67 / 187

67 / 187

Islamic Fund Management

53

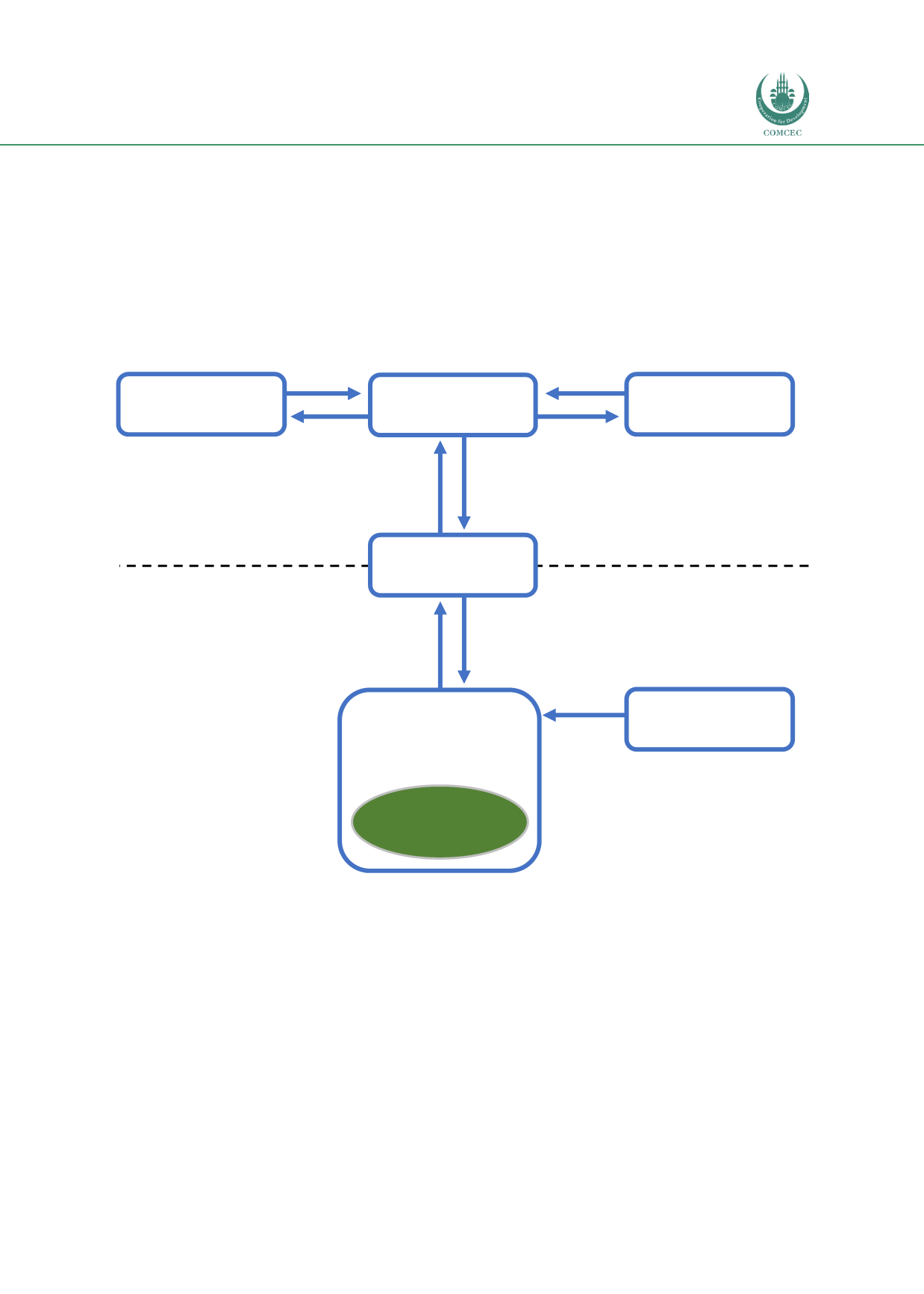

stock exchange will be linked to the NAV of the fund, but prices are available on a real-time

basis, depending on the trading volume of the stock exchanges. As such, arbitrage trading

ensures that the price of the ETF is typically very close to its NAV at any time. As the ETF

requires the ability to add/reduce it’s issued share capital according to demand, and as these

shares represent the underlying assets, the ETF utilises authorised participants (typically large

financial institutions) to create and redeem shares together with their underlying assets.

Figure 3.8shows the basic structure of an Islamic ETF.

Figure 3.8: Basic Structure of an Islamic ETF

ETF shares

ETF shares

ETF Provider

Cash

ETF shares

Cash

INVESTOR

(BUYER)

INVESTOR

(SELLER)

ETF shares

ETF shares

ETF shares

SecondaryMarket

Primary Market

SHARIAH

STOCKS/FOREX

/COMMODITIES

Islamic benchmark

index:

AUTHORISED

PARTICIPANTS

SHARIAHADVISORY

COMMITTEE

Advisory on

Shariah

matters

STOCK EXCHANGE

Sources: Nafis Alam (2013), RAM