50 / 247

50 / 247

The Role of Sukuk in Islamic Capital Markets

32

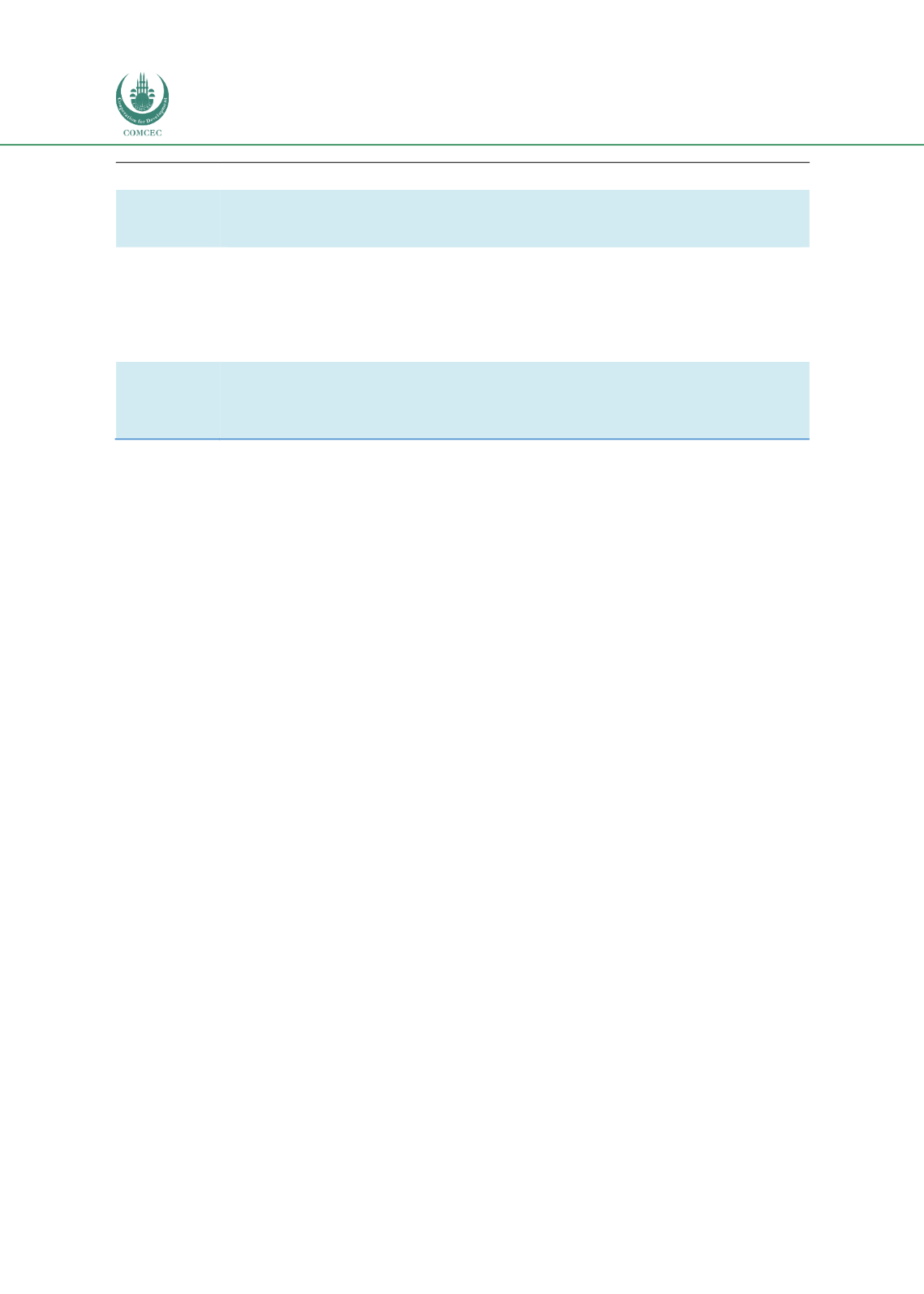

Country

Tax Changes

United

Kingdom

Alternate Finance Investment Bond (AFIB) introduced by Finance Act of 2007

deemed sukuk as 'securities' for tax purposes and eliminating VAT and stamp

duty on transfer of certificates

Turkey

In 2011, Turkish Law No.6111 was issued to provide tax exemption or

favourable tax treatment for sukuk, reducing the withholding tax on sukuk

and introduced tax neutrality on

ijarah

sukuk issuance

In 2016, the other sukuk structures namely

wakalah

,

murabahah

,

mudarabah

and

istisna’

were granted tax neutrality with a law amending the Stamp Tax

Law, VAT Law and Law on Charges.

Indonesia

Withholding tax on interest payments for government securities, including

sukuk, was removed

In 2016, the Financial Services Authority (Otoritas Jasa Keuangan (OJK))

provides lower registration fees for corporate sukuk issuances

Source: Compiled from various resources by ISRA and RAM.

2.6.3

SUPERVISORY

The role of an effective supervisory framework is to ensure discipline, control and minimum

standards of prudential conduct, among others. The regulatory and supervisory framework

encompasses the various frameworks put in place by the regulatory authorities in their

respective jurisdictions to deal with specific areas: licensing of capital market intermediaries;

requirements for acceptable market conduct; Shariah compliance requirements; registration of

Shariah advisers; disclosure, corporate governance and transparency requirements; and

establishment of robust infrastructure such as stock and commodity exchanges. These

frameworks are usually established through the collaboration of different bodies and agencies,

such as government authorities, regulators, exchange authorities, and industry associations.

They can take the form of specific guidelines issued to fulfill certain purposes. For instance, the

requirements set out under the LOLA Framework (June 2015) by the SC include the following:

Lodgement requirements.

Requirements for the invitation, offering, subscription, purchase and issuance of

sukuk.

Ringgit and FCY sukuk.

SRI sukuk.

Credit rating requirements and exemptions.

Details of the approved Shariah primary and supplementary principles and concepts.

Transferability and tradability, programme issuances, utilization of proceeds and

Shariah advisers.