69 / 203

69 / 203

Special Economic Zones in the OIC Region:

Learning from Experience

53

Zones

Fiscal Incentives

Non-fiscal Incentives

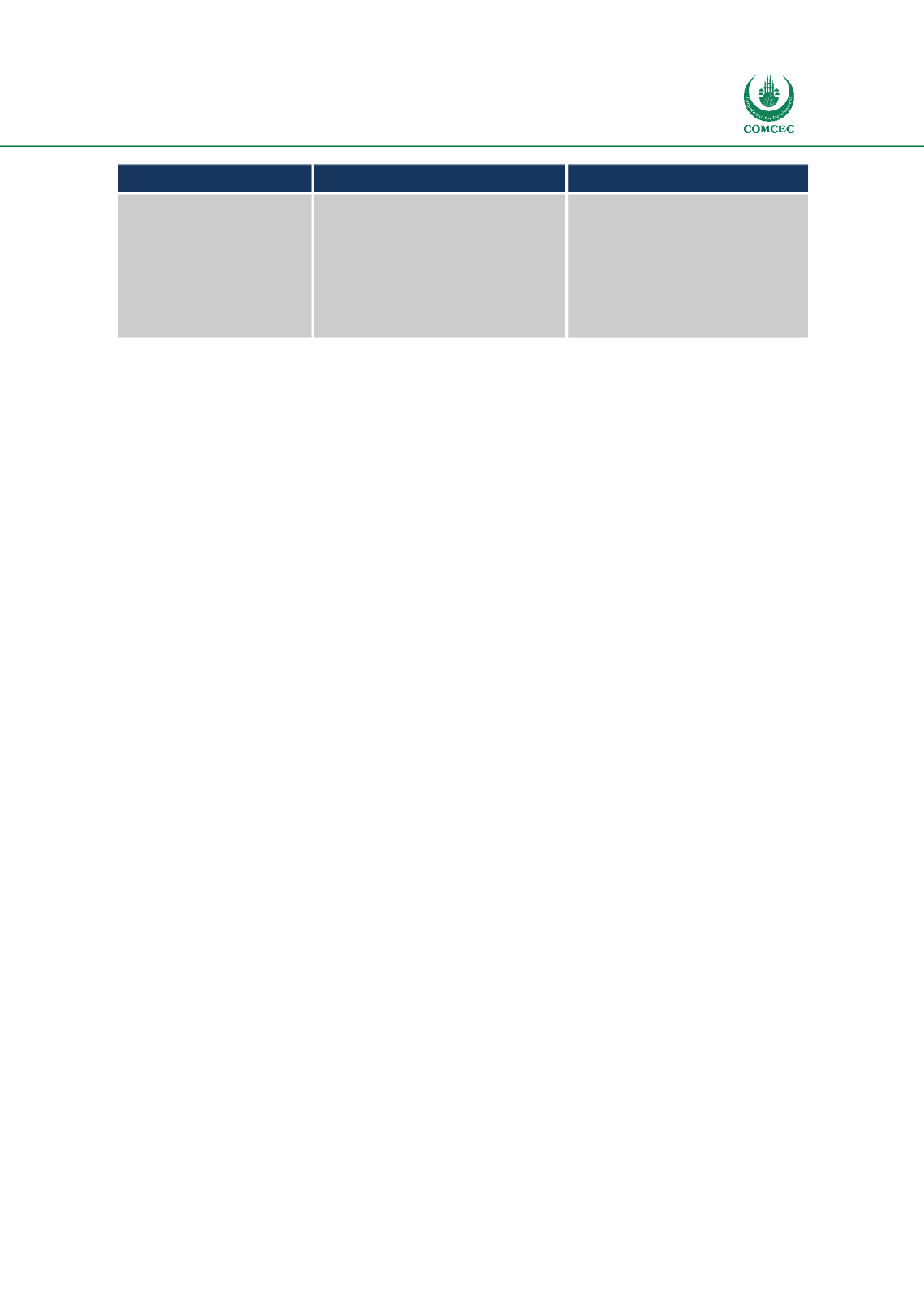

Ras Al Khaimah FTZ

0% import and re-export duties

0% personal income tax

Low land rates

No restrictions on employment

No restrictions on hiring of foreign

employees

Zero currency restrictions

Access to land through long-term

renewable leases

Source: BuroHappold Analysis 2017

A

s Table 4-3demonstrates, within the selected OIC SEZ case studies, a broad range of fiscal and

non-fiscal incentives are offered. It is observed that there are a number of common incentives

deployed to attract investments to SEZ, many of which have commonality with global

observations in SEZ development. The key regulatory, fiscal and financial incentives identified

in the above analysis are presented below:

Regulatory incentives:

o

Enhanced ability to employ foreign nationals; granting of visas and work permits;

o

Guarantees against nationalisation, expropriation and price controls;

o

Greater flexibility in repatriation of profits; and

o

Higher share of foreign business ownership.

Fiscal Incentives:

o

Exemption from corporate and personal income tax;

o

Reductions in customs duties, import/export tariffs and VAT on items related to

investment; and

o

Income tax exemption (mostly for an extended duration of ~5-15 years).

Financial Incentives:

o

State financed infrastructure;

o

Repatriation of profits;

o

Soft loans from national development banks; and

o

Preferential rates for land and utilities.

4.3

Evaluation of SEZ Development in OIC Member Countries

The following matrix provides a comparison of the SEZs selected for the comparative and

competitive benchmarking exercise including additional factors such as cost of energy and

competitive advantage.