212 / 231

212 / 231

Diversification of Islamic Financial Instruments

198

An extension of the Takaful sector is the micro-Takaful which can be focused on by the

policy makers to protect the people from unexpected shocks to income and enhance

productivity through better health for the poor and the vulnerable segment of the

society

Supportive institutions need to be established in order to promote NBFIs which can

provide governance and leadership; promotion of risk sharing and entrepreneurship;

and a sound regulatory and supervisory framework.

The supply side issue of NBFIs can be addressed by the policymakers focusing on

increasing the number and diversity of Islamic NBFIs, together with increasing the

range of products offered to various segments.

On the demand side, low levels of financial literacy about the products and services

offered by Islamic NBFIs; cultural, social, and physical barriers; insufficient consumer

protection practices; and reputation- and credibility-related challenges are the biggest

obstacles hindering further improvement of Islamic NBFIs. A balanced and enabling

regulatory and taxation framework that also fosters cross-border investments in the

Islamic NBFI sector is also needed.

These policy recommendations are further broken down to specific steps and who should be

responsible for it in the following table.

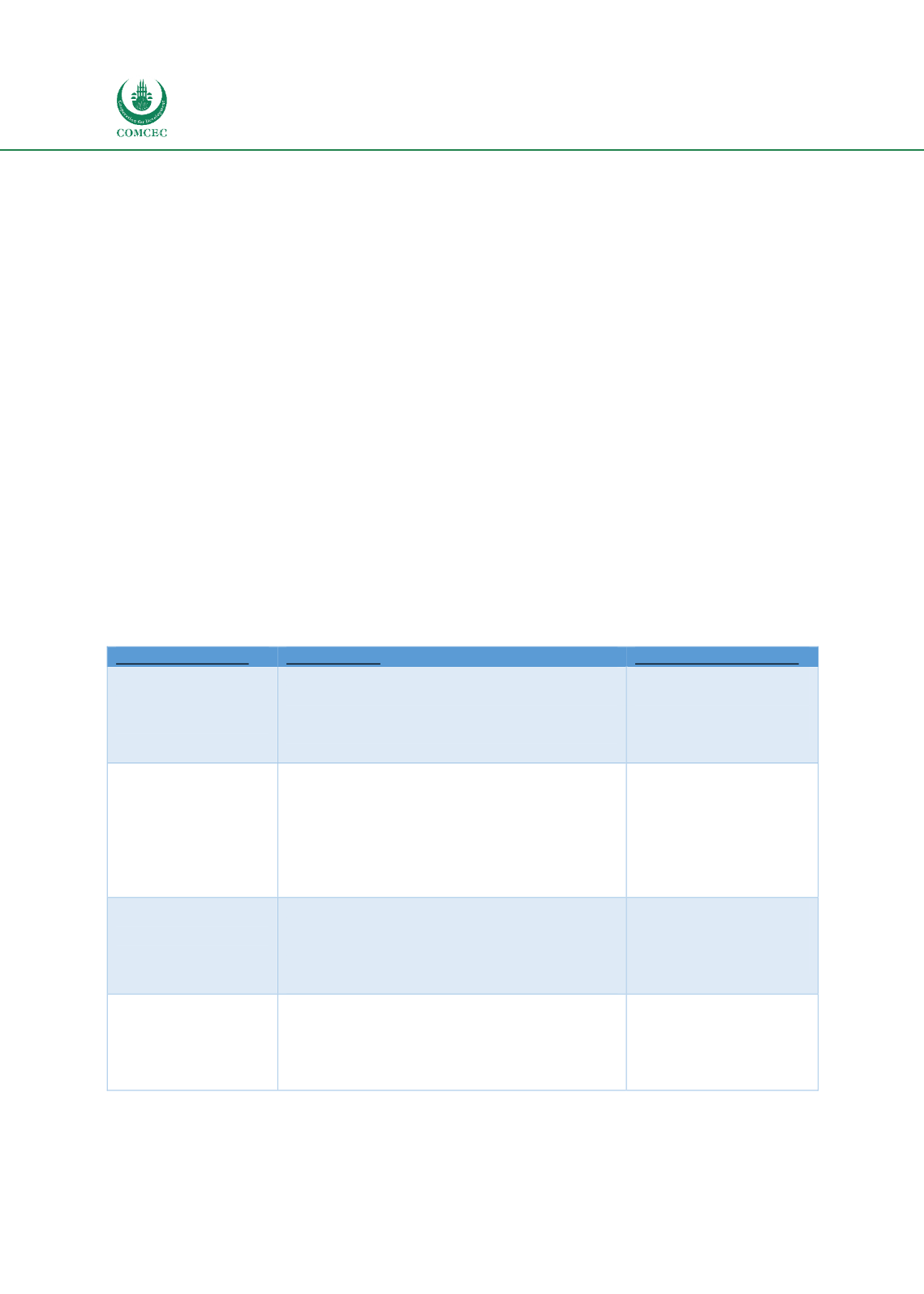

Table 82. Policy Recommendations for Development of Islamic Insurance-Takaful

Recommendation

Specific Step

Implementing Agency

Development of

Takaful Sector

Develop laws that allow for establishments of

Takaful Companies.

Provide incentives to expand Takaful business.

Provide tax advantage for Takaful investors.

Ease cross-border takaful expansion.

Central Banks of OIC

member countries

International Islamic

Financial Bodies

Development of

Micro-Takaful

Develop laws that allow for establishments of

micro-Takaful Companies.

Provide incentives to expand micro-Takaful

business.

Provide tax advantage for micro-Takaful

investors.

Ease cross-border micro-takaful expansion.

Central Banks of OIC

member countries

International Islamic

Financial Bodies

Increase Number of

NBFIs

Incentivize expansion and creation of NBFI’s.

Develop infrastructural support for NBFI’s in

forms of NBFI parks and preferable laws.

Assist in developing Shariah standards

harmonized across jurisdiction for NBFI’s.

Central Banks of OIC

member countries

International Islamic

Financial Bodies

Enhance Islamic

financial literacy

Develop trained Islamic banking professionals

More Shariah scholars with sound financial

knowhow

More financial experts with sound Shariah

knowledge

Islamic finance

educational institutions.

Central Banks of OIC

member countries

Source: Created by Author