113 / 231

113 / 231

Diversification of Islamic Financial Insturments

99

3.4.5 TAKAFUL (ISLAMIC INSURANCE) IN SUDAN

Overview of Takaful sector in Sudan

With reference to Takaful sector Sudan is the pioneer of both Takaful regulations and

developments since 1979. Sudan started Islamic Insurance in 1979 when Faisal Islamic bank

established the first Islamic Insurance Company in the world (Mohamed Abass 2012). In 1992

a new supervision law was introduced under which all companies were required to operate

according to

Shariah

principles (Abu Elbasher, n.d). Since Then Takaful spread to Malaysia in

1984 which has been also a pioneer in the developments of Takaful by the enactment of the

Takaful act of 1985- the first such regulatory act. The present insurance law in Sudan was

introduced in 2001 and is probably the only law which stresses on the authenticity of the

Takaful

principles. In addition, the law has placed strict measures on the investment returns,

surplus distribution and commission paid for the operator.

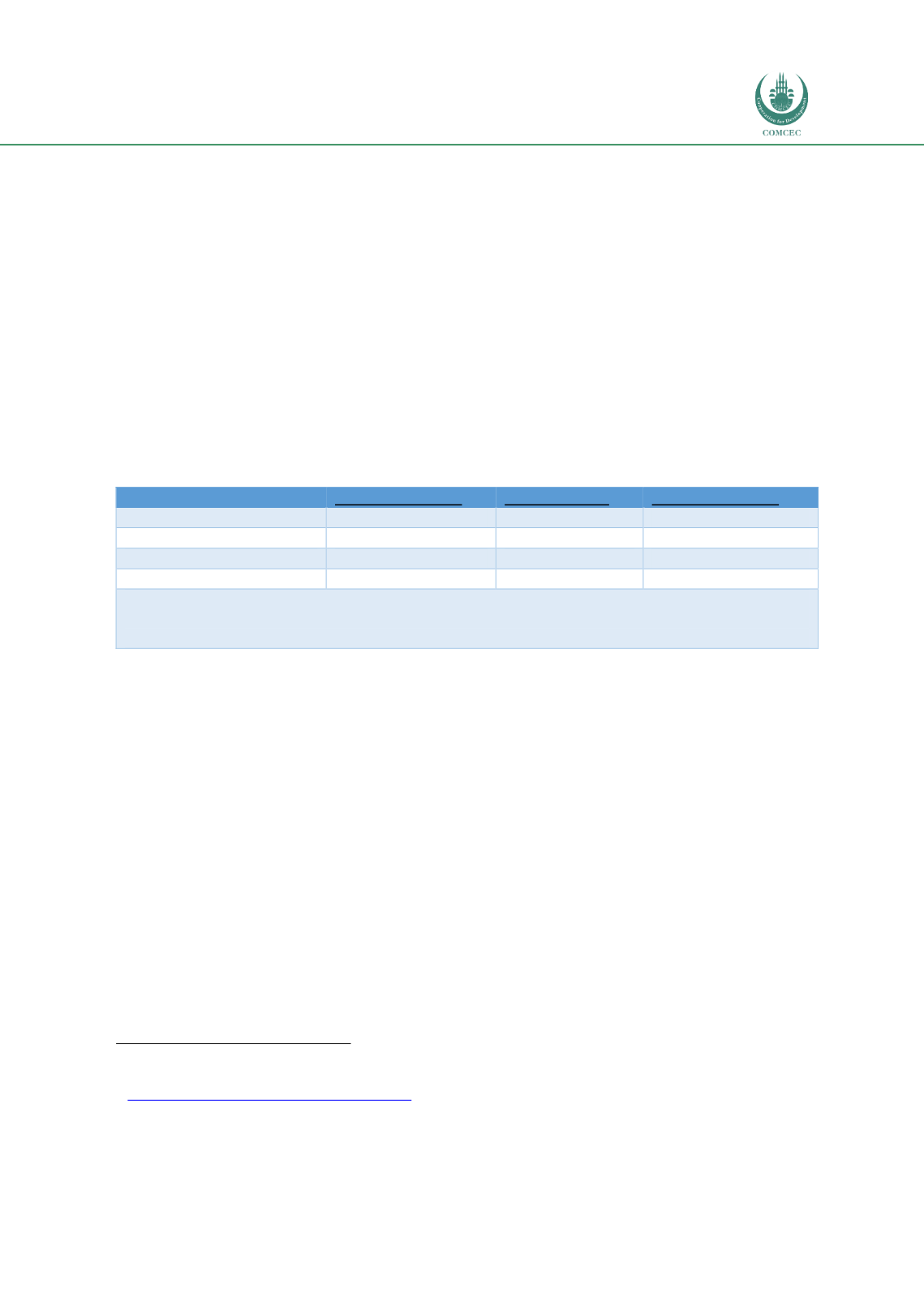

Table 43. Key Statistics of Takaful Sector in Sudan (2013)

No. of companies

Premiums* %

Investments** %

General & Life Takaful

4

62

68

Non-life Takaful

9

29

28

Retakaful

2

9

4

Total

15

100

100

*Premiums are the instalments (contributions) paid by clients of Takaful companies for getting Takaful coverage.

**Investments are Takaful company’s investment portfolios in different sectors

(real estate- bank deposits- shares –

sukuk) for a return.

Source: Bank of Khartoum

Takaful is consolidating its foundations in Sudan and has accomplished much over the past few

years, especially in the size of contributions. (Noor, 2015).

As seen in the above table, there

are 15

Takaful

and Retakaful companies in Sudan: 9 Non-life T

akaful

, 4 general and life

Takaful

and only 2

Retakfaul

companies as of 2013.

73

Main Takaful Products in Sudan

According to (Abu Elbasher, n.d), takaful companies in Sudan operate under mixed modes

namely:

Wakalah

and

Mudarabah

. The

Wakalah

model is used for insurance operations where

the company looks after the technical and administrative activities of technical and

administrative activities of the policy holders fund for a fee which is portion of the

contributions (actual management expenses). On the other hand, the

Mudarabah

mode is used

to invest the

Takaful

funds where the company invests the shareholders. The company invests

the shareholders fund according to

Mudarabah

agreement in which the company becomes the

Mudarib

and the shareholders are the owners of money (

rab-almal

). Profits are distributed

between shareholders and policyholders according to a certain policyholder’s agreement.

73

Note that in Sudan the whole insurance sector is based on Shariah-compliant principles, however, the terms “insurance”

and “Takaful” are used interchangeably and each insurance/Takaful company should have a Shariah committee.

http://elibrary.mediu.edu.my/books/RPS0008.pdf