27 / 176

27 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

10

Timeline: Consequently, all banks are required to have additional capital tackling for pro-

cyclicality. A capital buffer will be added on capital in 2016. By the year 2019, an additional

capital adequacy ratio of 2.5% will be required as a capital buffer

12

.

Liquidity Provisioning

Basel III imposes two internationally consistent regulatory standards for liquidity risk

supervision. These are Liquidity Coverage Ratio and Net Stable Funding Ratio.

Liquidity Coverage Ratio

Basel Committee has developed the Liquidity Coverage Ratio (LCR) to promote the short-term

resilience of the liquidity risk profile of banks by ensuring that they have sufficient High

Quality Liquid Assets (HQLA) to survive a significant stress scenario lasting 30 calendar days.

Liquidity coverage ratio (LCR) measures the amount of high-quality liquid assets that can be

used to match short-term (30-day period) net cash outflows and requires the ratio of stock of

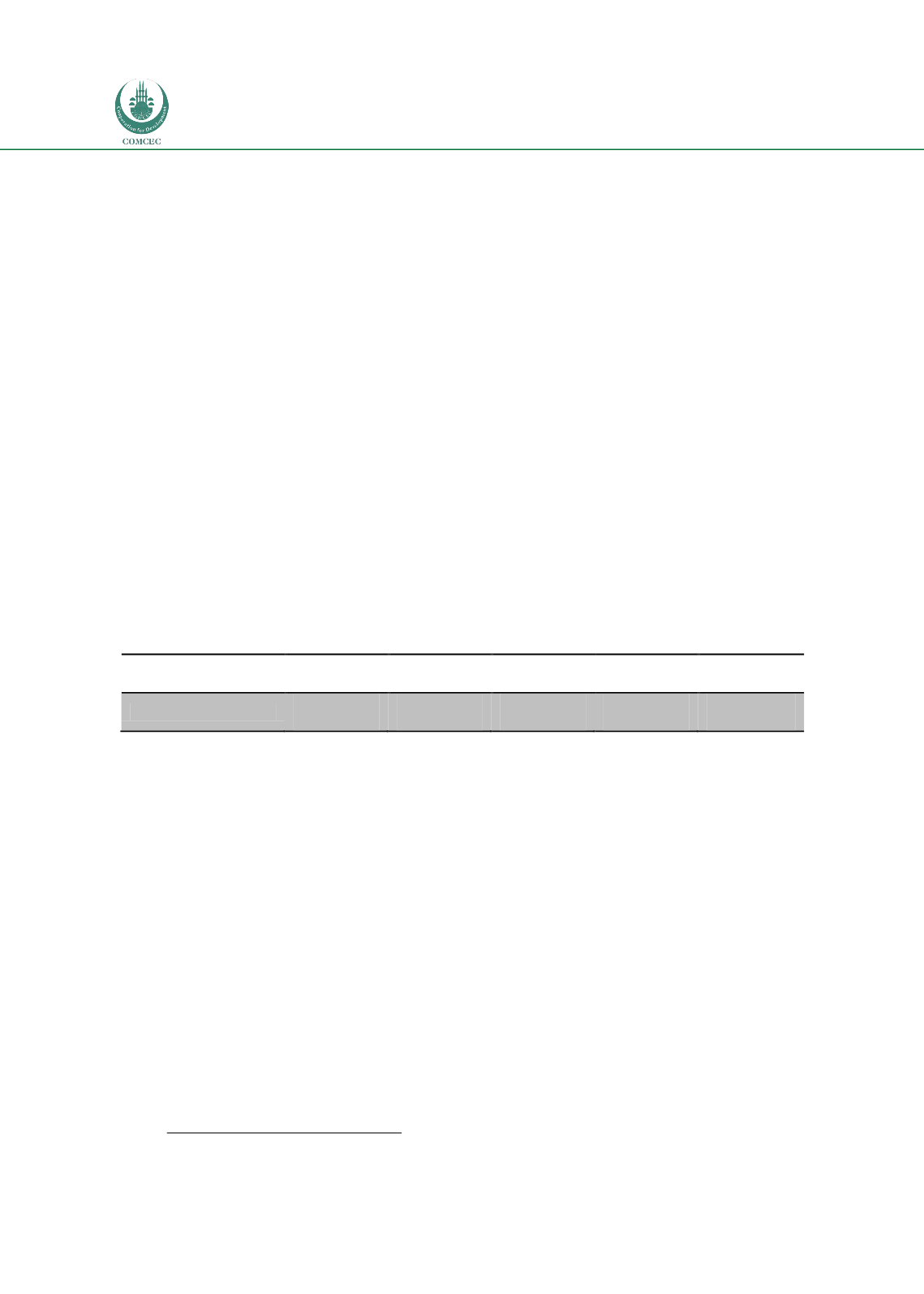

high-quality assets to the net cash outflows to be greater than a minimum. The time table for

LCR is presented below.

Basel III uses a gradual increase in its minimum LCR ratio, so banks need to adjust to this new

scheme in the next 5 years. Hence, as of 2015, at least 60% of a bank’s liabilities should be

covered by cash or cashable assets. This ratio will increase and reach 100% by 2019.

Regulators aim to ensure that a bank has enough high-quality liquid assets with to meet its

liabilities for a 30 calendar under a stress scenario. For emerging market countries there are in

fact two LCR ratios, one for local and one for foreign exchange positions.

Table 1: Minimum LCR Ratios Applicable Each Years

Year

2015

2016

2017

2018

2019

Minimum LCR

60%

70%

80%

90%

100%

Source:

www.bis.orgNet Stable Funding Ratio (NSFR)

On the other hand, Net Stable Funding Ratio measures the amount of long-term and stable

sources of funds relative to the liquidity of assets. This measure requires a minimum amount

of funding to be stable over a time horizon of one year. In this regard, retail deposits and

savings account will be more critical for banks. Even though this requirement will take place

later than LCR, banks should get ready for these changes.

Leverage Ratio

Even though risk based capital has certain advantages, over the recent crisis, regulators have

witnessed some negative implications of this calculation method. Therefore, a plain and non-

risk based approach was also planned to be used as a complementary tool to risk based capital.

As the Basel Committee states in 2014 "

An

underlying feature of the

financial crisis was the

build-up of excessive on- and off-balance sheet leverage in the banking system. In many cases,

banks built up excessive leverage while maintaining strong risk-based capital ratios. At the

height of the crisis, the market forced the banking sector to reduce its leverage in a manner

that amplified downward pressure on asset prices. This deleveraging process exacerbated the

feedback loop between losses, falling bank capital, and shrinking credit availability."

12

See time table for Basel III.