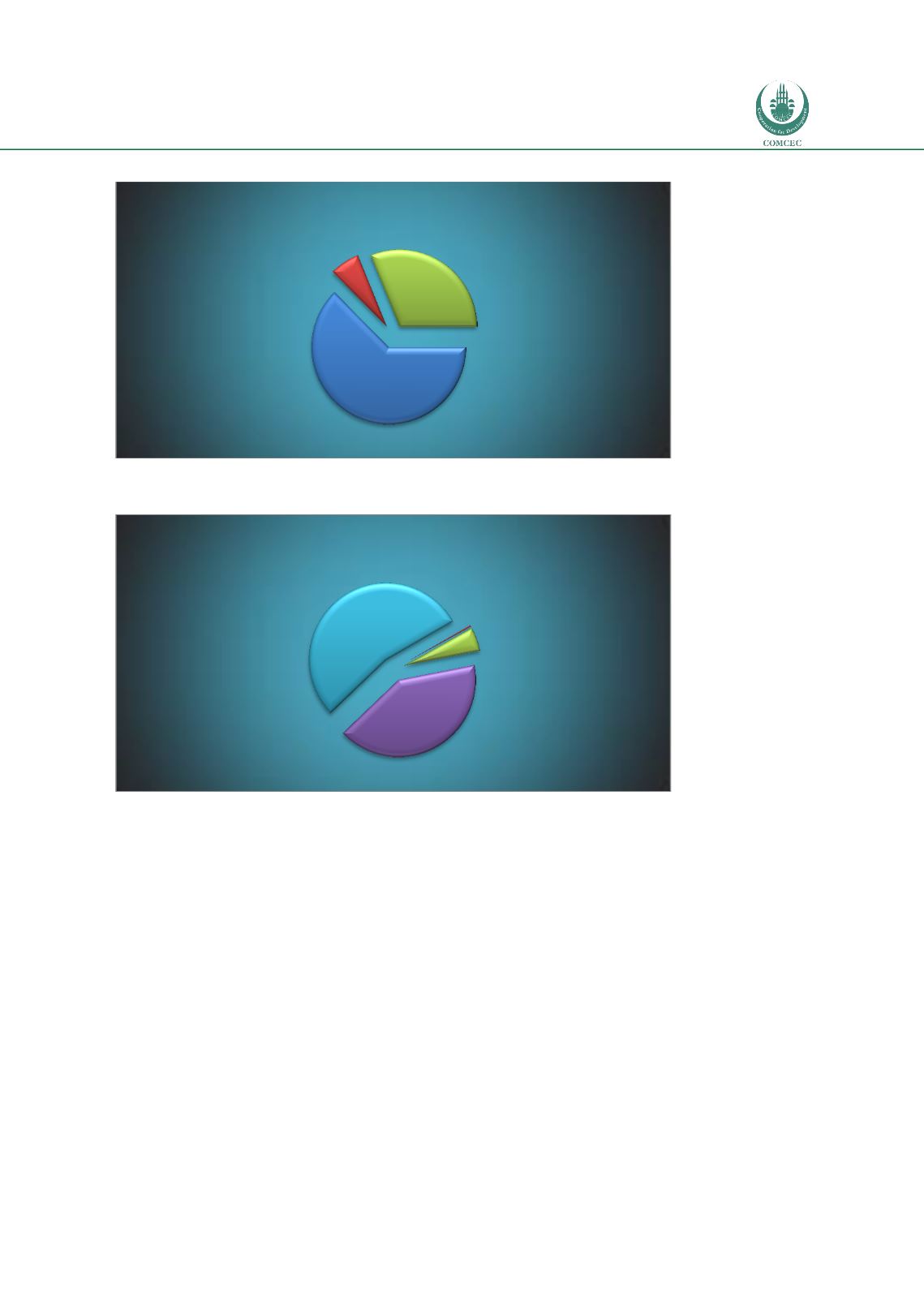

Figure 90: Profitability of the Banking Sector, Nigeria

Source: Bankscope

Figure 91: Loan Decomposition, Nigeria

Source: Bankscope

o

Algeria

Algeria, similar to Turkey, has a relatively lower fraction of loans in total assets with the

majority of assets held in other forms which are not directly identified in the Bankscope

database. Risk-weights are not provided in the database for Algeria, however we do not see a

significant deviation from other selected OIC member countries.

Securities are again predominantly in the form of “available for sale” which suggest a healthy

liquidity position. Loans are mostly extended, higher than OIC average, to the corporate sector,

which is the preferred distribution of loans. Liabilities are dominated by customer deposits

and profits mainly rely on interest income, therefore there is no significant deviation from the

general pattern observed in selected OIC member countries.

Net Interest

Income

63%

Net Gains on

Trad. and Der.

6%

Non-Interest

Operating

Income

31%

Profitability of the Banking Sector

Other Consumer

Retail Loans (%

of G. Loans)

5%

Corporate &

Commercial

Loans (% of G.

Loans)

41%

Other Loans

(% of G.

Loans)

54%

Loan Decomposition