57 / 231

57 / 231

Diversification of Islamic Financial Insturments

43

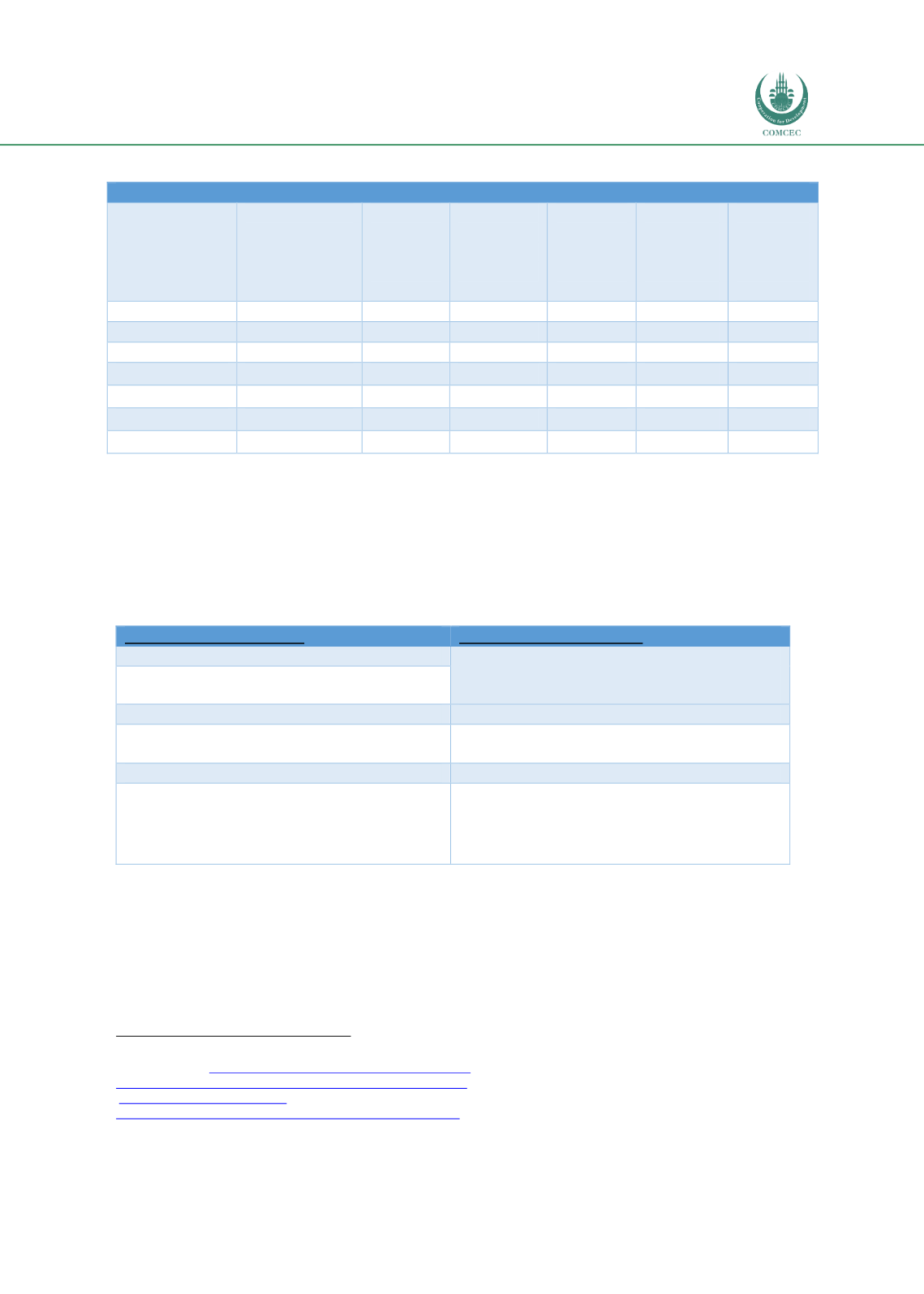

Table 13: Financial Performance Indicators as at December 2015 and 2016

Banking Sector Data in $ (1$ = 306 NAIRA)

2016:

Conventional

Banks

(Million $)

Non-

interest

Banks

(Million

$)

Total for

Industry

(USD

million)

% Non-

interest

Banks/

Industry

Conven-

tional

Banks

growth

rate (%)

Non

Interest

Banks

growth

rate (%)

Total Assets

98,473.88

229.66

98,703.54

0.023

11.76

29.4

Total Deposits

60,575.76

164.33

60,740

0.27

6.15

26.58

Total Credits

53,131.13

115.55

53,247

0.22

21.98

39.21

2015:

Total Assets

88,111.92

177.48

88,289

0.2

Total Deposits

57,066.86

129.82

57,197

0.23

Total Credits

43,558.08

83

43,641

0.19

Source: CBN’s FinA (Financial Analysis)

The Islamic Banking Products

24

Islamic banks structured products to satisfy the demand for service from their customers.

These products are classified into two categories; namely: Funding (Deposit mobilization) and

Financing products. A snapshot of the deposit mobilization products is depicted in table given

below:

Table 14: Deposit (liabilities) Mobilization Products

Customer requirements

Islamic Banking Product

Individual & Corporate Savings Accounts

Mudarabah, Qard Hasan

Tier one & two Savings Accounts

Special Investment Accounts

Mudarabah Term Deposit

Investment account, Zakat and Sabil

Management accounts

Wakala Investments

Liquidity Management Purposes

Wadiah based Accounts

Current and Domiciliary Accounts for

both

individual

and

corporate

customers as well as Salary Account for

individuals.

Qard Hasan

Source: Compiled from the websites of Jaiz Bank, Sterling and Stanbic IBTC Non-interest banking windows and

Tijara Islamic Microfinance Bank.

24

Details of these products can be obtained from the websites of Jaiz bank, the two Islamic banking windows and Tijara

Microfinance at

: http://jaizbankplc.com/?s=jaiz+annual+report , http://www.stanbicibtcbank.com/Nigeria/noninterestbanking , http://www.saf.ng/about.php , http://aifreport.afrief.com/tijara-microfinance-bank-limited/