108 / 231

108 / 231

Diversification of Islamic Financial Instruments

94

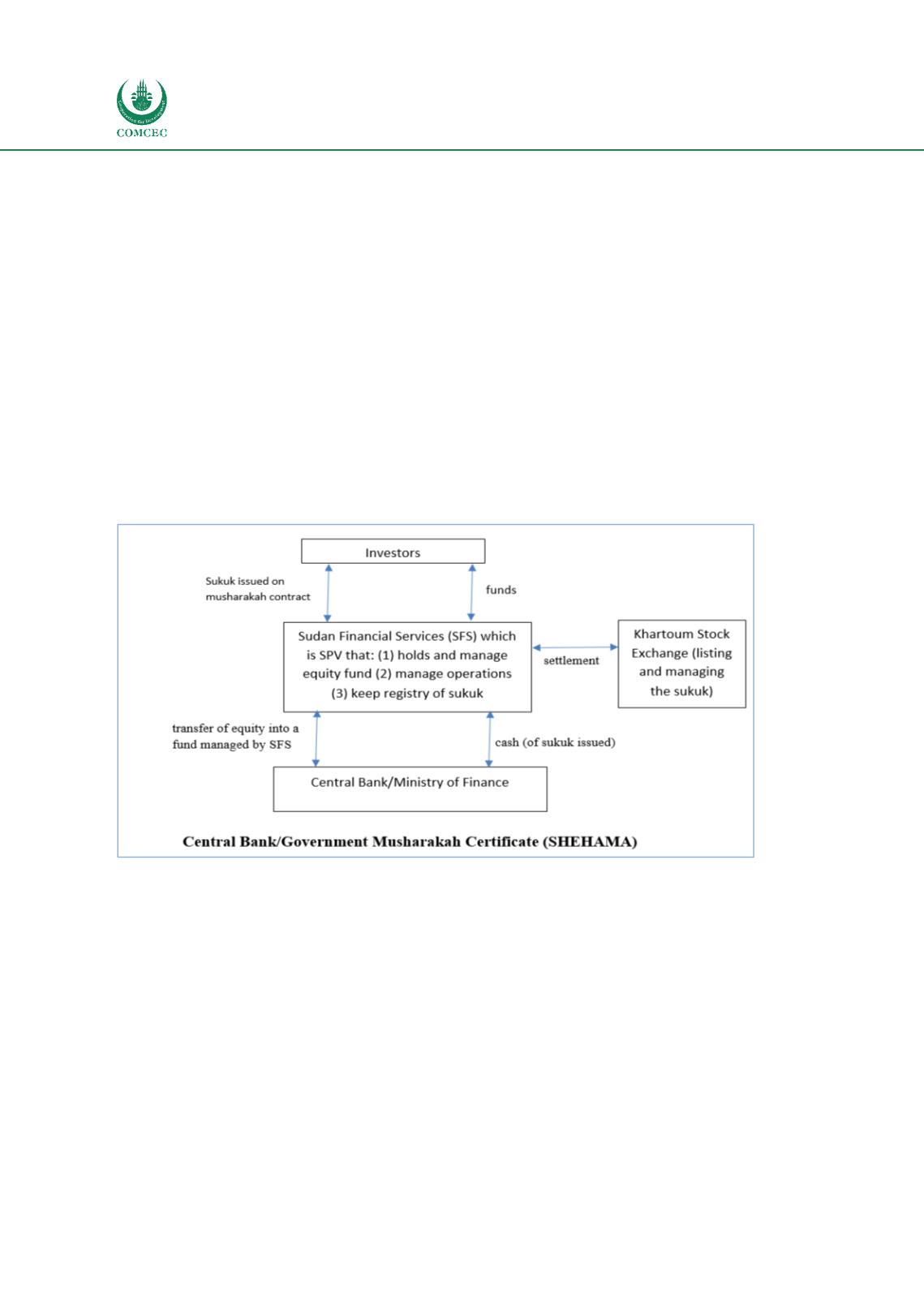

Government Musharakah Certificate (GMCs) – SHEHAMA

“From 2001 to early 2007 the government used short-term GMCs (SHEHAMA) to finance the

government budget deficit. Investment in GMCs was restricted to Sudanese only. Investors

received ownership interest in a portfolio of specific state-owned enterprises, whose profits

were distributed as pro-rated bullet payments at maturity. GMCs were tradable in the

secondary market immediately after issuance. In early 2007 the government discontinued

GMCs following reduced short-term financing needs. GMC is designed as an instrument based

on a profit- and loss-sharing contract. It is an asset based security issued against a certain

percentage of Government ownership in more profitable and joint venture enterprises. The

returns form GMC are determined by the expected return on the underlying asset where a pro-

rata share of the income stream is distributed between the partners. Among its features GMC is

fixed short-term maturity (one year), listed on and traded in the stock exchange (transferable

and fully negotiable), accessible to all, provides financing for Government’s budget deficit

through a non-inflationary instrument and can be used as a tool for open market operations”

(Sarker 2015).

Figure 12. Government Musharakah Certificate- SHEHAMA

Source: IIFM (2016)

Government Investment Certificate (GICs) – SARH

“In 2003, the government also introduced GICs to fund its trade, procurement, and

development projects. Unlike GMCs, investors are shareholders of an investment company

managed by SFSC and do not hold a title to government assets. GICs can also be traded in the

secondary market. GIC is designed as an asset-based security issued against a number of

contracts, including

Ijarah

,

Salam

,

and Mudarabah

. The relationship between the holder of a

GIC and the issuer is based on a restricted Mudarabah contract. The instrument’s maturity

profile ranges from two to six years. The expected return is determined by the fixed rental

income on

Ij

a

rah

plus the income from the sale of

Murabahah

,

Salam

and

Istisn

a

contracts.

Profit is distributed every three or six months. Sales of primary issues are made through an

auction system. The GIC is listed on the stock exchange. Among its features GIC appears