29 / 176

29 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

12

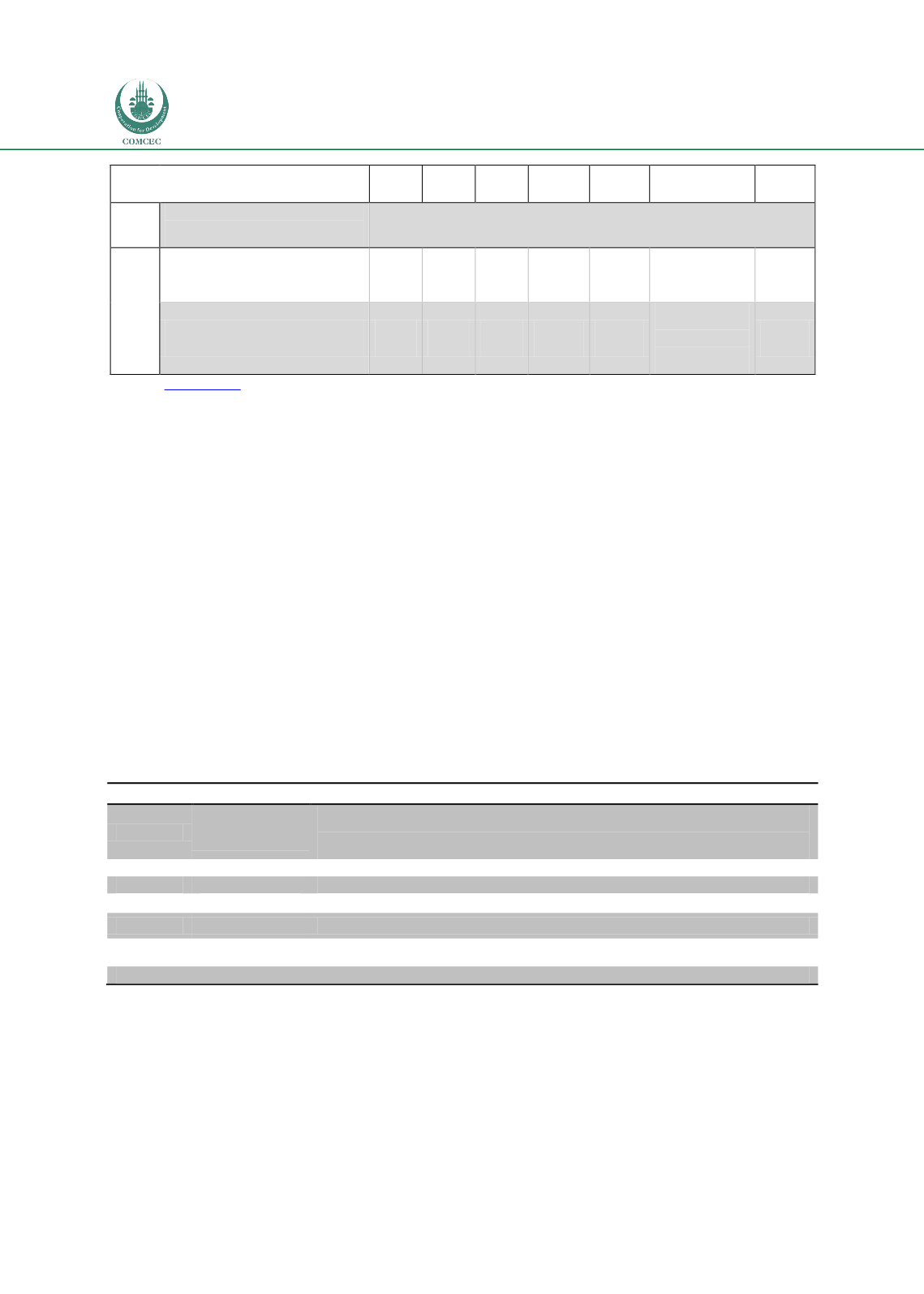

Phases

2013 2014 2015

2016

2017

2018

2019

longer qualify as non-core Tier

1 capital or Tier 2 capital

Liquidity

Liquidity coverage ratio -

minimum requirement

60%

70%

80%

90%

100%

Net stable funding ratio

Introduce

Minimum

Standard

Source

: www.bis.org* Including amounts exceeding the limit for deferred tax assets (DTAs), mortgage servicing rights (MSRs) and

financials.

- -

Transition periods

As can be seen from above, the new financial regulation framework will be much more

different and complex compared to previous regulation.

Systemic Risk Charges:

An additional requirement will be put on banks through their interconnectivity and asset size.

Depending on the size and contagious risks, banks might need to put aside additional capital.

In order to avoid the Lehman Brothers, AIG type big institutions to go bankrupt, BASEL III

requires very big institutions to hold surcharges. The amounts of these additional charges are

summarized below. Systemically important banks are required to hold up to 3.5% additional

capital. Financial Stability Board has determined 29 banks to be qualified as GSIB's. Even

though only 29 banks are considered as GSIB's, domestically big banks will also be required to

hold a stronger capital base. The alternative definition of GSIB is Domestic Systemically

Important Banks (D-SIBs) which is a term used for banks active in less developed countries.

Charging an extra capital for D-SIB's is under discussions in various countries.

Table 3: Systemic Risk Charge under BASEL III

Bucketing Approach

Bucket

Score range*

Minimum additional loss absorbency (common equity as a percentage of

risk-weighted assets)

5 (empty)

D -

3.50%

4

C - D

2.50%

3

B - C

2.00%

2

A - B

1.50%

1

Cut-off Point - A 1.00%

*Scores equal to one of the boundaries are assigned to the higher bucket

Source: BIS

(www.bis.org)

Summary of reforms

Increased overall capital requirement

: Between 2013 and 2019, the common equity

component of capital (core Tier 1) will increase from 2% of a bank’s risk-weighted

assets before certain regulatory deductions to 4.5% after such deductions.