36 / 187

36 / 187

Islamic Fund Management

22

trust funds. Although the idea of investing in a partnership (

musharakah

) fund is well

recognised in Shariah, there are issues that must be dealt with, such as the legal personality of

a company, the limited-liability structure of a company, participation in companies that

occasionally deal with prohibited transactions, e.g. usury, and the trading of shares (ISRA,

2015, p. 474-484). These issues were discussed at the OIC Islamic Fiqh Academy in 1992,

during its 7

th

session in Jeddah, Saudi Arabia; in 1993, during its 8

th

session in Brunei

Darussalam; and in 1995, during its 9

th

session in Abu Dhabi, the United Arab Emirates (UAE).

Notably, Resolution 63/1/7 at the 7

th

session prohibited investment in the shares of

companies that dealt with prohibited elements:

The basic principle is the prohibition of participating in companies that deal at

times in prohibited things such as riba etc., even though their main activities are

permissible.

However, prohibiting participation in such companies is deemed to inflict harm on the public

and cause hardship. That is why a ‘tolerant’ view has been adopted by many Shariah

authorities on the basis of necessity, which acknowledges the widespread use of interest in

commercial markets and the principle of removal of hardship and harm from Muslim

investors. This means that the impermissible businesses and operations of such companies are

restricted to a certain tolerable limit (the SAC of the SC, 2006; AAOIFI, 2015).

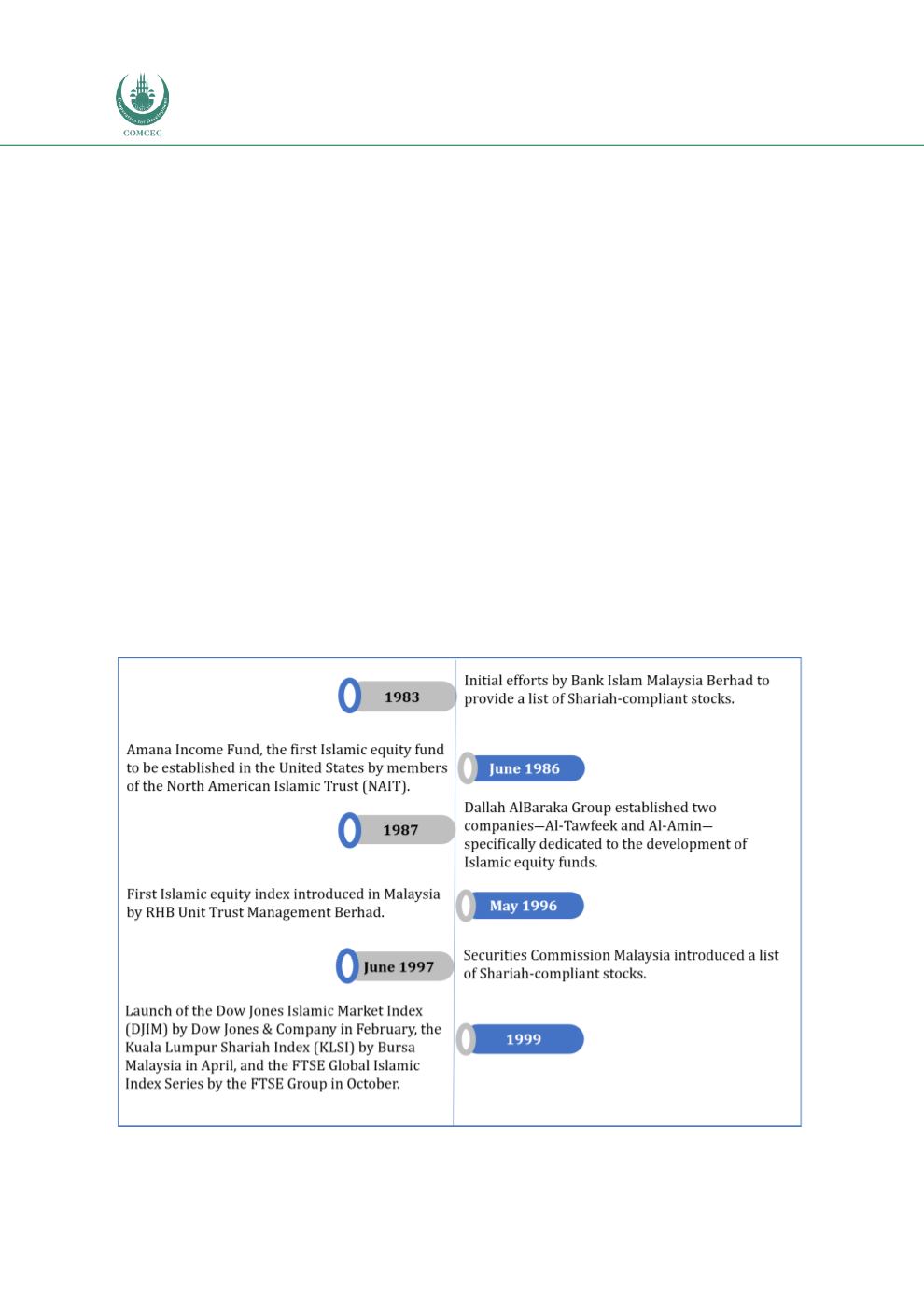

The review and identification of Shariah-compliant stocks had led to further developments in

Islamic equity markets, as elucidated i

n Figure 2.5 .Figure 2.5: Further Developments in Islamic Equity Markets

Source: IOSCO (2004)