59 / 111

59 / 111

46

Yemen

6

. The price of oil and the legacy of state dominated economic policies and structures are the two

factors that have shaped the MENA economies over the past twenty five years. In 2010, its total GDP

amounted to US$ 1.2 trn and its GNI (formerly GNP per capita), using the Atlas method of calculation, to

$3.866. More than 23% of the 336.5 million people of MENA live on less than $2 per day.

As the population in this region is growing more rapidly than other parts of the world, there are

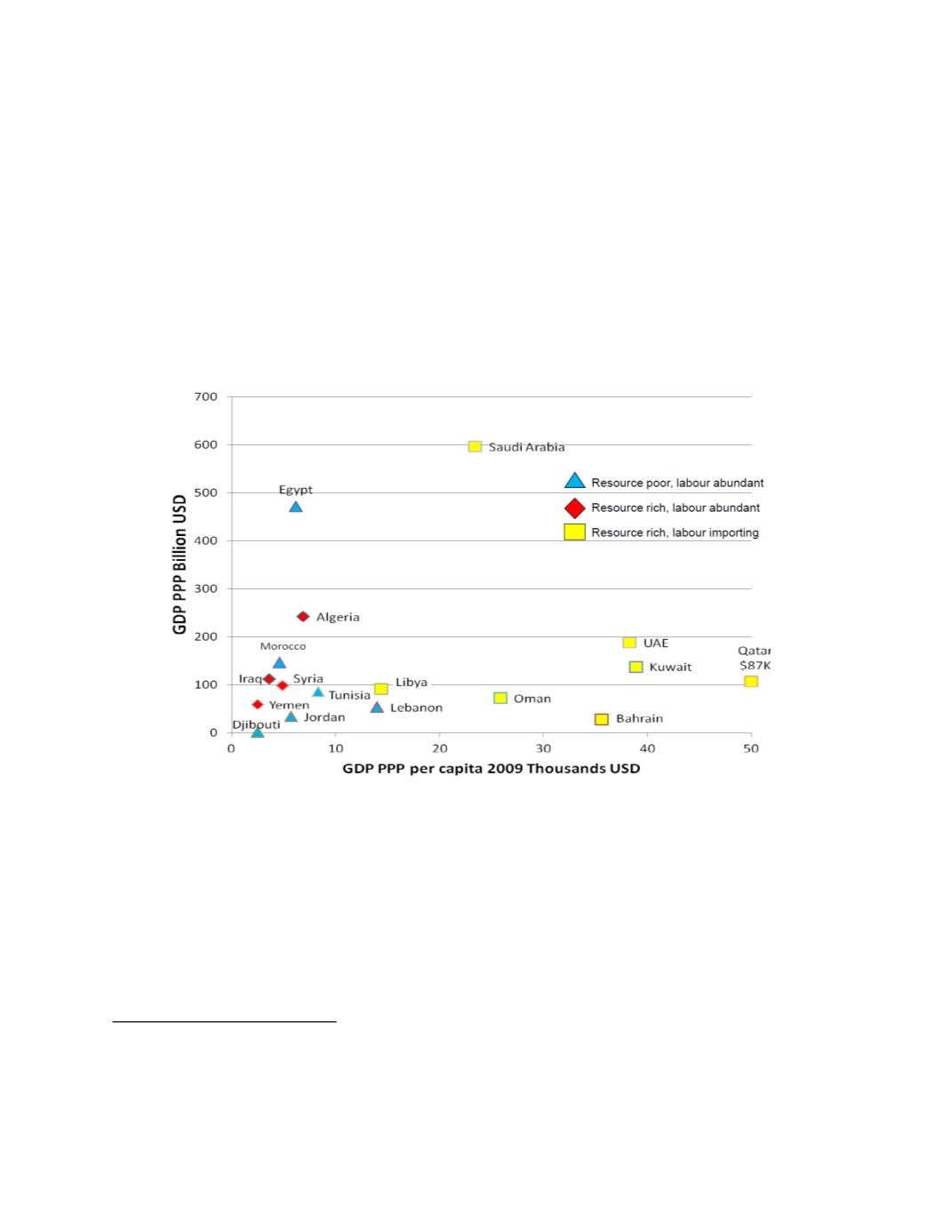

expectations of improvement in life expectancy, the quality of life, and infrastructure. Figure 3.2 shows

the diversity across MENA countries, in terms of absolute GDP value against a purchasing power parity

per capita basis. Saudi Arabia occupies a relatively lone position as the resource ‘rich, labour importing

country’ at the top in absolute GDP value while Qatar has a significant lead on a purchasing power per

capita basis. A cluster of labour abundant but either resource rich (Yemen) or resource poor countries take

up lowly positions by both measures.

Figure 3.2 Structural Diversity of MENA Region Countries

7

Source: IMF

In common with other regions, MENA countries’ ability to be competitive in the export market is

dependent on the strength, nature and quality of its domestic economies. Researchers argue that the short-

run costs of adjustment to trade liberalisation and successful integration to global markets and global

markets have generated large employment dividends. However, this association is also dependent on FDI

inflows. Trade alone adds a little to job creation. Low value added exports and loose or poor links to

global production networks together with a paucity of FDI may indeed reduce these countries’ capacity

for employment creation.

6

Yemen, together with Iraq, Kuwait, Saudi Arabia and the UAE, is one of the main providers of the world’s crude

oil supplies.

7

MENA-OECD Working Group on SME Policy, Entrepreneurship and Human Capital Development, Tunis 29

March, 2010