20 / 127

20 / 127

Barriers and Opportunities for Enhancing Capital Flows

In the COMCEC Member Countries

12

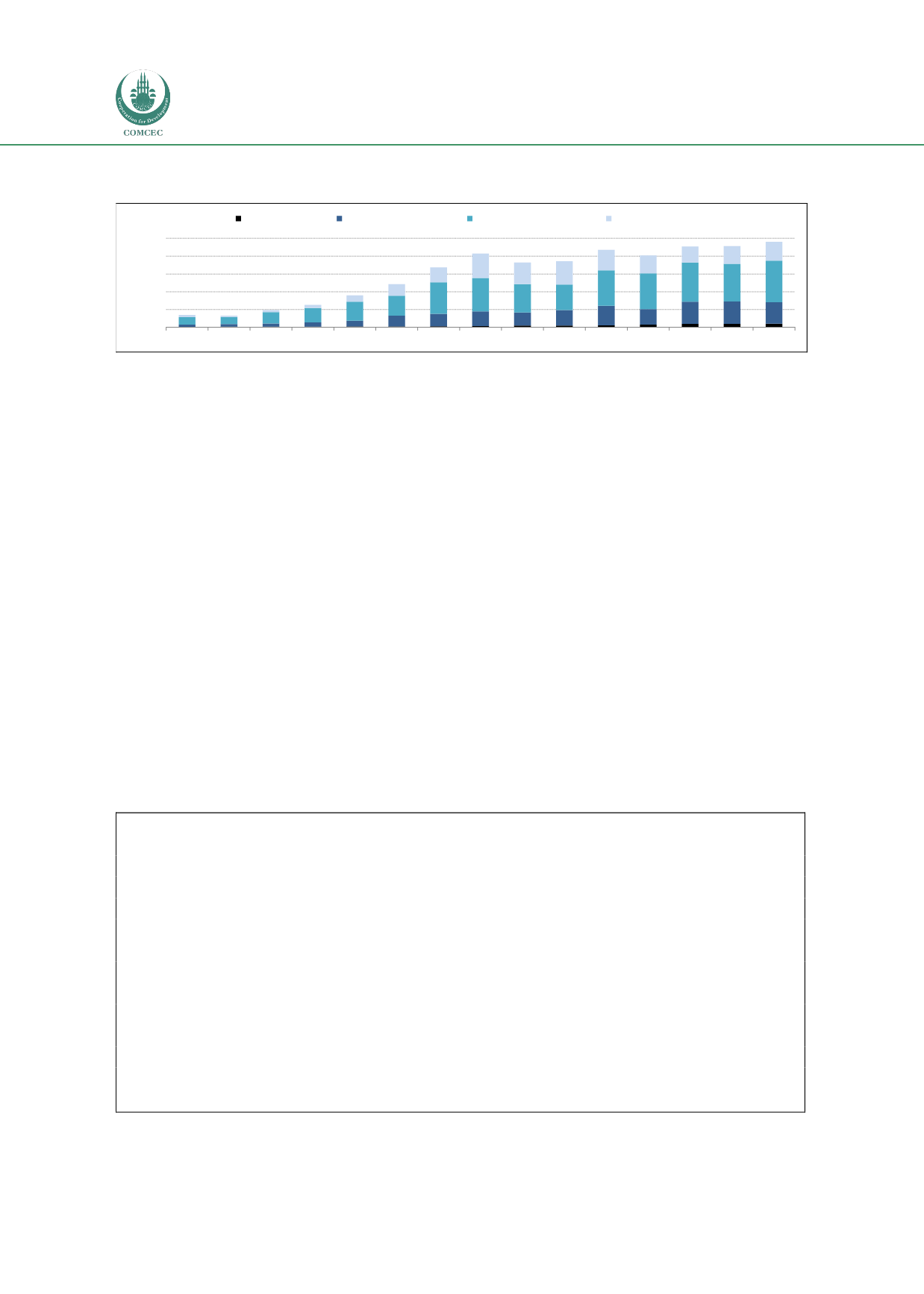

Figure 1.3: Share of capital inflows (excluding IMF credit) by income group, 2000-2014

Source: EIU Country Data

The bulk of capital inflows over the last decade have been to countries in the upper-middle

income group (see Figure 1.3). Notable among the countries in this group is Turkey, which has

been growing strongly and running large current-account deficits. The EIU expects Turkey to

draw capital inflows of US$95.6bn in 2013, outstripping the US$86.6bn of capital inflows

attracted by the top three countries in the high-income group – Saudi Arabia, Qatar and the

UAE – combined.

Also notable among the upper-middle income countries is Kazakhstan, which received average

capital inflows of US$17.7bn in 2008-12, equivalent to over 12% of GDP. FDI inflows alone

averaged US$13.6bn during the period 2008-12, dominated by investment in energy and

mining, sectors that require significant long-term capital commitments. According to official

data, 22.9% of FDI in 2011 was directed to existing mining operations, while mineral

exploration (largely oil) accounted for 37.8% of investments.

In third place in the upper-middle income group in terms of capital inflows is Malaysia. In

2012, Malaysia received just under US$30bn (US$29.7bn) in capital inflows – equalling the

total combined capital inflows for the other nine countries within this group (US$29.6bn),

illustrating that the other countries within this income group pale into significance when

compared with the top three countries in attracting capital flows.

A comparative story

In 2012, Turkey was top in the COMCEC rankings, with net portfolio investments of

US$36.5bn. Turkey and Malaysia are classified as upper-middle income economies by the

World Bank; both these countries saw large capital inflows as a result of easier global

liquidity conditions following the global financial crisis of 2008. Malaysia’s focus on the

development of financial markets in a phased manner has made it less vulnerable to the

volatility in capital markets following the threat of tighter liquidity conditions looming

ahead. Turkey, on the other hand, adopted a series of macro-prudential measures in 2010

to increase the resilience of the financial system to external shocks by increasing reserves;

it also raised monetary policy effectiveness by introducing the separate management of

domestic and foreign liquidity. The new monetary policy framework used weekly repo

rates, interest rate corridors and other tools to manage credit, interest rates and liquidity.

These measures have contributed further towards bolstering confidence in Turkey.

0

100

200

300

400

500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

US$ billion

Low Income Group

Low Middle Income Group

Upper Middle Income Group

High Income Group