60 / 111

60 / 111

47

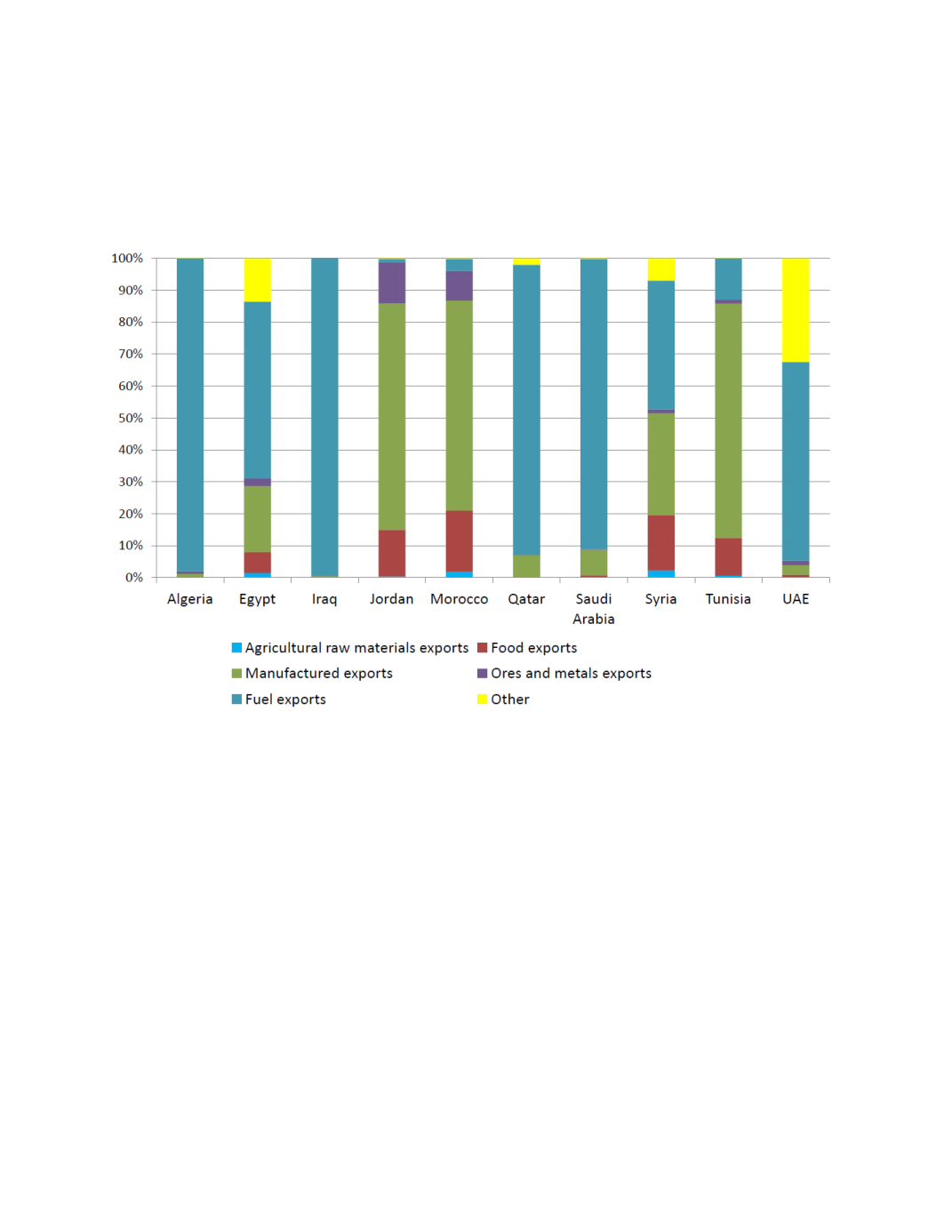

MENA countries have enjoyed a total trade (imports and exports) to GDP ratio of about 70%, which is

high by international standards. This indicator does, however, mask the particular factor endowments in

the region. A high level of exports of oil together with the import of a major part of all other needs

indicates limited capacity for local production and self-sufficiency, and therefore, high levels of economic

vulnerability.

Figure 3.3: Merchandise Exports of MENA Countries

Source: OECD, Word Bank, WDI

In this respect, the economies of the MENA countries do not all reflect the same upward or downward

trends in growth, competiveness, infrastructure developments, international trade and exports, and SME

activity. There are important differences between oil exporting and oil importing countries and between

those which have introduced major structural changes and those which have not. While overall growth in

the region is expected to be near the 5% mark, the economic growth of MENA’s oil exporting countries is

expected to be strong as it bounces back from 3.4% in 2010 to 5.4% in 2012. Oil importing countries, on

the other hand are expected to grow at about half that rate.

Recognition of the structural diversity of MENA countries leads us to identify common or similar

characteristics and overriding factors affecting particular groups of countries. We distinguish three intra-

MENA group of economies – the oil importing nations, the oil exporting economies and those which have

bucked the trend in the region.