214 / 247

214 / 247

193

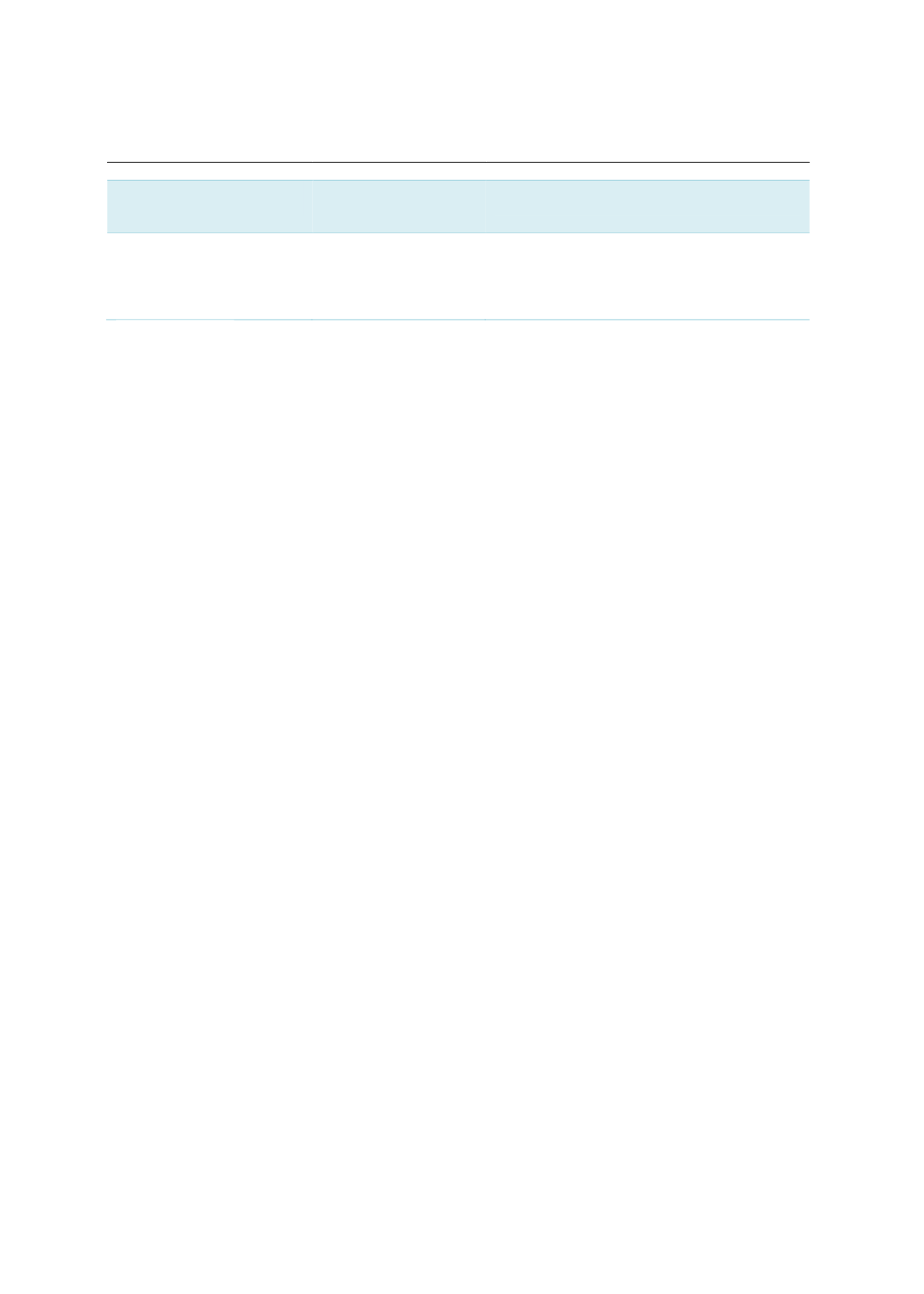

Issues

Affected countries

Recommendations

Not cost competitive for

corporate issuers

Indonesia

To amend the relevant tax laws to

encourage corporate sukuk issuance.

Unavailability/limited

retail sukuk

Malaysia

UAE

Turkey

Hong Kong

Nigeria

To make retail sukuk returns more

attractive and competitive than fixed

deposit rates.

Sources: RAM, ISRA

6.3

SUKUK INVESTMENTS (DEMAND – BUY SIDE)

The financial sector in Arab countries, particularly the GCC, is generally led by the banking

sector. NBFIs have a limited presence in the GCC. Investment funds have been expanding

rapidly in several countries, but focused largely on domestic equities and real estate. The

insurance sector, meanwhile, remains small and targets property/casualty risks. Contractual

savings are underdeveloped and dominated by public pension systems, which are mainly

defined as benefit, “pay as you go” schemes. Since most investment funds are owned by banks,

domestic investors of GCC sukuk are largely local financial institutions. A review of the

investor profile for the GCC’s recent bond issues (including sukuk) shows a high reliance on

foreign investors. Amid negative or near-zero bond yields in the UK, the euro zone and Japan,

these investors have been attracted to the bond yields offered by the Gulf region.

In Asia, Hong Kong and Malaysia have undergone healthy developments in their respective

financial markets, with strong intermediation from NBFIs. Indonesia, on the other hand, is still

working towards augmenting the ratio of its outstanding bond market against GDP. Based on

McKinsey Asian Capital Markets Development, Malaysia takes pole position among its Asian

peers, with a score of 3.25 (out of 5) in terms of funding scale, investment opportunities and

pricing efficiency; Indonesia recorded a score of 2.20.

Elsewhere, African countries liberalized their financial sectors in the late 1980s and 1990s, as

part of the structural adjustment programmes promoted by the IMF and the World Bank. The

reforms included the removal of credit ceilings, the liberalization of interest rates, the

restructuring and privatization of state-owned banks, and the introduction of a variety of

measures to promote the development of private banking systems as well as financial markets.

South Africa’s financial market appears to be the most advanced, as evinced by the increase in

its outstanding bonds and market capitalization as a percentage of GDP. Nonetheless, Africa’s

financial system remains relatively underdeveloped compared to other emerging markets.

Based on its investor profile, Africa’s debt securities are mainly held by foreigners. Although

African governments have implemented measures to hasten the development of NBFIs, they

are still hampered by challenges such as financial inclusion and low savings rates.

The main issues and challenges facing the sukuk market in terms of demand are briefly

presented in Table 6.4.