125 / 231

125 / 231

Diversification of Islamic Financial Insturments

111

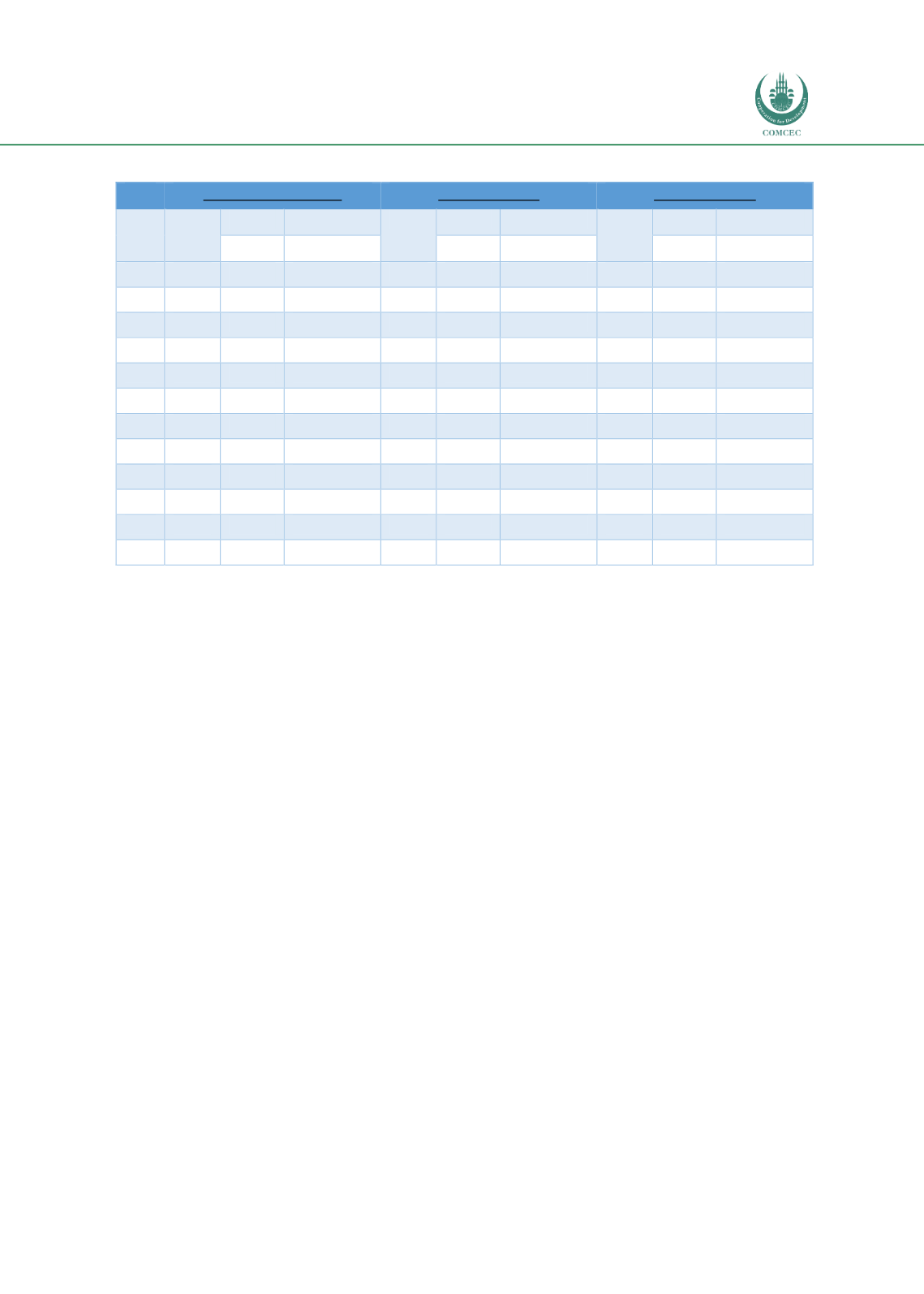

Table 50:

Selected Financial Indicators: Deposit Banks (Conventional) and Participation Banks

Capital Adequacy Ratio

Return on Assets

Return on Equity

Year

Sector

Deposit

Participation

Sector

Deposit

Participation

Sector

Deposit

Participation

Banks

Banks

Banks

Banks

Banks

Banks

2003

25.1

22.9

N/A

16.4

14.4

N/A

135.6

129

N/A

2004

30.9

28.2

N/A

2.5

2.4

N/A

18.1

19

N/A

2005

28.2

26.2

12

2.4

2.3

N/A

15.8

16.9

N/A

2006

23.7

21.6

12.5

1.7

1.5

3.5

12.1

11.8

36.9

2007

21.9

19.9

16.5

2.6

2.5

3.3

21

22.2

30.8

2008

18.9

17.4

16.1

2.8

2.7

3.1

24.8

26.6

30.7

2009

18

16.5

15.2

2

1.9

2.8

18.7

19.9

24.1

2010

20.6

19.3

15.3

2.6

2.6

2.4

22.9

25.2

19

2011

19

17.7

15.1

2.5

2.5

2

20.1

22.2

16.9

2012

16.6

15.5

14

1.7

1.7

1.6

15.5

16.8

14.8

2013

17.9

17.2

13.9

1.8

1.8

1.5

15.7

16.8

14.7

2014

15.3

14.6

14

1.6

1.6

1.3

14.2

15.1

13.8

Source: BRSA, Sakarya (2016)

A comparison of return on assets (ROA) and return on equity (ROE) reveals that the ROA and

ROE were 1.3% and 13.8% respectively for the depository banks, while they were 1.6% and

15.1% for the PBs in the year 2014. It is noticeable that the profitability ratios were

consistently higher of the PBs during 2006-2009. However, since 2009 and onward there has

been overall decline in these ratios due to overall global and domestic macroeconomic

conditions. The low economic growth of the real sector in recent years explains low

profitability of PBs as the bulk of short-term financing of PBs are linked to the activities in the

real sector of the economy.

Summary of Islamic Banking in Turkey

The growth of Islamic Banking in Turkey has shown notable increase over the past 10

years. The banks were able to double their market share to over 5% in 2015 from

2.5% in 2005.

The total assets of PBs reached US$42.2 billion by the end of 2015, which is five-fold

increase compared to its assets in 2005.

The dominant modes of financing are ‘Murabahah’ and ‘Ijarah’. Murabahah mode of

financing constitutes around 90%, while Ijarah (Leasing) mode of financing is 5%.

One of the major reasons for using ‘Murabahah’ is its short-term investment

mechanism. The overall market conditions in Turkey, where over 70% of funds

collected by PBs have three months maturity period (Taner, 2011) limits these banks

to resort to short-term investment financing modes.

Mark-up in ‘Murabahah’ also allows PBs to earn comparable returns with the interest

returns of the conventional banks.