127 / 231

127 / 231

Diversification of Islamic Financial Insturments

113

contracts had been prescribed for the issuance of Sukuk. Four of them come under the Lease

Certificates (Sukuk), they include

88

:

Ownership-based (Ijarah);

Management Agreement-based (Ijarah/Wakala);

Trading based (Murabahah);

Partnership-based (Mudarabah/Musharakah).

Some of the characteristics of these lease certifcates are as follows:

Ownership based lease certifcates: These are issued to provide fnancing for the

acquisition of financil assets by the ALC from the originating institution.

These certifcates are backed by management contracts. They are issued to transfer the

proceeds generated to the ALC.

Lease certifcates tha are backed by trading, the proceeds generated from the sale these

assets are on deferred basis.

Lease certifcates backed tha are backed by partnership are issued for providing

fnancing to the ALC and become a shareholder of the joint-venture.

EPC based lease certifcates are aimed to fnance the realization of the project for which

the ALC shall be party to the EPC contract as well.

By the end of 2015 shows that Sukuk issuances have raised more than US$5.7 billion by the

private institutions. In addition, between 2012 and 2015, the sovereign has issued eight Sukuk

with a value of US$7.7 billion (IFN, 2016). However, given the overall size of the Turkish

capital market, this growth of Sukuk by the PBs and sovereign has been limited. It is vital that

new regulations are needed to promote Turkish corporate to issue Sukuk. The outstanding

Sukuk issuances are mainly denominated in US dollars with an average maturity period of 5

years. Turkiye Finance, Kuyet Turk and Treasury are the leading issuers of US denominated

Sukuk (see the two Tables on Sukuk issuances below).

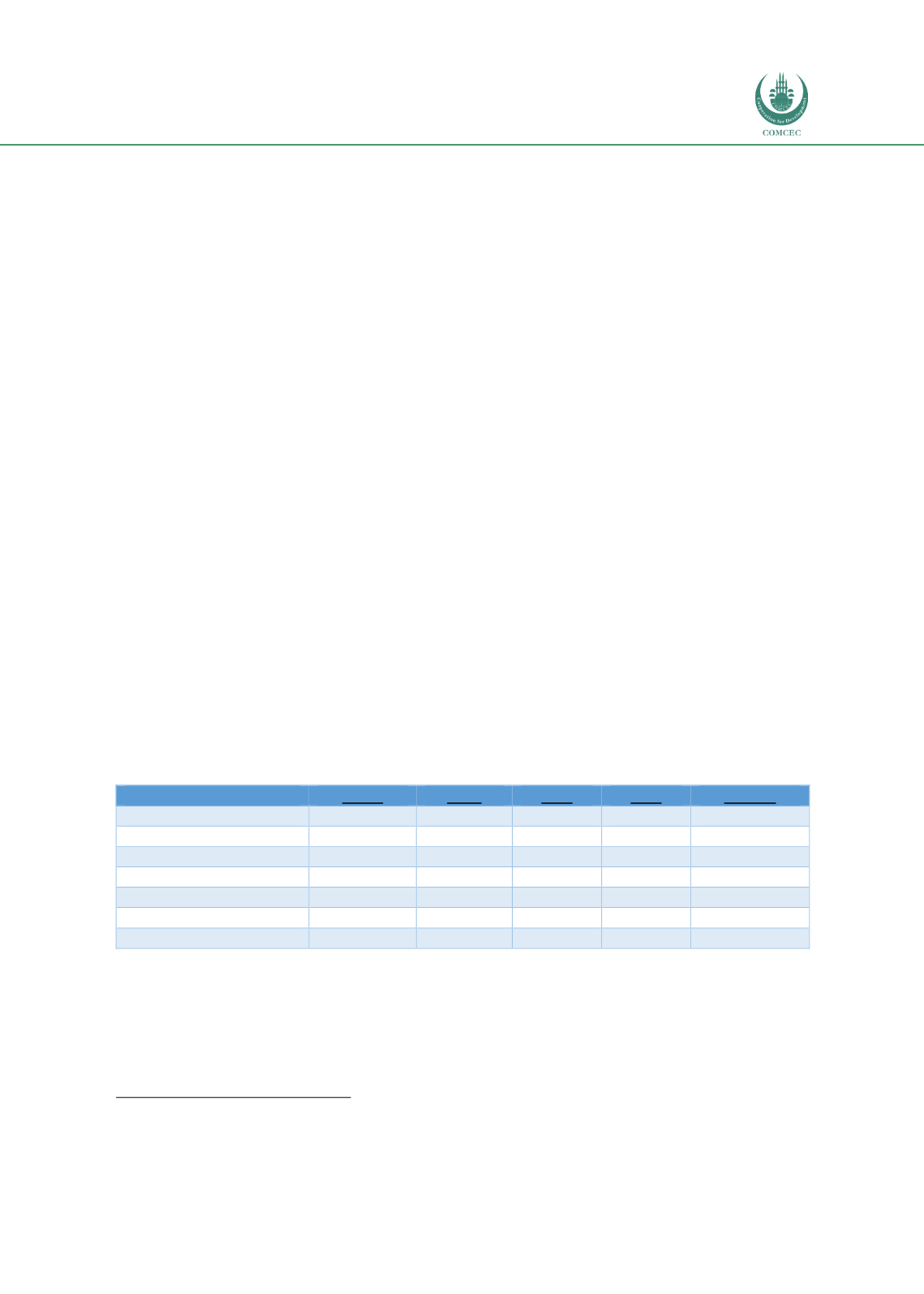

Table 51: Sukuk Issuance in Turkish Market

EUR0

MYR

TRY

USD

TOTAL

Matured

Domestic

74

74

Foreign

1

4

5

Outstanding

Domestic

20

20

Foreign

1

6

2

7

16

Total

1

6

97

11

115

Source: Undersecretariat of Treasury (2016)

88

The discussion on the structure of Sukuk issuance is primarily taken from, Erdem E. (2014), http//www.erdem-

erdem.av.tr/publications/prominance-of-sukuk-in-Turkey-as-an-islamic-finance-instrument.