41 / 231

41 / 231

Diversification of Islamic Financial Insturments

27

institutions are bound by the Shariah law to invest in them. Recently, high-profile issuances by

non-Muslim sovereigns have catapulted Sukuk into the big leagues of finance, earning global

visibility despite their very modest size in absolute terms.

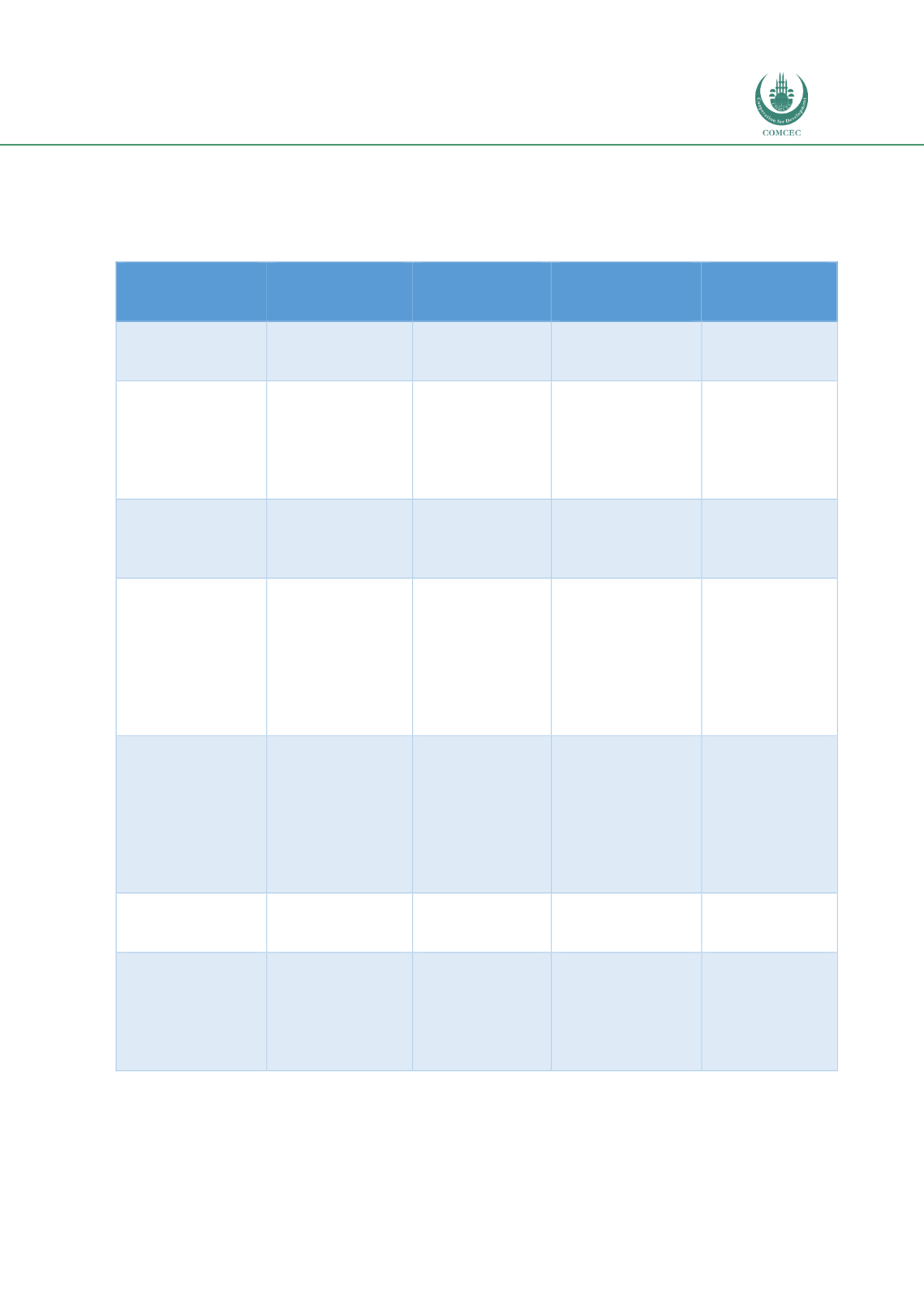

Table 11. Underlying Contracts in Sukuk Contracts

Underlying

contract

Originator

(Mudarib)

Investor

(Sukuk holder)

Interim cash-

flows(to Sukuk

holders)

Cash-flow at

maturity

Ijarah (lease)

Lessee of asset.

Pays lease

payments

Lessor

Periodic Lease

Payments

At maturity from

sale of asset

Wakalah

(Principal-agent

relationship)

Agent

undertaking

investment in

underlying asset.

Principal Owner

of invested asset

Cash Flows

generated by

investment

Dependent on

type of invested

asset and/or

economic life of

project. No fixed

return.

Bay Bithaman

Ajil (sale based

on deferred

payments)

Purchaser of

underlying asset

Owner/seller of

underlying asset

Payment of

purchase price in

instalments

May and may

not have a final

balloon payment

Mudarabah

Mudarib

(entrepreneur in

need of financing)

Rab-ul-Mal

(provide capital)

Periodic cash

flows from asset as

determined by

PSR

Unlikely. Final

payment could

simply be the

last periodic

payment given

tenor of

Mudarabah

contract.

Salam (Contract

for goods to be

delivered later–

forward)

Seller of

commodity/goods

which will be

delivered later

Purchaser of

commodity/good

s which will be

delivered later

Proceeds from sale

of goods received

– if there will be

delivering in the

interim

Usually the

largest cash

flows occur at

maturity when

delivery occurs.

Cash flow is

from sale

proceeds

Istisna

Purchaser of asset

under

construction

Financier for

asset under

construction

Payments from

Mudarib if any

Profit from sale

of completed

asset

Murabahah

Purchaser of asset Financier of

asset

Periodic payments

received from

Mudarib

representing price

of asset plus mark

up

Unlikely. Final

payment could

simply be the

last periodic

payment of

contract

Source: Created by Author