211 / 231

211 / 231

Diversification of Islamic Financial Insturments

197

Variable and perverse tax regimes classify interest as a tax-deductible expense while

equity dividends are not. This skews the playing field in favor of debt based

instruments rather than equity. Taxation amendments is the need of the hour to create

a level playing field.

Tax neutrality for Sukuk structures is essential as Sukuk currently entail multi-layer

legal transactions which increases the tax cost of the issuer.

Governments need to be encouraged to either issue themselves, or through their

agencies, Sukuk with varying maturities to develop a long-term yield curve and to

develop a corporate Sukuk market, as well as to promote transparency and efficiency

of the asset pricing.

These policy recommendations are further broken down to specific steps and who should be

responsible for it in the following table.

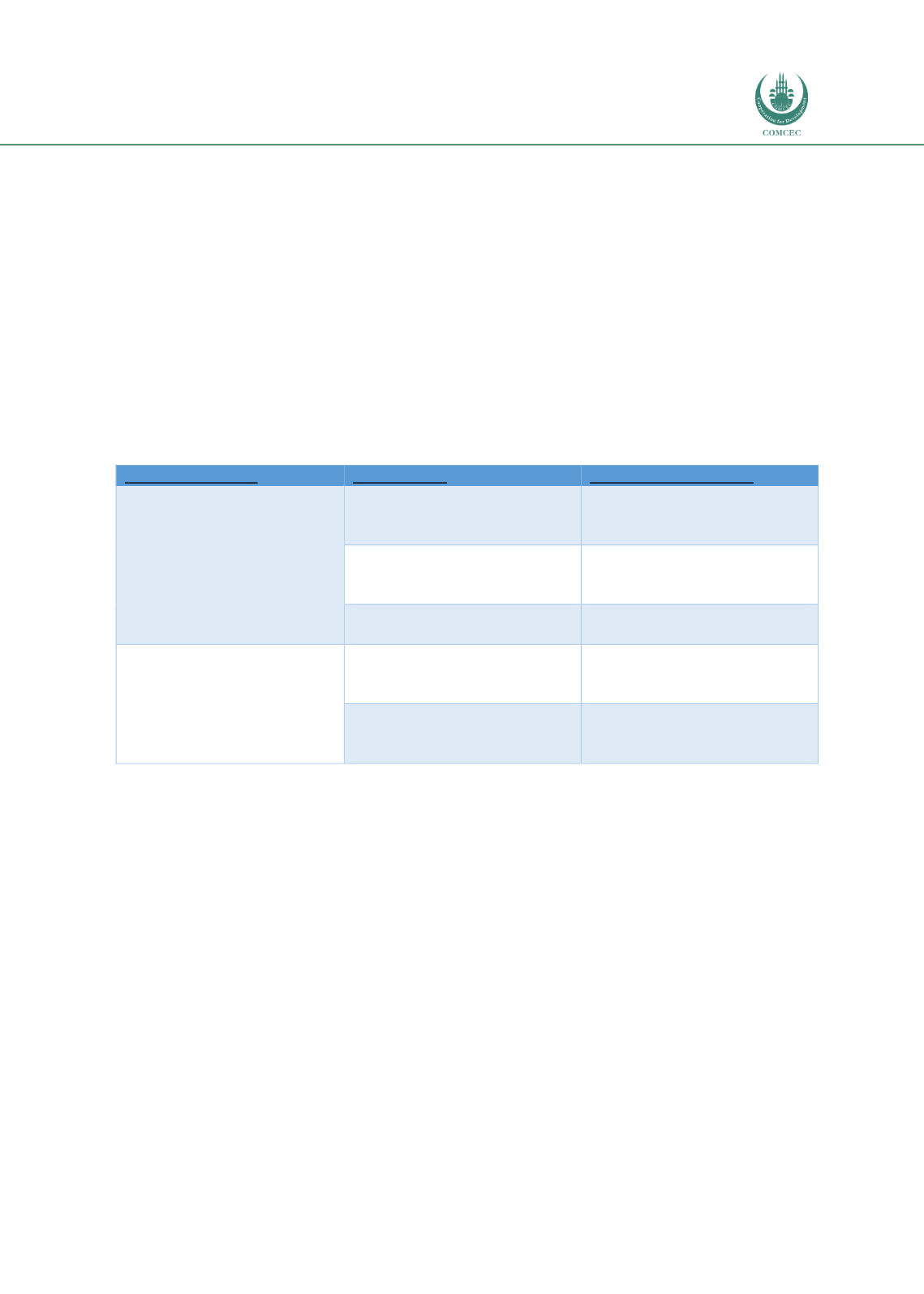

Table 81. Policy Recommendations for Islamic Capital Markets Development

Recommendation

Specific Step

Implementing Agency

Tax Regime Management

Remove double taxation and

tax loopholes for Sukuk

issuances.

Governments of OIC member

countries

Allow tax breaks to Shariah

compliant investments to make

them more appealing.

Central Banks, Securities

Commission and Governments

Tax Neutrality for Sukuk

Investors and Issuers

Central Banks of OIC member

countries.

Yield Curve Development

Issue different tenors of Sukuk

To create liquidity and a yield

curve.

Governments of OIC member

Countries

Corporates follow a similar

path to create corporate yield

curve

Central Bank and Securities

commission need to push

corporates.

Source: Created by Author

4.3 TAKAFUL (ISLAMIC INSURANCE)

The future of Islamic Finance under a risk-sharing model relies on development and further

strengthening of the Non-banking Financial Institutions Sector. Globally the importance of

nonbank financial institutions (NBFIs) has grown as they have contributed towards specialty

sectors such as housing finance, leasing, and asset management. Islamic finance with its risk-

sharing and asset-backed nature suits the NBFI category and the right instrument to

contribute towards economic development and providing access to all. This sector has been

neglected and needs to be given special attention by the policy makers and regulators. Some

important measures that policy makers and regulators can take on priority basis for the NBFI

sector are as follows.

The Takaful sector can be developed as it can play a critical role in enhancing financial

inclusion, reducing poverty, achieving inclusive economic growth, and boosting shared

prosperity. Takaful can provide important benefits to households and firms. Greater

access to financial services for both households and firms may help reduce income

inequality and accelerate economic growth.