89 / 247

89 / 247

The Role of Sukuk in Islamic Capital Markets

70

4.

CASE STUDIES

4.1

INTRODUCTION: SELECTION CRITERIA AND METHODOLOGY

In determining the selection criteria and methodology, several factors have been analysed. The

development-stage matrix (shown in Table 4.1) has been established to categorise the

countries under review.

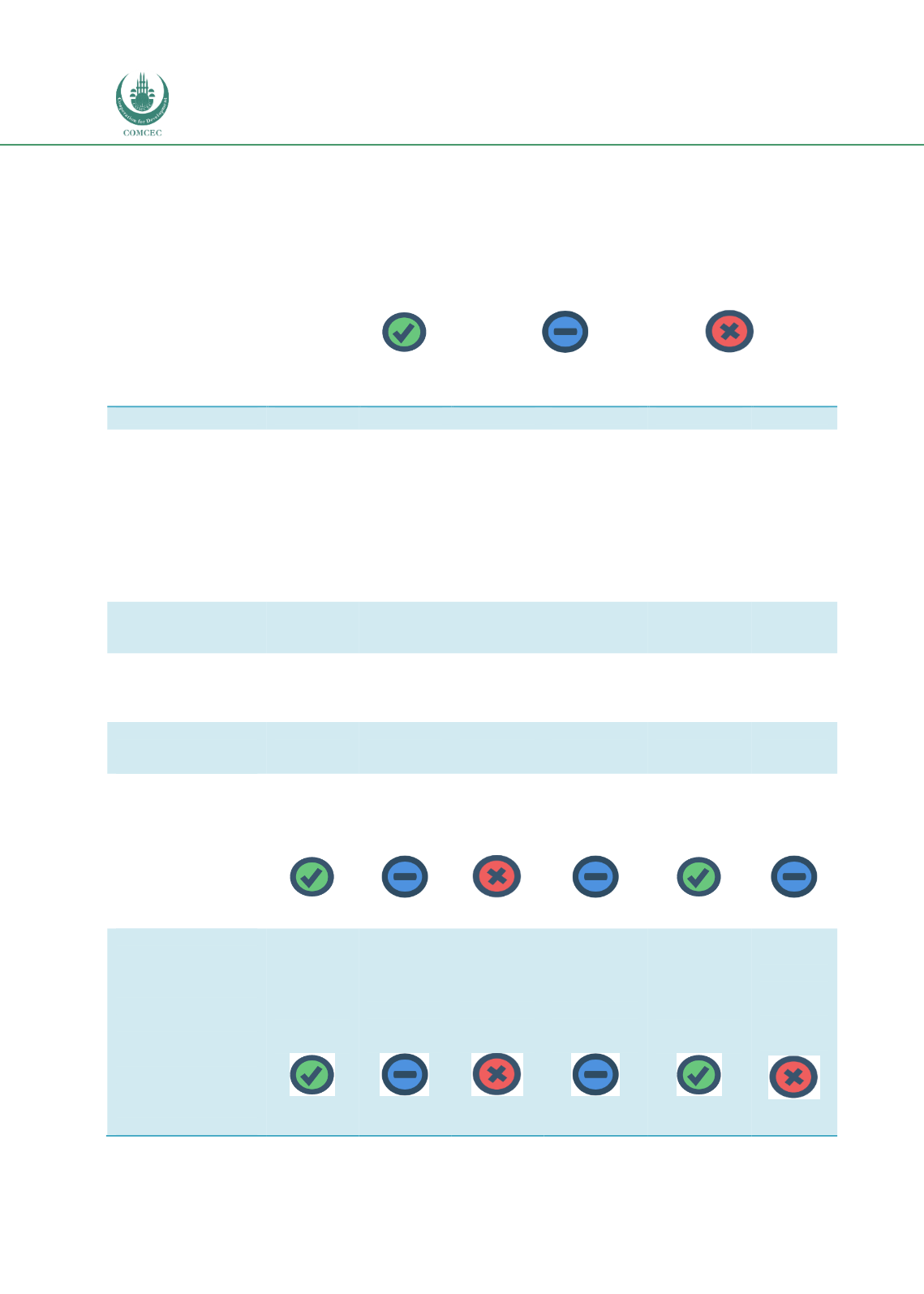

High

Moderate

Low

Table 4.1: Development-Stage Matrix for Sukuk

Matured

Developing

Infancy

Malaysia

UAE

Indonesia

Turkey

Hong Kong

Nigeria

Level of

macroeconomic

stability

(ratings of the

country based on

various factors such

as geopolitical

tension, volatility of

local currency, level

of inflation rate)

A- (S&P),

A3

(Moodys),

A- (Fitch),

A

2

(RAM)

AA (S&P),

Aa2

(Moodys),

AA (Fitch)

AA

2

(RAM)

BBB-

(S&P), Baa3

(Moodys),

BBB

(Fitch),

BBB

2

(RAM)

BB (S&P),

Ba1

(Moodys),

BB+ (Fitch)

BBB

3

(RAM)

AA+ (S&P),

Aa2

(Moodys),

AA+ (Fitch)

B (S&P),

B2

(Moodys),

B+ (Fitch)

Percentage of

Muslim population

to total population

61.3%

76%

87.2%

99.8%

1.4%

50%

Percentage of

Islamic banking

assets to total

banking assets

> 20%

> 20%

< 5%

< 5%

< 1%

< 1%

Market share of total

global sukuk

issuance

> 40%

10%-20%

10%-20%

< 10%

< 1%

< 1%

Legal framework:

-

Common law or

civil law

-

Amendments to

local law

-

Clarity of dispute

resolution,

bankruptcy act,

arbitration

Common

law

Civil law,

market

driven

Civil law,

market

driven

Civil law,

with clear

processes

Common

law

Common

law

Regulatory

framework:

-

Strong and single

regulation to

govern bond

market

-

Specific guidelines

on sukuk

-

Regulatory

protection for the

bond market

-

Ratings

Comprehen

sive

framework

and

guidelines

Vulnerable

due to

minimal

framework

Gaps

between

sovereign

and

corporates

Release of

Communique

to govern

sukuk

Global

financial

centre

Under-

developed