153 / 178

153 / 178

148

industry in these three countries is largely governed by conventional laws.

Shari'ah

framework

and matters are left to the discretion of individual insurance and Islamic finance institutions.

It

would take some time for these countries to institute comprehensive

Shari'ah

framework for

Takaful

.

Some of the major challenges facing the

Takaful

industry especially in the three out of the four

countries selected for this study are: the absence of a comprehensive

Shari'ah

governance

framework for

Takaful

, lack of

Takaful

Shari'ah

standards, conflict between the existing legal

framework and

Shari'ah

requirements, and absence of

Shari'ah

conflict resolutions. For

example, there exist numerous conflicts between the

Shari'ah

principles and domestic laws.

There are cases involving Islamic contracts claimed to be non-

Shari'ah

compliant due to

ambiguous clauses.

8.3. Products and Services

Product development, innovation, new business models and quality of operations play positive

roles in the growth of the

Takaful

industry.

Takaful

companies must continue to invest in

research and product development. They need to be innovative and strategize for sustainability.

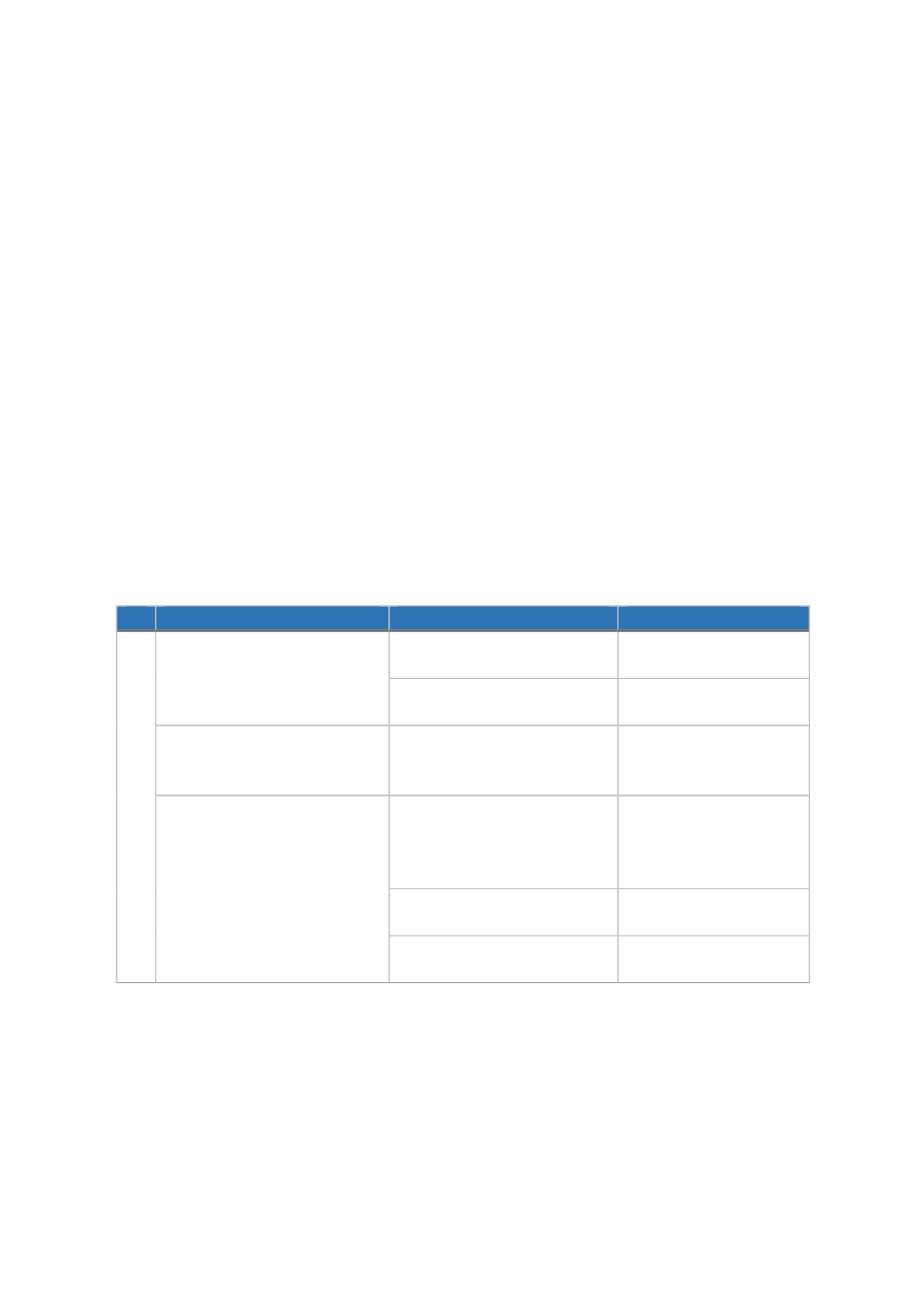

T

ABLE

24: P

RODUCT AND

S

ERVICES

I

SSUES AND

P

OLICY

R

ECOMMENDATIONS

No

Issues

Policy Recommendation

Country Affected

3

3.1. Lack of innovation and

use of technology

Developing unique and

original products

UK, Turkey and Saudi

Arabia

Investing in technology

UK, Turkey and Saudi

Arabia

3.2. Lack of customer

awareness

Awareness campaign among

the public and in schools

and colleges

Applies to all the four

countries

3.3. Weak market

penetration and

distribution channels

Promote the use of

technology particularly

InsurTech, and mobile apps

for micro-

Takaful

UK, Turkey and Saudi

Arabia

Diversify products to

include trade insurance

Applies to all the four

countries

Offer more

Re-Takaful

businesses

Applies to all the four

countries

Source: Authors

A good business model and product must be competitive, cost-effective and appealing to

consumers.

Takaful

companies must not continue to mimic the marketing strategy being

adopted by the conventional insurance. Instead they must innovate original products and

services. The constant change in customers’ taste and demands requires

Takaful

companies to