35 / 187

35 / 187

Islamic Fund Management

21

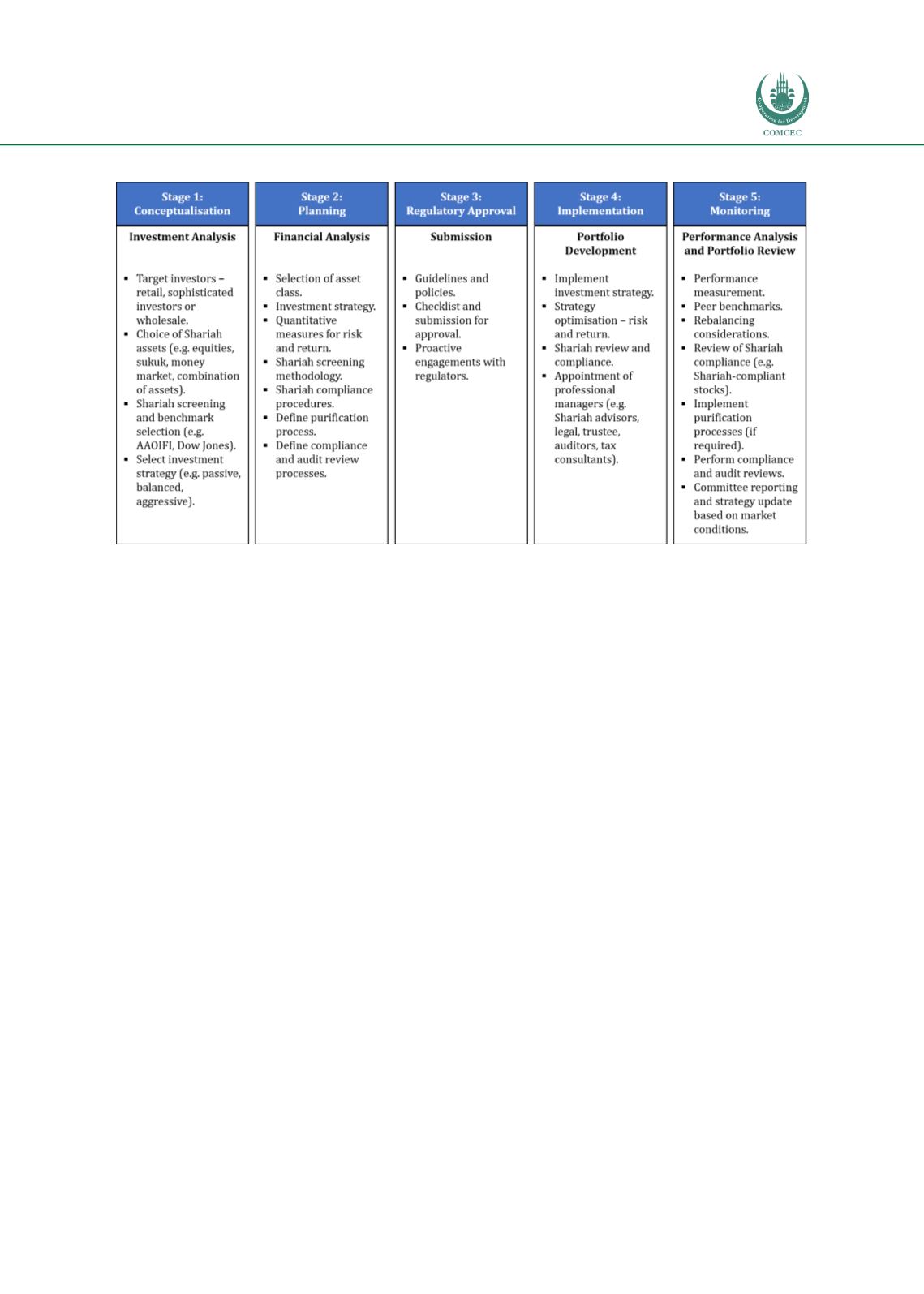

Figure 2.4: Process Flow of Fund Development

Sources: Saturna Sdn Bhd, Amundi Islamic Malaysia Sdn Bhd, Franklin Templeton Asset Management (Malaysia)

Sdn Bhd, RAM

Additionally, Islamic fund managers need to take into account the specific Shariah-related

issues discussed earlier in

Figure 2.2 .These include the elements of proscribed investments

and activities, the requirements for Shariah screening of investments, the necessity of

appointing a Shariah board and carrying out Shariah reviews and audits, the need for

purification of income, and the application of the appropriate fee structure.

The idea of setting up a mutual fund is reportedly a relatively recent development. It dates

back to the beginning of the 20

th

century when Boston law firms had initially established trust

divisions to manage the assets of wealthy families (Pozen and Hamacher, 2011). The mutual

fund had then evolved as the wealth of families were passed down through generations, with

the ensuing need to manage multiple family accounts. In 1924, the concept of open-ended

funds was mooted as the fund accepted new money and allowed investors to redeem their

shares on a daily basis (Pozen & Hamacher, 2011).

The concept of Shariah-compliant funds, on the other hand, arose from Muslims’ need for the

management of their investments in accordance with their faith. The concept of fund

management had been originally been adopted from the Islamic practice of endowment (

waqf

)

(ISRA, 2015, p. 534).

The first modern Islamic investment fund in Malaysia appeared in the early 1960s, with the

development of the Tabung Haji (Pilgrimage Fund). This fund collects the savings of Muslims

who wish to go on the pilgrimage (

hajj

). This idea is being increasingly used in many other

countries to kickstart their fund management industries.

Another aspect of the early-stage development of the Islamic equity markets had centred on

the need to establish clear guidance on the Shariah legitimacy of investing in company shares,

especially when such firms deal with prohibited elements such as

riba

(interest), and in unit