169 / 231

169 / 231

Diversification of Islamic Financial Insturments

155

Qard saving account

Saving accounts based on qard refers to the contract of lending money by a lender (depositor)

to a borrower (banks) where the latter is bound to repay an equivalent replacement amount to

the lender. Under this contract, there should not be any contractual benefits offered by a

borrower to alender unless it is based on the borrower’s discretion and is not made

conditional to the qard. In the case that the borrower wishes to grant lenders some amount of

return, the return may be granted as Hibah (gift) to the lender.

Mudarabah Investment Account

The investment account product is based on Mudarabah contract, which is profit sharing based

equity contract, the ratio is proposed by the Bank based on the market benchmark rate that

reflect the performance of the underlying assets, the ratio and rate that have been offered to

the customers are also benchmarked against rates by other competitors. Dividend Rates is

agreed upon upfront and the ratio is pre-determined at the initial stage of concluding the

contract. The difference between murabahah concept in term deposit and mudarabah in the

investment account is that, for mudarabah, the bank will determine the rate upfront and will

make it known to the customer since it is sale based contract, the rate is calculated based on

selling price, whereas for mudarabah contract, the indicative rate displayed is based on the

history/previous performance of the bank.

Fixed Rate Term Deposit

The fixed rate in Islamic Deposit is based on the contract commodity murabahah/ Tawarruq.

The product of fixed deposit involves buying and selling of commodity using Bursa Malaysia

Suq Al-Sila (BSAS). The selling price in the product of fixed deposit is fixed, where the Bank

needs to pay the fixed selling price, which reflects fixed return to the customer.

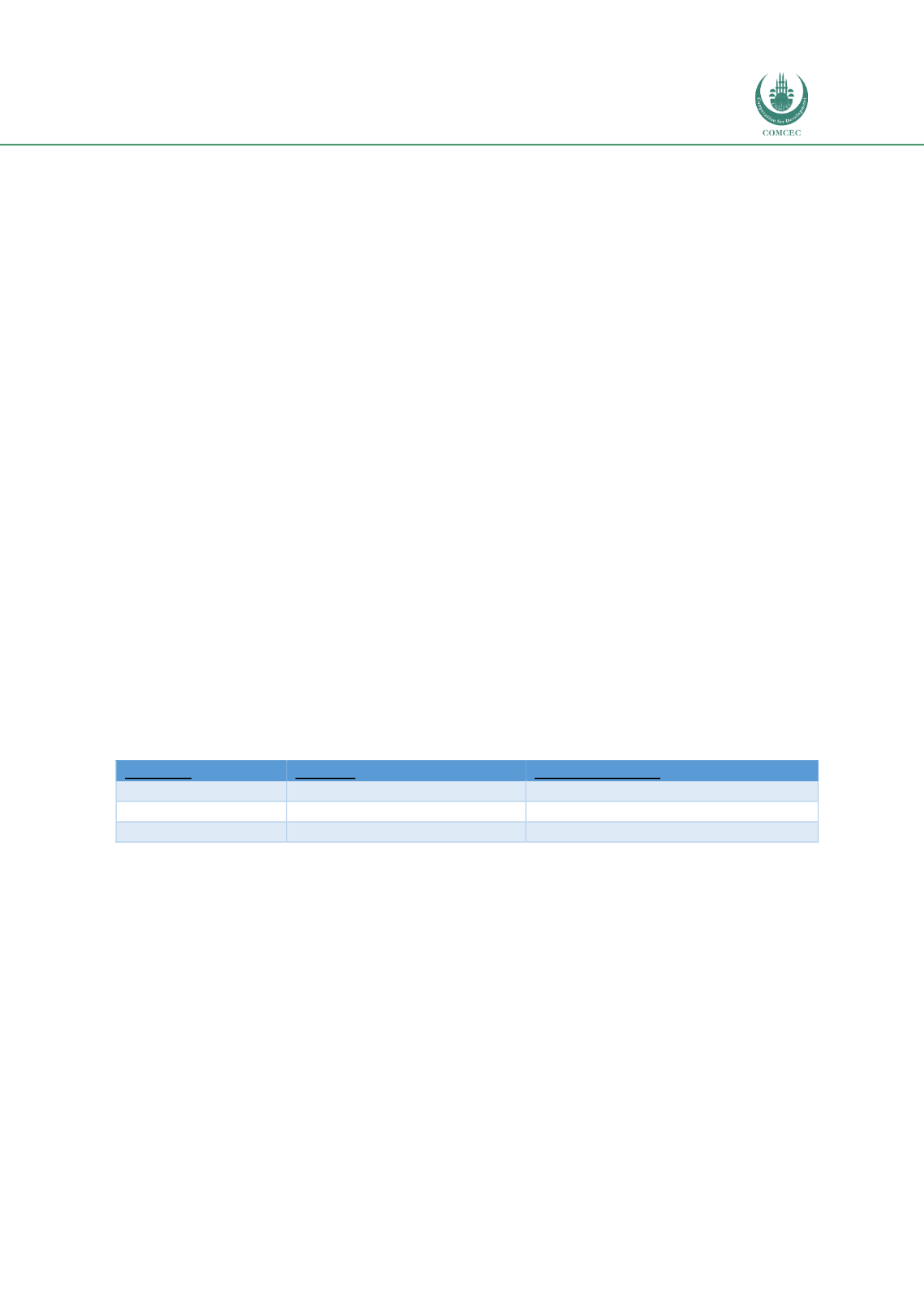

The list of deposit products for Consumer Banking is shown below.

Table 62: Deposit Instruments in Consumer Banking in Malaysia

Category

Product

Shariah Contract

Saving Account

Saving Account

Qard/Tawarruq

Current Account

Current Account

Qard/Tawarruq

Term Deposit

Islamic Fixed Deposit

Commodity Murabahah/Tawarruq

Source: Created by Author

Financing Products

Financing represent the deficit unit in the economic system, the Islamic bank offered various

facilities that benefit the customer needs. It includes home financing, vehicle financing, trade

financing and other services such as credit card, and others, below is short descriptions on the

most popular products in the financing side.

Home Financing

Home financing is financing product offered to the Islamic bank to finance the purchase of

property, residential and commercial, the home financing is offered based on different Shariah

contracts, as for the Home financing based on Equity or partnership basis, it is known as

Musharakah Mutanaqisah in which the Islamic bank and the customer will jointly purchase the