210 / 231

210 / 231

Diversification of Islamic Financial Instruments

196

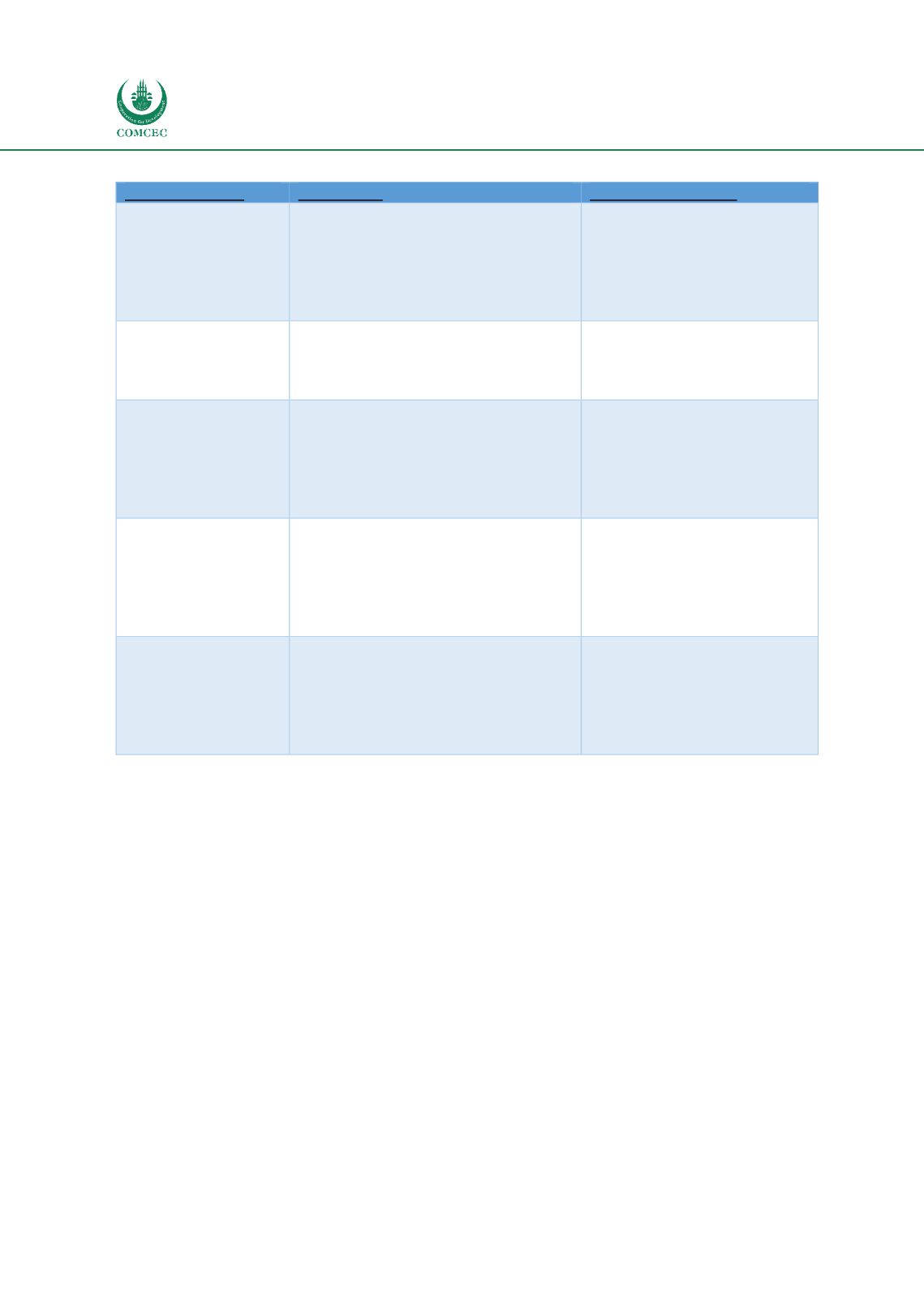

Table 80. Policy Recommendations for Islamic Banking Development

Recommendation

Specific Step

Implementing Agency

Regulatory

Standardization

Enabling regulatory environment and

laws.

Standardized and harmonized laws

across jurisdictions

Ease cross-border Islamic financial

transactions and banking activities

Central Banks of OIC member

countries

International Islamic Financial

Bodies

Promoting Risk-

Sharing

Develop Risk Sharing products on

asset side.

Reduce replication of conventional

Banking products

Islamic Bankers,

Shariah Scholars,

Central Banks of OIC member

countries

Shariah Governance

Create globally consistent Shariah

standards.

Monitor Shariah laws and new fatwas

for harmonized opinions.

Remove contrasting opinions in fatwas

across jurisdictions.

Governments of OIC member

countries.

International Islamic financial

agencies, including AAOIFI,

IIFM.

Customer Base

Expansion

Expand to lower income group of

society.

Create more products for poor people,

for agricultural sector, for SMEs etc.

Increase CSR activities for social well-

being

Islamic Banking institutions

Central Banks of OIC member

countries

Human Capital

Develop trained Islamic banking

professionals

More Shariah scholars with sound

financial knowhow

More financial experts with sound

Shariah knowledge

Islamic finance educational

institutions.

Central Banks of OIC member

countries

Source: Created by Author

4.2 ISLAMIC CAPITAL MARKETS

With the focus of Islamic finance on risk-sharing instruments, the Islamic capital markets

would play a crucial role as equity are the purest form of risk sharing finance. The

development of this component (Islamic Capital Markets) through equity based finance can

play a critical role in reduction of poverty, which is a main problem plaguing the Muslim world

today.

Albeit Islamic Capital Markets are young and smaller relative to Islamic banking, they are

growing at a fast paced and has the potential or promoting mutually shared growth and

prosperity through providing a base for financing infrastructure, raising funds for new

businesses, encouraging entrepreneurship, and supporting economic development. The

further development of Islamic Capital Markets is an essential ingredient for the sustainability

of Islamic financial sector truly based on a risk-sharing ideology. The policy direction and

efforts that need to be undertaken for promoting Islamic capital markets are like an extent to

those for Islamic banking sector but with a different focus.