115 / 231

115 / 231

Diversification of Islamic Financial Insturments

101

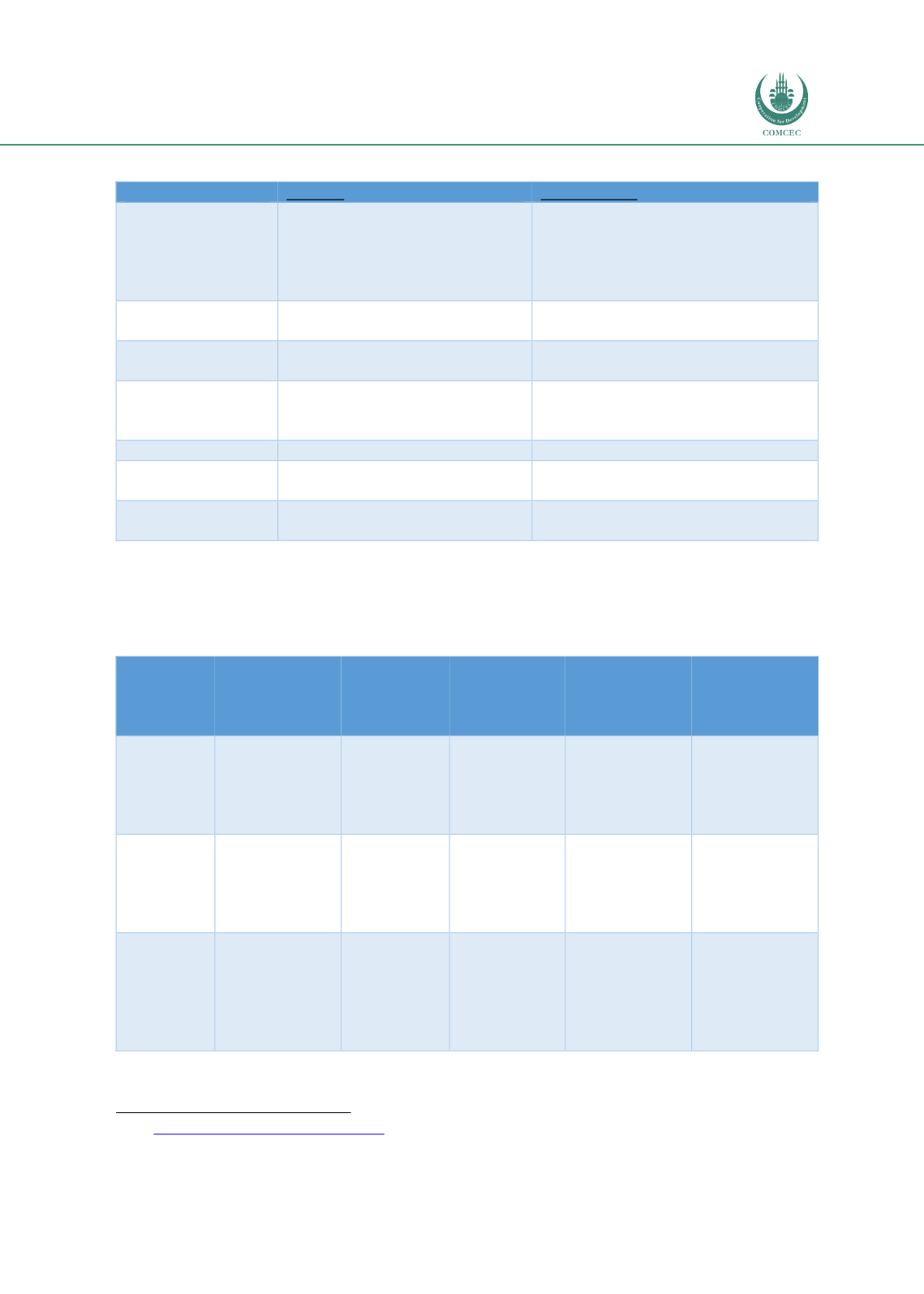

Table 44: Differences Between Takaful and Microtakaful in Sudan

Takaful

Microtakaful

Market

Policyholders are from middle

and high-income households

Policyholders are the poor and low-

income households, often working in

the informal economy and outside of

the social insurance coverage with

irregular income streams.

Market awareness

Market is largely familiar with

insurance

Market is largely unfamiliar with

insurance

Contributions

(premiums)

Based on age or other specific

risk characteristics.

Low contributions and affordable

Affordability

considerations

Contributions are paid by

policyholders

Contributions may be paid in full or

partly by a subsidy from zakah funds,

waqf funds or th government

Sums insured

Large sums insured

Small sums insured

Policy document

Complex policy document with

many exclusions

Simple and easy to understand policy

document with a few or no exclusions

Claims handling

Claims process for large sums

insured may be quite complicated

Simple and fast procedures to small

sums, yet still controls fraud

Source: Hasim (2014)

However, in Sudan the Microtakaful models are the same as the Takaful models as seen in

table below.

Table 45. Microtakaful Models

Aspects

Wakalah

Mudarabah

with surplus

sharing

Mudarabah

without

surplus

sharing

Hybrid

Waqf

Takaful

operator

share in

investment

profits

Fees as

percentage of

total

investments

Profit share

Profit share

Profit share

fees as

percentage of

total

investments

Takaful

operator

share in

underlying

surplus

Not available

Profit share

Not available

Profit share

Not available

Operating

expenses

Borne by

shareholders

which are

compensated by

upfront charge of

wakala fees

Borne by

shareholders

and no fees

Borne by

policyholders

and charged at

year end

Borne by

shareholders

which are

compensated by

upfront charge of

Wakala fees

Borne by

shareholders

which are

compensated by

upfront charge of

Wakala fees

Source: Haydari (2007), Erlbeck et al (2011), Khan (2011), Barawi (2012)

74

74

See

: http://slideplayer.com/slide/10448792/