28 / 176

28 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

11

The leverage ratio aims to:

Restrict the build-up of excess leverage in the banking sector to avoid destabilizing the

financial system and the economy;

To simplify the risk-based requirements by switching to a simple, non-risk-based

“backstop” measure

This new ratio ensures both the on- and off-balance sheet assets to be included in the

capital assessment.

Leverage ratio = Capital measure/Exposure measure, where the capital measure for the

leverage ratio is the Tier 1 capital of the risk-based capital framework

A bank’s total exposure measure is the sum of the following exposures: (a) on-balance

sheet exposures; (b) derivative exposures; (c) securities financing transaction (SFT)

exposures; and (d) off-balance sheet (OBS) items.

Consequently, BASEL III, imposes a constraint of 3% on the leverage of banks, i.e. the ratio of

Tier 1 capital to the total exposure of banks to supplement the risk-based capital framework of

BASEL II. The new leverage ratio will be much easier to calculate and will have a simpler logic

than that of right weight calculations.

Timeline: According to BASEL Committee, leverage ratio will be disclosed by 2015.

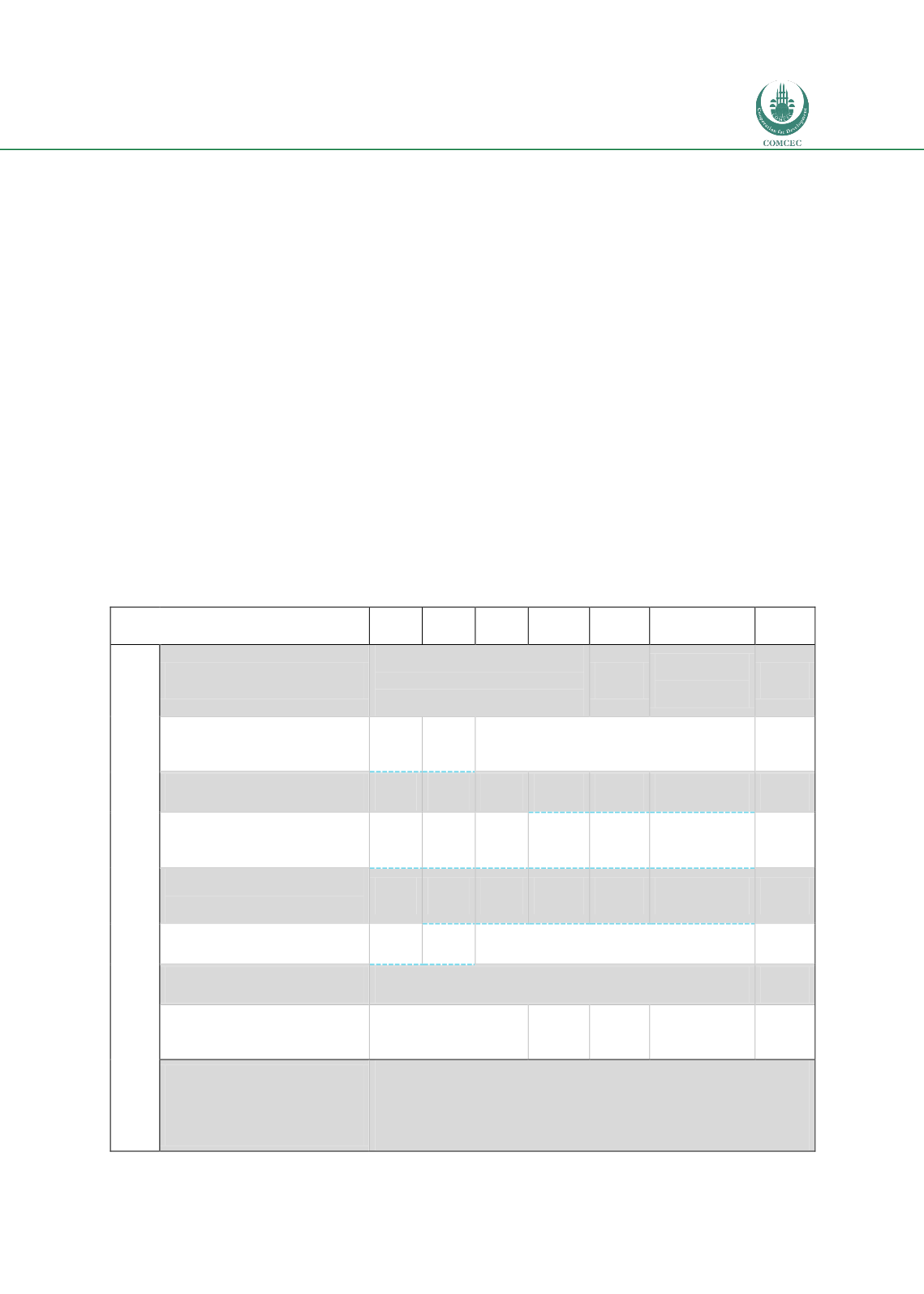

Below is the summary of the new BASEL III requirements and their time table.

Table 2: Time-table for new BASEL III Requirements

Phases

2013 2014 2015

2016

2017

2018

2019

Capital

Leverage Ratio

Parallel run 1 Jan 2013 - 1 Jan

2017

Disclosure starts 1 Jan 2015

Migration to

Pillar 1

Minimum Common Equity

Capital Ratio

3.50% 4.00%

4.50%

4.50%

Capital Conservation Buffer

0.625% 1.250%

1.875%

2.500%

Minimum common equity plus

capital conservation buffer

3.50% 4.00% 4.50% 5.125% 5.75%

6.375%

7.00%

Phase-in of deductions from

CET1*

20%

40%

60%

80%

100%

100%

Minimum Tier 1 Capital

4.50% 5.50%

6.00%

6.00%

Minimum Total Capital

8.00%

8.00%

Minimum Total Capital plus

conservation buffer

8.00%

8.625% 9.25%

9.875%

10.50%

Capital instruments that no

Phased out over 10 year horizon beginning 2013