59 / 231

59 / 231

Diversification of Islamic Financial Insturments

45

The shares and sizes of these products in the entire Islamic banking segment are displayed in

table given below:

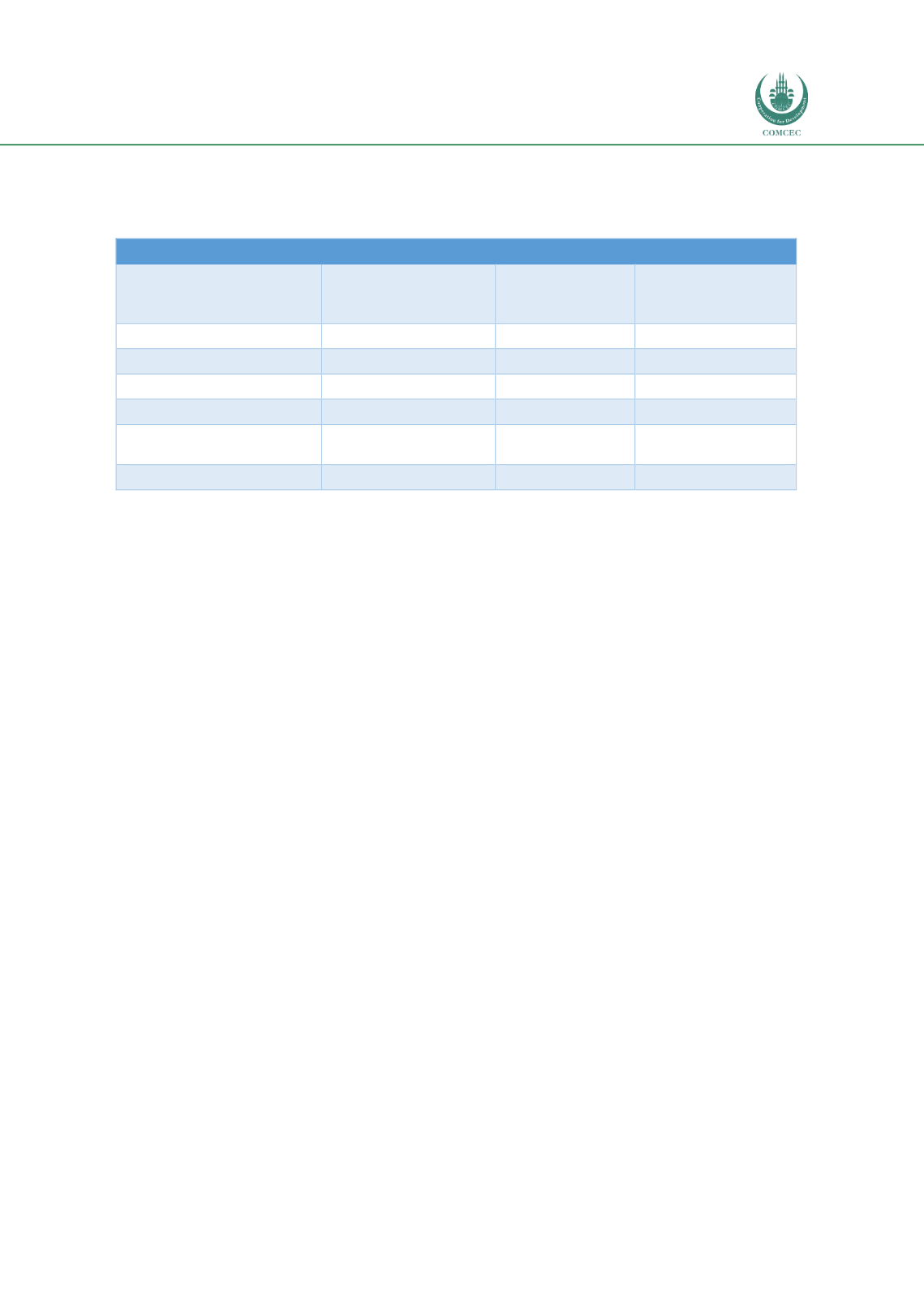

Table 18: Sizes and Shares of Financing Products (Corporate and Retail)

Financing by Islamic Banks as at December 31, 2015

FINANCING MODE

Local Currency

(Million Naira)

Dollar

Equivalent

(Million $)

% OF TOTAL

FINANCING

Murabahah

Receivables

12,290.25

40.30

47.45

Musharakah

Financing

653.18

2.13

2.52

Qard Hasan

Receivables

147.24

0.48

0.57

Istisna

Investments

781.90

2.57

3.02

Ijarah

Assets

Investments

12,028.84

39.50

46.44

TOTAL FINANCING

25,901.42

84.98

100

Source: Computed from Annual and Management Accounts

From above table it is obvious that the retail financing products dominate the market with

Murabahah

and

Ijarah

accounting for 47.45% and 46.44%, respectively, while the corporate

financing which mainly consists of

Musharakah

and

Istisna

accounts for only 2.52% and 3.02,

respectively. The following are some of the issues and benefits that account for this financing

trend in Nigeria:

(a)

The use of

Hamish Jiddiyya

(Down Payment) in

Murabahah

to secure the promise to

purchase

(b) Mark up is defined considering historic market trend and tenured as much as possible

for shorter period thus encouraging fixed income instrument like Murabahah

(c)

Accurate forecast of income in view of the fixed income nature of the preferred

financing products

(d)

In an

Ijarah

contract the customer maintains the asset in protection of the interest of

the Lessor at his expense except in cases of any accident due to natural

calamity/disaster (Acts of Allah) which has to be ascertained by the banks.

(e)

Use of

Takafu

l cover as a mitigant to natural disasters.

(f)

Longer gestation period of project normally financed through either

Istisna

or

Musharakah

discourages Islamic banks from using such products.

(g)

The Islamic banks lack the expertise to appraise and monitor projects and this

discourages them from financing such projects through either

Mudarabah

or

Musharakah

Thus in Nigeria, the Islamic banking industry is dominated by retail financing (

Murabahah,

Ijara

h and

Qard Hasan

) accounting for about 94.46% while the corporate financing

(

Musharakah

and

Istisna

) accounted for only 5.54%.