49 / 231

49 / 231

Diversification of Islamic Financial Insturments

35

The concept of Takaful in its essence is very similar to that of mutual insurance, with the

exception that it complies with Islamic law. Essentially, an operational Takaful model has to be

free of not just Riba, but the elements of Gharar (excessive or avoidable uncertainty) and

Maysir (gambling). The basis of Takaful is mutual solidarity with risk sharing – specific funds

are established with a selected group of Takaful participants agreeing to jointly support each

other from any losses arising from specified risks. The schemes or funds are then managed on

their behalf by a Takaful operator, who usually earns income on the basis of Mudarabah (profit

and loss sharing) or Wakala (agency). Hence in one word, the two key characteristics of any

Takaful operation are Shariah compliance and Risk sharing.

11

A diversified Islamic financial

industry with a well-developed Takaful sector also contributes to increasing the overall

stability of the financial system.

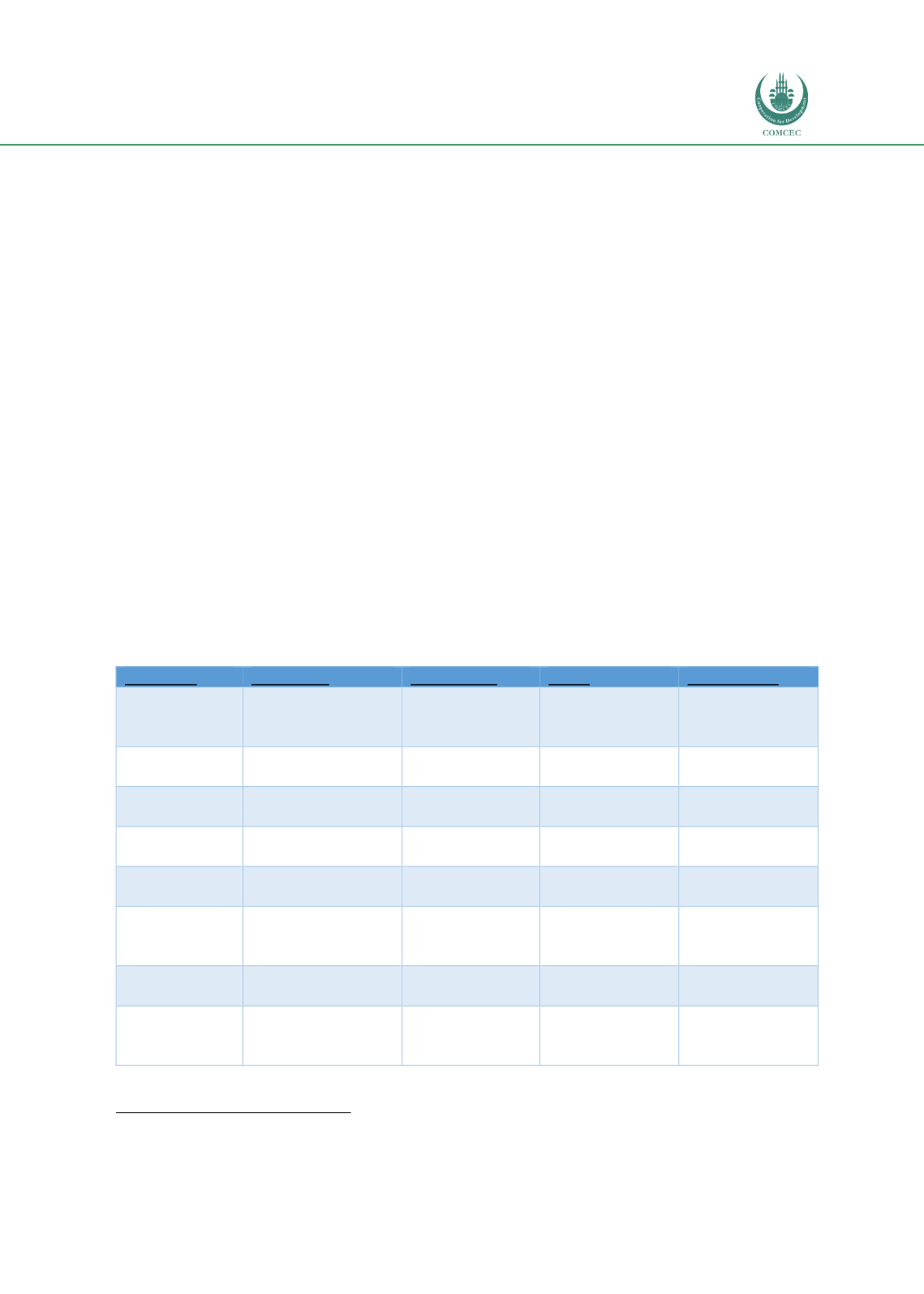

The ‘optimal structure’ of a Takaful model is still a disputed matter. In the international

landscape, multiple models are used, mostly based on Tabarru (donation), Wakala, Mudarabah

and Waqf. As the table below demonstrates, though sometimes the Takaful operation is on a

pure Mudarabah or a pure Wakala basis, in many jurisdictions today including Sudan, Bahrain,

Malaysia and Pakistan, hybrid models are used, such as Wakala – Waqf, Mudarabah – Wakala

and Wakala-Mudarabah-Waqf. The choice of the operational model depends on factors such as

Regulations in a given jurisdiction

Whether its Family Takaful or General Takaful

Requirement from Shariah advisor

Compliant securities.

Table 12. Differences in Takaful Models Used

Properties

Mudarabah

Pure Wakala

Mixed

Wakala-Waqf

Creation of

fund:

The participants

(Takaful clients)’

contributions

participants’

contributions

participants’

contributions

There is an initial

donation to create

Waqf

Fees:

None

Up-front fees as

agreed

Up-front as agreed

Up-front as agreed

Underwriting

losses:

Qard-a-hasan from

Takaful operator

Qard-a-hasan from

Takaful operator

Qard-a-hasan from

Takaful operator

Waqf to solicit

funds

Investment

profits:

None

None

As per the agreed

profit-sharing ratio

As per agreed

profit-sharing ratio

Investment

losses:

Borne by participants

By participants

Borne by Takaful

operator

by Takaful

operator

Operational

expenses:

Borne by Takaful

operator (with some

exceptions)

by Takaful

operator

by Takaful

operator

by Takaful

operator

Liquidation

Proceeds accrue to

participants only

Proceeds accrue to

participants only

Proceeds accrue to

participants only

Proceeds accrue to

participants only

Present in

Jurisdictions:

Malaysia, Saudi Arabia

and some GCC

members

United Kingdom

Bahrain, Malaysia

and Sudan

Pakistan & South

Africa

Source: IRTI Global Report on Islamic Finance, 2016

11 IRTI The Global Report on Islamic Finance 2016, Chapter 5 Takaful