62 / 231

62 / 231

Diversification of Islamic Financial Instruments

48

According to the 2016 financial statements

31

of Cornerstone Insurance Plc., the performance of

the

Takaful

products vis-à-vis the conventional insurance products is shown in the table

(Takaful Products Performance) below. It should be noted that the other two conventional

insurance companies did not report the performance of their

Takaful

products perhaps due to

its insignificant.

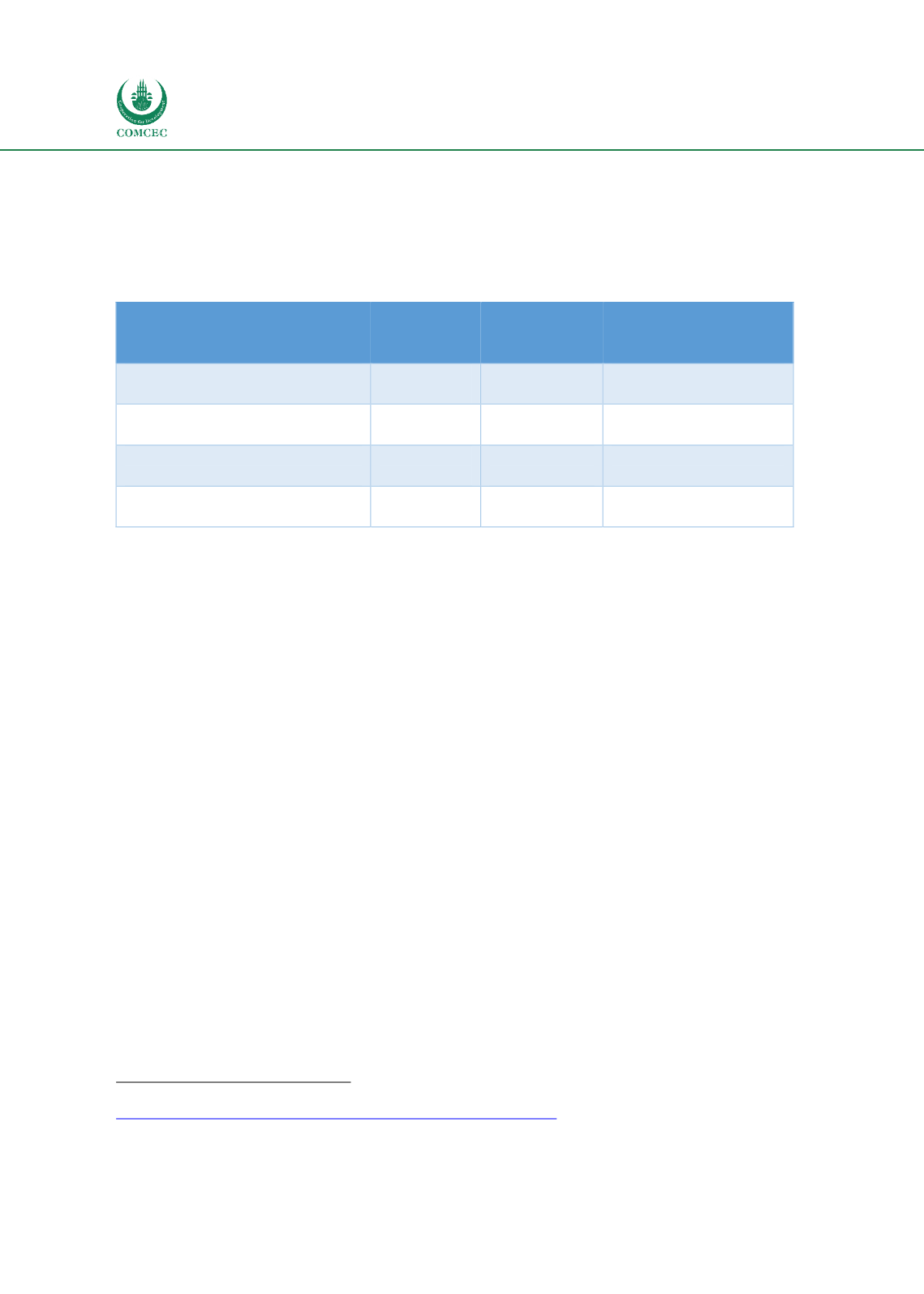

Table 20: Takaful Products Performance as at end December 2016

Takaful

Insurance

Products

Conventional

Insurance

Products

%

Takaful

/Conventional

Gross Premium ($' 000 )

672.73

18,242.83

3.69

Gross Claim ($' 000 )

247.58

8,025.20

3.09

Underwriting Expenses ($'

000)

139.32

3,634.15

3.83

Underwriting Results ($' 000)

298.30

2,081.03

14.33

Sources: Computed from Cornerstone Insurance Financial Statements for 2016

From the table above, the gross premium, gross claims and underwriting expenses generated

by the

Takaful

products is less than 4% of those generated by the conventional insurance

products. Compared to the entire insurance industry, the performance of the

Takaful

in terms

of premium, claims and underwriting expenses will be much more less than 4% signifying

insignificance of the

Takaful

business in Nigeria.

Challenges Facing the Islamic Financial Sector

There are a number of issues that are militating against the development and growth of Islamic

finance sector Nigeria. These include:

Lack of separate legal framework:

The operations of Islamic financial institutions

are subjected to the interpretation of the laws guiding the operations of the

conventional financial institutions. There are no explicit statements of laws for the

Islamic financial institutions; they depend on the interpretation of some provisions of

the laws for conventional financial institutions.

Lack of viable liquidity management instruments for Islamic financial

institutions:

To date the Central of Bank of Nigeria has been able to come up with

only three (3) liquidity management instruments and only one of the three

instruments is viable as it enables an Islamic bank to manage it liquidity and obtain

some return. This instrument involves securitization of the Central Bank’s holding of

multilateral financial institutions’

Sukuk

for the Islamic banks to invest. Unfortunately,

this instrument is still not available as the Central Bank is still having some challenges

31

Cornerstone Insurance Annual Report and Financial Statements 2016 available at:

www.nse.com.ng/.../13741_CORNERSTONE_-_2015_AUDITED_ACCTS_FINANCI ...