212 / 247

212 / 247

191

istithmar

contracts, which combine tangible assets (such as

ijarah

assets and shares) and debt

receivables (arising from

murabahah

or

istisna’

transactions), are rapidly gaining ground. The

benchmark issuances of

wakalah bil istithmar

sukuk by the IDB in 2003 and 2005 have

influenced other market players (including Turkish private sector issuers) to adopt the same

structure.

A similar scenario can also be observed in Asia, with the exception of Malaysia; Brunei,

Pakistan and Indonesia have adopted

ijarah

as the underlying Shariah contract for most of

their issuances. Unlike other countries in the region, Malaysia has been issuing sukuk based on

different Shariah contracts, predominantly

murabahah

. This is due to the varying opinions of

Shariah experts. For example, the trading of debt or

bay’ al-dayn

is a common practice in

Malaysia following the SAC of the SC’s acceptance of the principle of

bay’ al-dayn

as one of the

concepts for the development of Malaysia’s ICM instruments in August 1996. Over the years,

Malaysian practices have converged with international standards, hence the increased

issuance of

wakalah/wakalah bil istithmar

sukuk, which comply with the AAOIFI requirements

on secondary trading.

For most African countries that have issued sukuk, the frequently used Shariah contract is

ijarah

. The reasons cited by market participants include the simplistic features in terms of

flexibility, tradability and suitability in funding construction projects. Unlike the

murabahah

structure, the

ijarah

structure enables secondary trading of the sukuk instrument on an

exchange, which in turn helps increase investors’ participation in the transaction. Moreover,

the

ijarah

contract is innately designed to produce periodic rental payments, which

automatically act as coupon payments to sukuk investors. On the other hand, The Gambia has

issued short-term sukuk for liquidity management based on the

salam

contract.

Based on case studies and field visits to the selected countries, several key issues and

challenges confront the various sukuk markets in terms of structures, as explained in Table

6.2.

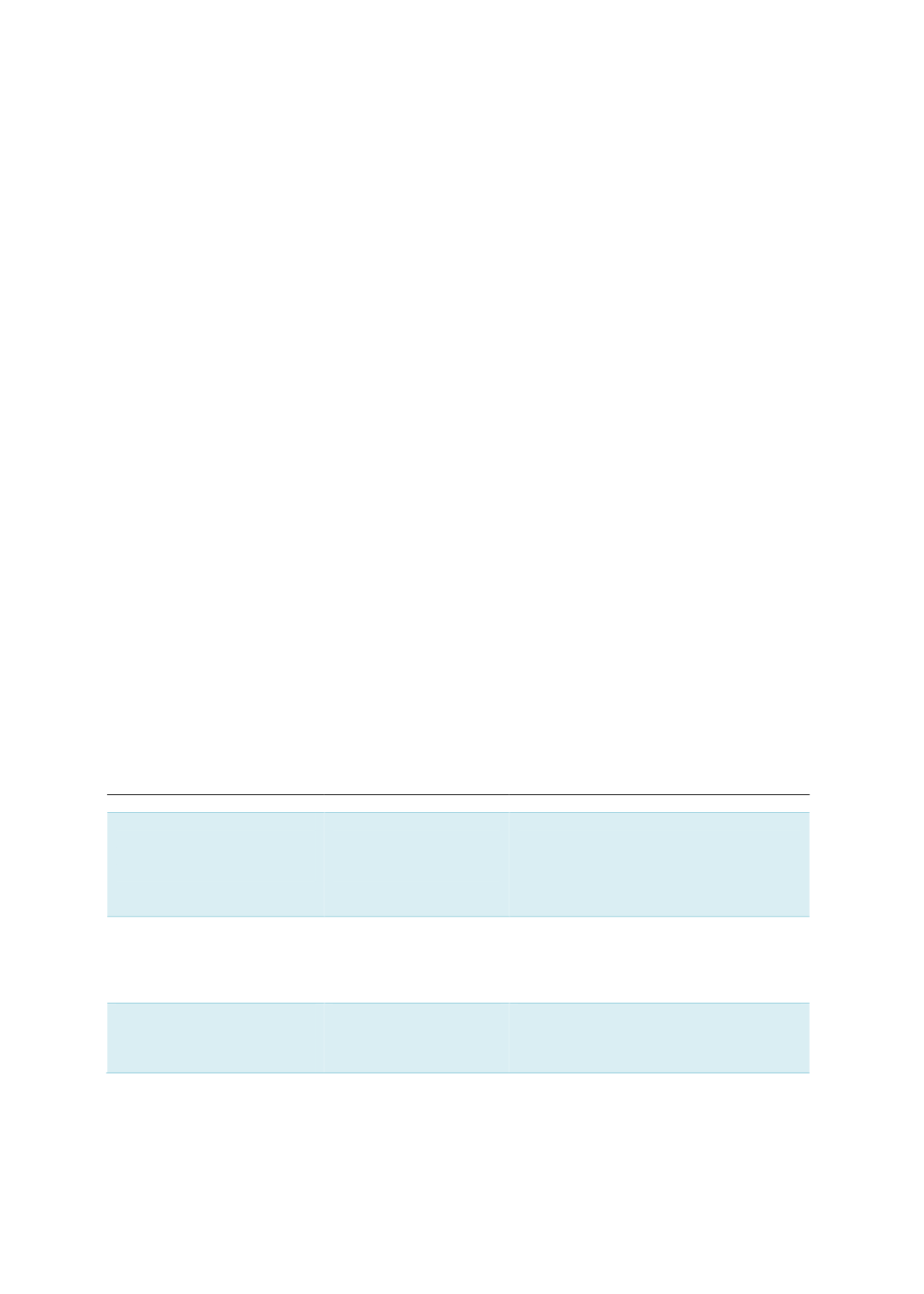

Table 6.2: Key Issues and Challenges of Sukuk Markets – Sukuk Structures

Issues

Affected countries

Recommendations

Limited sukuk structures

that have a balanced mix of

social considerations and

commercial values

Malaysia

UAE

Indonesia

Turkey

Hong Kong

Nigeria

To increase green and social sukuk that

embrace the VBI concept and SRI, which

looks at ESG screening.

Shortage of attractive sukuk

structures that cater to the

distinct requirements of

Shariah-based institutional

investors

UAE

Indonesia

Nigeria

Turkey

Hong Kong

To expand the boundaries of innovation in

sukuk structures (e.g.

waqf

-linked sukuk) to

entice religious institutional investors (e.g.

waqf

and

hajj

funds) to tap the sukuk

market.

Lack of understanding on

ICM instruments (e.g.

unfamiliarity with Islamic

structures and principles)

Indonesia

Turkey

Hong Kong

Nigeria

To increase market awareness on ICM

products through conferences, training

sessions and seminars.

Sources: RAM, ISRA